Understanding how to calculate mortgage interest is a fundamental skill for anyone navigating the complex world of homeownership. For most individuals, a mortgage represents the largest financial commitment they will ever make. The interest rate attached to that loan directly impacts not only your monthly payments but also the total cost of your home over the loan’s lifetime. Far from being a mere number provided by a lender, comprehending the mechanics behind its calculation empowers you to make informed decisions, negotiate effectively, and even strategize ways to save substantial amounts of money.

This guide delves into the core principles of mortgage interest calculation, breaking down the formulas, illustrating with practical examples, and exploring the myriad factors that influence the rate you pay. By the end, you’ll possess a clear understanding of the arithmetic at play and be better equipped to manage your most significant financial asset.

Understanding the Components of Your Mortgage Interest Rate

Before we dive into the actual calculation, it’s crucial to differentiate between the various elements that constitute your mortgage and, by extension, the interest you’ll pay. These components work in concert to determine your financial obligation each month.

Principal and Interest

At its most basic, your mortgage payment is composed of two primary elements: principal and interest.

- Principal: This is the actual amount of money you borrowed from the lender to purchase your home. Every payment you make chipping away at the principal balance brings you closer to outright ownership.

- Interest: This is the cost of borrowing the principal amount. It’s the fee lenders charge for providing you with the capital, calculated as a percentage of the outstanding principal balance. In the initial years of a standard mortgage, a significant portion of your monthly payment goes towards interest. As time progresses and the principal balance decreases, a larger share of your payment begins to apply to the principal.

Loan Term

The loan term refers to the length of time over which you agree to repay the mortgage. Common terms are 15 years and 30 years, though other durations exist. The loan term has a profound impact on both your monthly payment and the total interest paid over the life of the loan.

- Shorter Terms (e.g., 15 years): Typically result in higher monthly payments because you’re paying off the principal over a shorter period. However, because you’re paying back the loan faster, you’ll incur significantly less interest overall.

- Longer Terms (e.g., 30 years): Offer lower monthly payments, making homeownership more accessible. The trade-off is that you’ll pay substantially more in total interest over the life of the loan, as the principal balance remains outstanding for a longer duration.

Amortization Schedule

An amortization schedule is a detailed table showing each payment made over the life of a loan, breaking down how much of each payment goes towards interest and how much goes towards principal, and the remaining loan balance. It’s a powerful tool for visualizing your loan’s progression.

In the early years of a mortgage, your payments are heavily weighted towards interest. This is because the outstanding principal balance is at its highest, and interest is calculated on that larger amount. As you continue to make payments, the principal balance gradually decreases, and consequently, the interest portion of your payment also declines, allowing more of each subsequent payment to go towards reducing the principal. Understanding this schedule can reveal opportunities for accelerated repayment and interest savings.

The Core Formula: Calculating Your Monthly Interest Payment

While the full mortgage payment calculation can be complex, understanding how to calculate the interest portion of your monthly payment is straightforward and provides critical insight into your loan.

The Basic Interest Formula

The core formula for calculating the interest portion of your payment for any given month is:

Monthly Interest Payment = (Outstanding Principal Balance) × (Monthly Interest Rate)

To use this formula, you first need to convert your annual interest rate into a monthly rate.

- Monthly Interest Rate = (Annual Interest Rate) / 12

Let’s break down the steps.

Illustrative Example

Suppose you have a mortgage with the following characteristics:

- Original Loan Amount (Principal): $250,000

- Annual Interest Rate: 4.5%

Step 1: Convert the Annual Interest Rate to a Monthly Interest Rate.

First, express the annual interest rate as a decimal: 4.5% = 0.045

Monthly Interest Rate = 0.045 / 12 = 0.00375

Step 2: Calculate the Interest Payment for the First Month.

Since this is the first month, your outstanding principal balance is the full loan amount.

Monthly Interest Payment (Month 1) = $250,000 × 0.00375 = $937.50

So, in your first mortgage payment, $937.50 will go directly towards paying off the interest accumulated that month.

Calculating Principal Repayment

To find out how much of your first payment goes towards reducing the principal, you need to know your total scheduled monthly payment. Let’s assume, for our example, that the total monthly payment for this $250,000 loan at 4.5% over 30 years is approximately $1,266.71 (this amount is usually calculated using a more complex amortization formula by lenders).

- Principal Paid (Month 1) = Total Monthly Payment – Monthly Interest Payment

- Principal Paid (Month 1) = $1,266.71 – $937.50 = $329.21

After your first payment, your new outstanding principal balance would be:

- New Principal Balance = $250,000 – $329.21 = $249,670.79

For the second month, you would repeat the calculation using this new principal balance. This iterative process is what an amortization schedule illustrates, showing how the interest portion gradually shrinks and the principal portion grows with each successive payment.

Beyond the Basic Calculation: Factors Influencing Your Interest Rate

While the calculation method is standard, the actual interest rate you’re offered by a lender can vary significantly based on a multitude of factors, both personal and economic. Understanding these influences is key to securing the most favorable terms.

Credit Score

Your credit score is arguably one of the most significant personal factors determining your mortgage interest rate. Lenders use your score as an indicator of your creditworthiness and your likelihood of repaying the loan.

- Higher Credit Score (e.g., 760+): Generally translates to lower interest rates. This is because a strong credit history indicates a lower risk to the lender.

- Lower Credit Score: Will likely result in higher interest rates, as lenders perceive a greater risk of default. It’s crucial to maintain a healthy credit profile by paying bills on time, keeping credit utilization low, and checking your credit report for errors.

Down Payment

The amount of money you put down upfront for your home, known as your down payment, also plays a crucial role. A larger down payment reduces the loan-to-value (LTV) ratio, which is the amount of the loan compared to the home’s appraised value.

- Larger Down Payment (e.g., 20% or more): Leads to a lower LTV, signaling less risk to the lender and often resulting in a lower interest rate. Additionally, a 20% down payment typically allows you to avoid Private Mortgage Insurance (PMI), an extra monthly cost.

- Smaller Down Payment: Increases the LTV, meaning the lender is taking on more risk. This can lead to higher interest rates and often requires you to pay PMI, adding to your monthly housing expense.

Loan Type (Fixed vs. Adjustable-Rate)

The type of mortgage you choose has a direct bearing on your interest rate structure.

- Fixed-Rate Mortgage: The interest rate remains constant for the entire duration of the loan. This provides stability and predictability in your monthly payments, making budgeting easier. While initial fixed rates might be slightly higher than initial ARM rates, they offer protection against rising interest rates in the future.

- Adjustable-Rate Mortgage (ARM): These loans typically offer a lower initial interest rate for a set period (e.g., 3, 5, 7, or 10 years). After this introductory period, the rate adjusts periodically (e.g., annually) based on a specified market index. While ARMs can offer lower initial payments, they come with the risk of future rate increases, which could lead to significantly higher monthly payments.

Additionally, specific government-backed loans like FHA (Federal Housing Administration) and VA (Department of Veterans Affairs) loans have unique rate structures and eligibility requirements that can influence the rates offered.

Economic Factors

Beyond your personal financial profile, broader economic conditions exert a significant influence on mortgage interest rates.

- Federal Reserve Policy: The Federal Reserve’s decisions regarding the federal funds rate indirectly impact mortgage rates. When the Fed raises its target rate, borrowing costs for banks increase, which can translate to higher rates for consumers.

- Inflation: High inflation often leads to higher interest rates as lenders seek to maintain the purchasing power of their returns.

- Bond Market Yields: Mortgage rates are closely tied to the yields on U.S. Treasury bonds. When bond yields rise, mortgage rates tend to follow suit.

- Market Competition: The competitive landscape among mortgage lenders can also affect rates. In a highly competitive market, lenders might offer slightly lower rates to attract borrowers.

Practical Tools and Advanced Considerations

Beyond manual calculations and understanding influencing factors, several practical tools and advanced considerations can further refine your comprehension and management of mortgage interest.

Using Online Mortgage Calculators

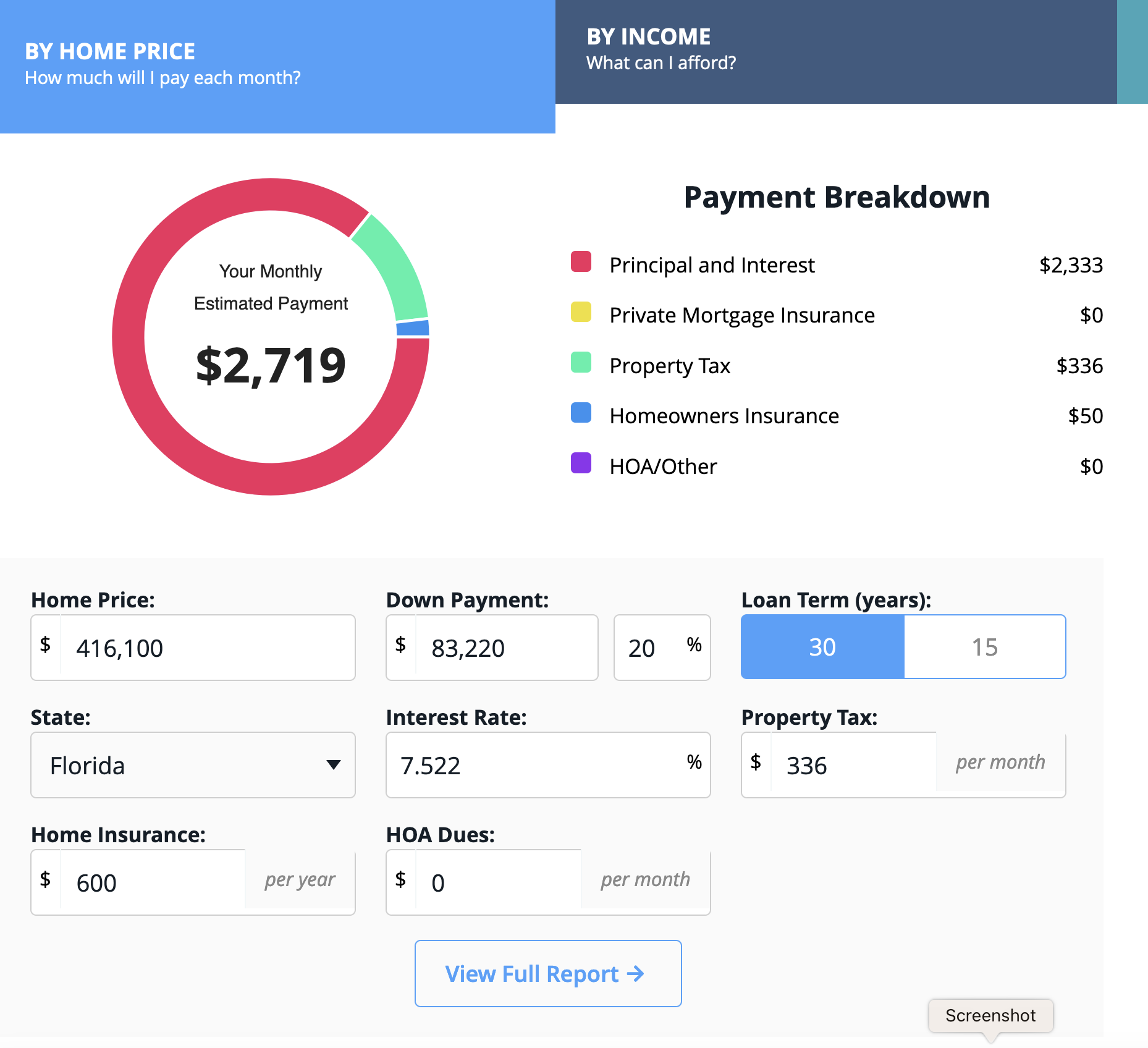

In today’s digital age, manual calculations are often unnecessary for everyday planning thanks to readily available online mortgage calculators. These tools are invaluable for quickly estimating payments and understanding loan scenarios.

- Convenience and Accuracy: Online calculators instantly provide precise figures based on complex amortization formulas, saving you time and preventing arithmetic errors.

- Required Inputs: Typically, you’ll need to input the loan amount (principal), the annual interest rate, and the loan term (in years or months).

- Provided Outputs: Most calculators will display your estimated monthly principal and interest payment, the total amount of interest you’ll pay over the life of the loan, and sometimes even a full amortization schedule. Some advanced calculators allow you to factor in property taxes, homeowner’s insurance, and PMI to give you a more complete picture of your total monthly housing cost.

Understanding APR vs. Interest Rate

It’s critical to distinguish between the nominal interest rate and the Annual Percentage Rate (APR).

- Interest Rate: This is the rate at which interest is charged on your principal loan amount. It’s the numerical percentage you typically see advertised.

- Annual Percentage Rate (APR): The APR provides a more comprehensive measure of the true cost of borrowing because it includes not only the interest rate but also most other costs associated with the loan, such as points, origination fees, mortgage broker fees, and some closing costs.

When comparing loan offers from different lenders, always compare the APRs, not just the interest rates. A lower interest rate might look appealing, but a higher APR could indicate significant upfront fees that make the loan more expensive overall.

Refinancing and Prepayments

Once you have a mortgage, your journey with interest rate management doesn’t necessarily end.

- Refinancing: This involves taking out a new mortgage to pay off your old one. People refinance for various reasons, most commonly to secure a lower interest rate (which can significantly reduce monthly payments and total interest paid), change the loan term (e.g., move from a 30-year to a 15-year mortgage to pay it off faster), or convert from an ARM to a fixed-rate mortgage. The decision to refinance should always involve a careful calculation of closing costs versus potential savings.

- Prepayments: Making extra payments towards your principal balance can be an incredibly effective strategy to reduce the total interest you pay and shorten your loan term. Even small, consistent extra payments (e.g., adding an extra $50-100 to your monthly payment, or making one extra principal-only payment per year) can shave years off your mortgage and save tens of thousands of dollars in interest. Ensure any extra payments are explicitly designated by your lender to go towards the principal, not future interest.

Conclusion

The mortgage interest rate, while seemingly just a percentage, is a pivotal factor in your financial well-being as a homeowner. Understanding “how to calculate mortgage interest rate” is not merely an academic exercise; it’s a fundamental aspect of intelligent personal finance. By grasping the relationship between principal, interest, and loan term, and by recognizing the profound impact of your credit score, down payment, loan type, and prevailing economic conditions, you empower yourself to make better decisions.

Leveraging online tools and appreciating the distinction between interest rate and APR further refines your ability to evaluate loan offers critically. Moreover, knowing the benefits of strategies like refinancing and making extra principal payments can significantly optimize your mortgage and accelerate your path to debt freedom. With this knowledge, you are not just a borrower; you are a strategic financial manager, capable of navigating the mortgage landscape with confidence and securing your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.