Understanding how your monthly salary is calculated is fundamental to effective personal finance management. It’s not simply about the gross amount you see on your offer letter; a significant portion of that figure is adjusted through taxes, deductions, and contributions before it ever lands in your bank account. This article will demystify the process, providing a clear and comprehensive guide to calculating your net monthly salary, empowering you to make informed financial decisions and budget with confidence.

Understanding the Components of Your Paycheck

Your gross salary is the initial figure agreed upon with your employer, representing the total compensation before any deductions. However, several crucial elements are subtracted from this gross amount to arrive at your net salary – the actual amount you receive. These deductions typically fall into a few key categories: statutory deductions (mandated by law), voluntary deductions (chosen by you), and employer-specific contributions. A thorough understanding of each component is the first step in accurately calculating your monthly earnings.

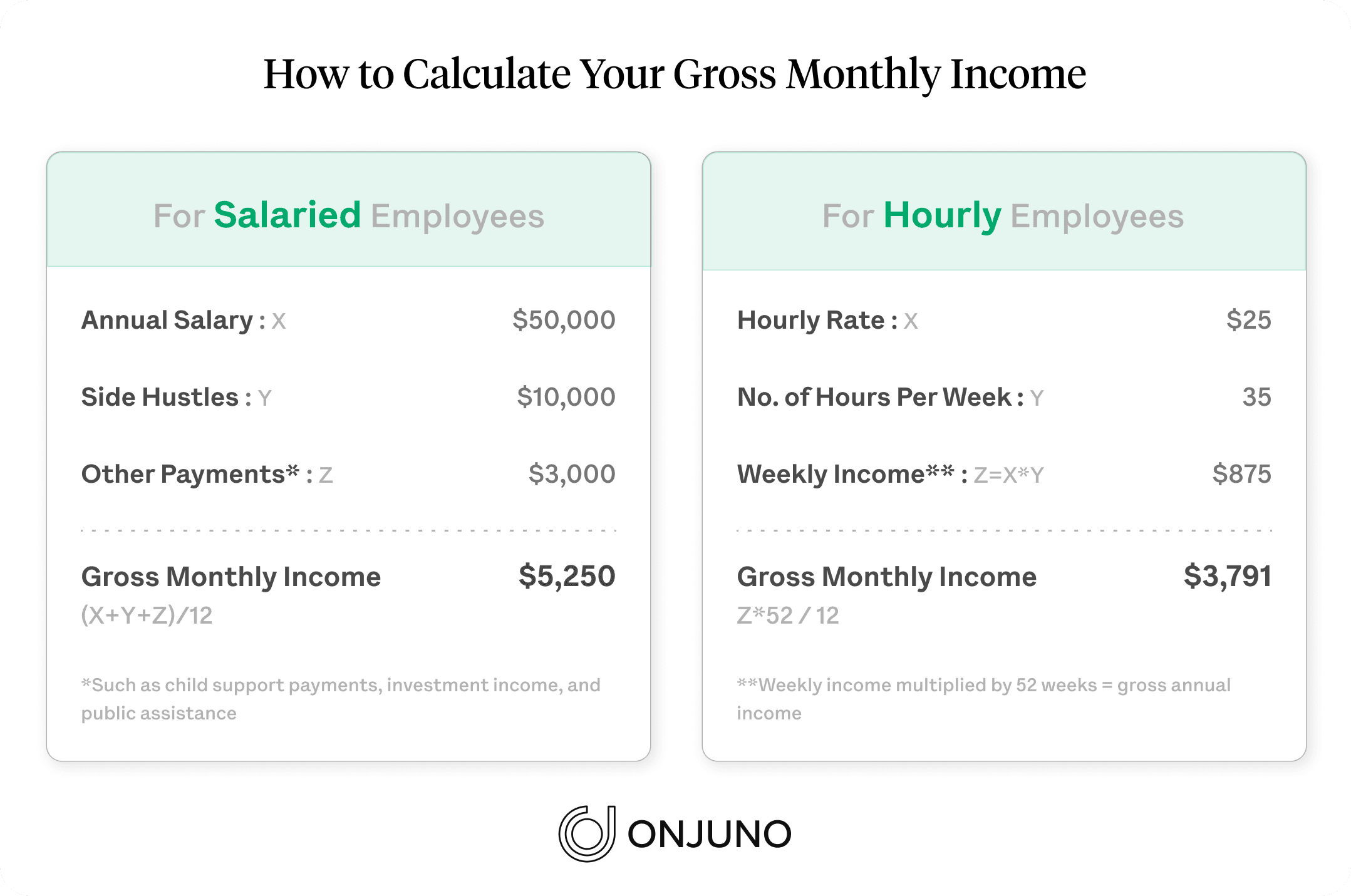

Gross Salary: The Starting Point

The gross salary is the headline figure, the number that often dictates your lifestyle expectations and financial planning. It’s the agreed-upon annual or hourly rate for your services, before any taxes or other deductions are taken out. It’s important to distinguish between your base salary and your total compensation. Your base salary is the fixed amount you receive for your primary job duties. Total compensation, on the other hand, can include bonuses, commissions, stock options, and other benefits, which may or may not be paid out monthly and can complicate a simple monthly salary calculation. For the purpose of calculating your net monthly salary, we will focus on the base salary component that forms the recurring paycheck.

Statutory Deductions: Mandated Contributions

These are the non-negotiable deductions that every employee must contribute, dictated by government regulations. The most significant statutory deduction is income tax. The amount of income tax you pay is determined by your tax bracket, which is based on your taxable income (your gross salary minus certain pre-tax deductions) and your filing status. Beyond income tax, other common statutory deductions include social security contributions (which fund programs like retirement, disability, and unemployment benefits) and, in some regions, mandatory healthcare contributions or pension schemes. These are often calculated as a percentage of your gross salary up to a certain limit.

Voluntary Deductions: Employee Choices

Voluntary deductions are those that you, as an employee, elect to have subtracted from your gross pay. These often relate to benefits or savings plans offered by your employer. Common examples include:

- Health Insurance Premiums: If you opt for employer-sponsored health, dental, or vision insurance, your share of the premium is typically deducted from your paycheck. These can be pre-tax deductions, meaning they reduce your taxable income.

- Retirement Contributions: Contributions to 401(k)s, 403(b)s, IRAs, or other employer-sponsored retirement plans are usually voluntary. These are often pre-tax, offering a dual benefit of saving for the future and lowering your current tax liability.

- Flexible Spending Accounts (FSAs) and Health Savings Accounts (HSAs): These accounts allow you to set aside pre-tax money for healthcare expenses or other qualified costs, reducing your taxable income.

- Life Insurance Premiums: If you choose to enroll in supplemental life insurance offered by your employer, the premiums will be deducted.

- Union Dues: If you are part of a union, membership dues are typically deducted from your salary.

- Garnishments: In specific legal circumstances, such as unpaid debts or child support obligations, a portion of your salary may be legally mandated to be withheld and sent directly to a creditor or government agency. These are not voluntary but are a result of legal proceedings.

Employer-Specific Contributions: Benefits Beyond Your Paycheck

While not directly deducted from your salary, it’s important to be aware of employer contributions that enhance your overall compensation package. These don’t impact your net pay calculation but are valuable benefits. Examples include:

- Employer 401(k) Match: Many employers offer to match a portion of your retirement contributions, which is essentially free money towards your retirement savings.

- Employer-Paid Health Insurance: In many cases, your employer covers a significant portion of your health insurance premiums.

- Paid Time Off (PTO): While not a cash deduction, accrued PTO represents a benefit that you are compensated for even when not actively working.

- Other Benefits: This can include things like tuition reimbursement, wellness program stipends, commuter benefits, and more.

The Calculation Process: From Gross to Net

Calculating your monthly salary involves a series of subtractions from your gross pay. The order of these subtractions can sometimes matter, especially when dealing with pre-tax versus post-tax deductions. Generally, pre-tax deductions are subtracted first, reducing your taxable income, and then taxes are calculated on the remaining amount. Post-tax deductions are then subtracted from the amount after taxes have been applied.

Step 1: Determine Your Gross Monthly Salary

If you are paid an annual salary, divide it by 12 to get your gross monthly salary. For example, an annual salary of $60,000 would result in a gross monthly salary of $5,000 ($60,000 / 12). If you are paid hourly, multiply your hourly rate by the number of hours you are scheduled to work in a month. For consistent full-time employment, this is often 40 hours per week multiplied by an average of 4.33 weeks per month (52 weeks / 12 months), or simply the actual hours worked in a given pay period. Be mindful of overtime pay, which would increase your gross monthly income for that period.

Step 2: Subtract Pre-Tax Deductions

These are deductions taken before income taxes are calculated. This is advantageous because it reduces your taxable income.

- Retirement Contributions: If you contribute to a 401(k) or similar plan, this amount is deducted pre-tax. For instance, if you earn $5,000 gross and contribute $300 to your 401(k), your taxable income for that month is now $4,700.

- Health Insurance Premiums: Your portion of health, dental, and vision insurance premiums are usually pre-tax. If your monthly premium is $200, this further reduces your taxable income. So, in our example, the taxable income becomes $4,500 ($4,700 – $200).

- FSA/HSA Contributions: Any contributions to these accounts are also typically pre-tax. If you contribute $100 to an FSA, your taxable income is reduced to $4,400 ($4,500 – $100).

Step 3: Calculate and Subtract Income Taxes

This is often the most complex part, as tax laws vary significantly by location (country, state, province) and individual circumstances.

- Federal Income Tax: This is calculated based on your taxable income (after pre-tax deductions), your tax bracket, and your filing status (single, married filing jointly, etc.). Tax brackets are progressive, meaning higher portions of your income are taxed at higher rates.

- State/Local Income Tax: Many states and some cities also levy their own income taxes, which are calculated similarly to federal income tax but with different rates and rules.

- Social Security and Medicare Taxes (in the US): These are federal taxes that fund social insurance programs. Social Security typically has a wage base limit, meaning only income up to a certain amount is subject to this tax. Medicare generally does not have a wage base limit. The rates for these taxes are fixed percentages of your taxable income.

To illustrate, let’s assume after pre-tax deductions, your taxable income is $4,400.

- If your combined federal and state income tax rate (after considering deductions and credits) is, for example, 20%, then your total income tax for the month would be $880 ($4,400 * 0.20).

- Social Security tax (e.g., 6.2% in the US up to the annual limit) on $4,400 would be approximately $272.80.

- Medicare tax (e.g., 1.45% in the US) on $4,400 would be approximately $63.80.

So, your total statutory tax deductions would be roughly $880 + $272.80 + $63.80 = $1,216.60.

Step 4: Subtract Post-Tax Deductions

These are deductions taken after all applicable taxes have been calculated and subtracted.

- Garnishment Payments: If you have a wage garnishment, this amount is deducted here.

- Other Post-Tax Benefits: Some less common benefits or contributions might be deducted post-tax.

Continuing our example, if there are no post-tax deductions, we move to the next step.

Step 5: Arrive at Your Net Monthly Salary

Your net monthly salary, often referred to as your “take-home pay,” is what remains after all deductions.

Net Salary = Gross Monthly Salary – Total Pre-Tax Deductions – Total Taxes – Total Post-Tax Deductions

Using our ongoing example:

Gross Monthly Salary: $5,000

Total Pre-Tax Deductions (401k + Health Insurance + FSA): $300 + $200 + $100 = $600

Total Taxes (Estimated Income Tax + Social Security + Medicare): $1,216.60

Total Post-Tax Deductions: $0

Net Monthly Salary = $5,000 – $600 – $1,216.60 – $0 = $3,183.40

This $3,183.40 is the amount that would ideally be deposited into your bank account each month.

Tools and Resources for Salary Calculation

While manual calculation provides a deep understanding, various tools and resources can simplify the process and offer greater accuracy, especially considering the nuances of different tax systems and benefit plans.

Payroll Software and HR Systems

Most employers utilize sophisticated payroll software. These systems automatically handle the calculation of gross pay, application of statutory and voluntary deductions, and calculation of taxes based on employee-specific information and current tax laws. Your payslip, generated by these systems, is the definitive document detailing your salary calculation. Understanding the line items on your payslip is crucial, as it provides a breakdown of all these calculations. If you are unsure about any item, your HR or payroll department is the best resource for clarification.

Online Salary Calculators

Numerous online salary calculators are available, offering a quick way to estimate your net pay. These tools typically require you to input your gross salary, location, and any voluntary deductions you make. They are excellent for budgeting and financial planning, allowing you to explore “what-if” scenarios, such as the impact of increasing your 401(k) contribution or understanding the tax implications of a pay raise. However, it’s important to note that these are estimations. They may not always account for every specific tax credit, deduction, or localized tax nuance that an official payroll system would. Always cross-reference with your official payslip for precise figures.

Financial Planning Apps and Spreadsheets

For more personalized financial management, personal finance apps and customizable spreadsheets can be invaluable. These tools allow you to track your income and expenses, budget effectively, and monitor your progress towards financial goals. By inputting your calculated net salary, you can allocate funds towards savings, debt repayment, investments, and daily living expenses. Many apps offer features that can help you forecast your income based on your known deductions and tax rates. Creating your own spreadsheet allows for complete control and customization, enabling you to build a calculation model that precisely reflects your unique financial situation.

Maximizing Your Net Income and Financial Well-being

Understanding your monthly salary calculation is not just an academic exercise; it’s a gateway to better financial decision-making. By knowing precisely how much you earn after all deductions, you can create a realistic budget, identify areas where you might be overspending, and make informed choices about contributing to benefits or savings plans.

Budgeting with Your Net Salary

Your net salary is the only figure that truly matters when it comes to your day-to-day spending and saving. Base your budget on this amount, not your gross salary. This ensures that your planned expenses do not exceed the funds you actually have available. Allocate portions of your net salary to essential expenses (housing, food, utilities), discretionary spending (entertainment, hobbies), savings (emergency fund, retirement, specific goals), and debt repayment. A well-structured budget based on your net income is the cornerstone of financial stability.

Strategic Use of Pre-Tax Deductions

Leveraging pre-tax deductions is a powerful strategy for increasing your effective take-home pay and planning for the future. By contributing to retirement accounts like a 401(k) or IRA, you not only save for your future but also reduce your current tax burden, effectively increasing the money you have available for other financial needs in the short term. Similarly, utilizing FSAs or HSAs for anticipated healthcare expenses can provide significant tax savings. Regularly review your contributions to these accounts to ensure they align with your financial goals and are optimized for tax efficiency.

Seeking Professional Financial Advice

While this guide provides a comprehensive overview, individual financial situations can be complex. Tax laws change, and personal circumstances evolve. For personalized guidance on salary optimization, tax planning, and achieving your long-term financial goals, consulting with a qualified financial advisor or tax professional is highly recommended. They can help you navigate the intricacies of your specific financial landscape, ensuring you make the most informed decisions to secure your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.