Understanding your monthly income is the cornerstone of financial literacy. Whether you are applying for a mortgage, creating a household budget, or planning an early retirement, “how much you make” is rarely a single, static number. It is a dynamic figure that varies based on your employment type, tax jurisdiction, and secondary revenue streams.

In a modern economy where traditional 9-to-5 jobs often coexist with side hustles and investment portfolios, calculating your income requires more than just a glance at a paystub. This guide provides a professional framework for determining your true monthly earnings, ensuring you have the clarity needed to make informed financial decisions.

Understanding the Core Definitions: Gross vs. Net Income

The first step in any financial calculation is distinguishing between gross and net income. These two figures serve different purposes in your financial life, and confusing them can lead to significant budgeting errors.

Calculating Gross Monthly Income

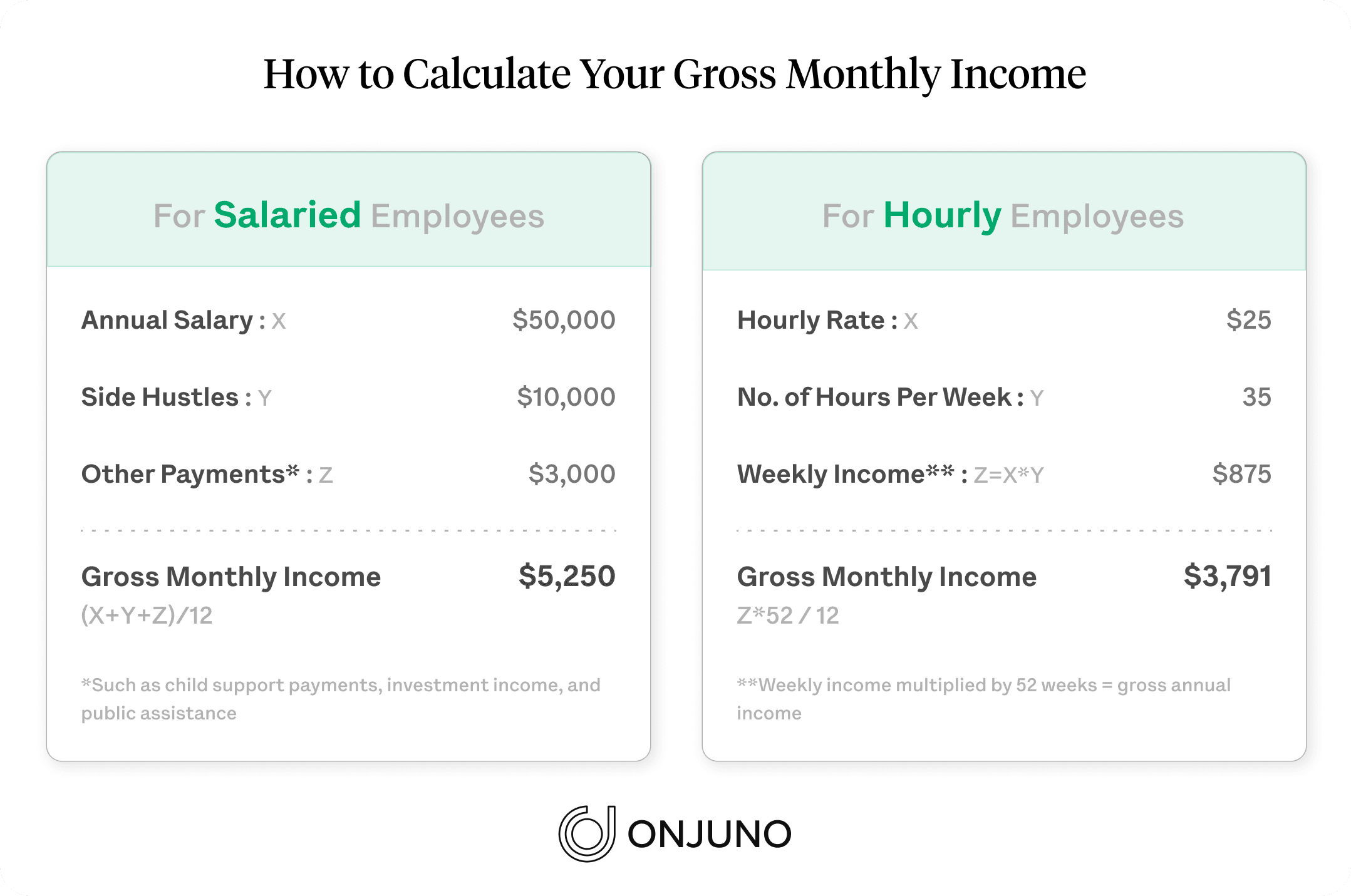

Gross monthly income is the total amount of money you earn before any taxes or deductions are taken out. For many, this is the “sticker price” of their salary. Lenders and landlords almost exclusively look at gross income to determine your debt-to-income (DTI) ratio.

If you receive an annual salary, the calculation is straightforward: divide your total yearly salary by 12. For example, an annual salary of $72,000 results in a gross monthly income of $6,000. However, for those with irregular bonuses or commissions, gross income should be calculated using a trailing average—typically over the last six to twelve months—to account for fluctuations.

Decoding Deductions and Net Take-Home Pay

While gross income is a metric for “earning power,” net income is your “spending power.” This is the amount that actually lands in your bank account after all deductions. These deductions typically fall into three categories:

- Statutory Deductions: Federal, state, and local income taxes, as well as Social Security and Medicare (FICA) contributions.

- Voluntary Benefits: Health insurance premiums, life insurance, and flexible spending accounts (FSA).

- Retirement Contributions: Pre-tax or post-tax contributions to 401(k) or 403(b) plans.

To calculate your net monthly income, subtract the sum of these deductions from your gross monthly total. Understanding this number is vital for daily living expenses, as it represents the actual liquidity available to cover your rent, groceries, and debt payments.

Methods of Calculation for Various Employment Models

Not every worker receives a predictable paycheck on the 1st and 15th of the month. The method used to calculate monthly income must adapt to the specific nature of your employment contract.

The Salaried Professional’s Formula

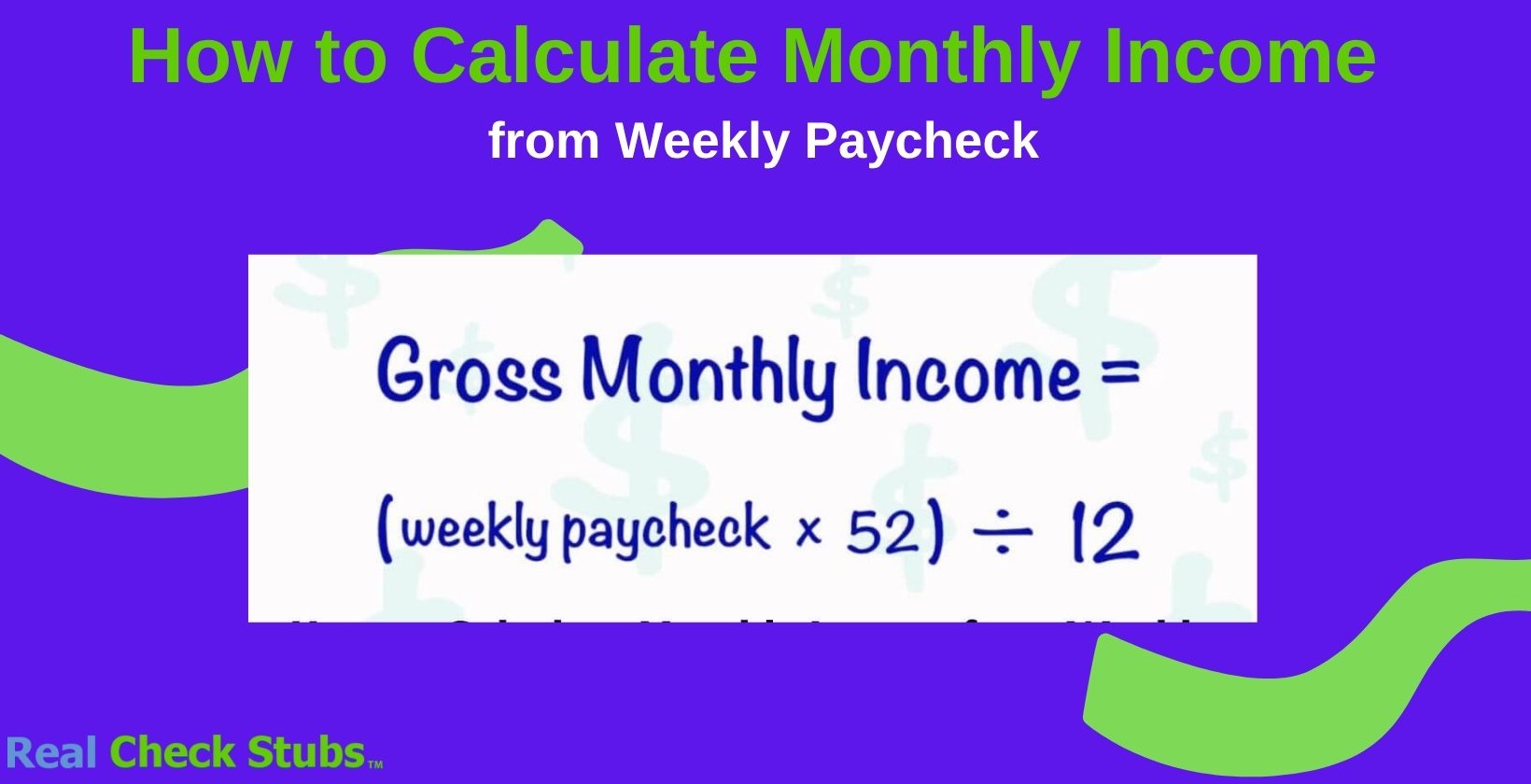

Salaried employees generally have the easiest time calculating monthly income, but the frequency of pay periods can create “hidden” income months. If you are paid semi-monthly (24 times a year), your gross monthly income is simply two paychecks.

However, if you are paid bi-weekly (every two weeks, totaling 26 times a year), you will have two months every year where you receive three paychecks instead of two. To find your true average monthly income in a bi-weekly system, multiply your gross per-paycheck amount by 26 and then divide by 12. This prevents you from underestimating your annual earnings while also helping you avoid overspending during those “triple-paycheck” months.

Hourly Wages and the “4.33 Rule”

Calculating monthly income for hourly workers requires accounting for the fact that months are longer than exactly four weeks. A common mistake is multiplying a weekly wage by four. Instead, professional financial planners use the “4.33 rule.”

Since there are 52 weeks in a year, the average month consists of 4.33 weeks (52 divided by 12). If you earn $25 per hour and work 40 hours a week, your weekly income is $1,000. Multiplying this by four gives you $4,000, but using the 4.33 rule gives you a more accurate $4,330. This extra $330 per month represents nearly $4,000 in “missing” income over a year if calculated incorrectly.

Navigating Variable Income for Freelancers and Entrepreneurs

For the self-employed, monthly income is rarely consistent. The “high-water mark” month where a large project pays out can create a false sense of security, while a “dry month” can cause panic.

The professional standard for calculating variable income is the 12-month rolling average. Total your net profit (business revenue minus business expenses) over the last 12 months and divide by 12. If you are a new freelancer with less than a year of data, use a 3-month average but subtract a 20% “safety buffer” to account for the lack of historical data and the necessity of self-employment tax set-asides.

Factoring in Passive Income and Secondary Revenue

In the modern financial landscape, your primary job is often just one piece of the puzzle. To calculate your total monthly income, you must integrate secondary streams, which are often taxed differently and may arrive on different schedules.

Investment Yields and Dividends

If you hold assets that produce regular cash flow, such as dividend-paying stocks or bonds, these should be included in your total income calculation. However, these are often quarterly payments. To find the monthly equivalent, sum the last four dividend payments and divide by 12.

It is important to note whether these dividends are being reinvested (DRIP) or taken as cash. If they are automatically reinvested, they increase your net worth but do not contribute to your monthly liquidity for budgeting. Only include them in your monthly income calculation if you intend to use them as spendable cash.

Real Estate and Rental Cash Flow

For property owners, rental income is a significant component of monthly wealth. However, the gross rent collected is not your monthly income. To find the true income from a rental property, you must subtract the “PITI” (Principal, Interest, Taxes, and Insurance) plus a maintenance reserve—usually 10% of the rent.

For example, if you collect $2,000 in rent, but your mortgage and insurance cost $1,200 and you set aside $200 for repairs, your actual monthly income from that asset is $600. Using the gross $2,000 figure would dangerously inflate your perceived financial health.

Strategic Implementation: Turning Data into Financial Progress

Once you have calculated your gross and net monthly income across all streams, the final step is applying this data to your broader financial strategy. Calculation without application is merely bookkeeping; calculation with intent is financial planning.

The Foundation of Realistic Budgeting

An accurate monthly income figure allows you to utilize the 50/30/20 rule effectively. This rule suggests allocating 50% of your net income to “needs” (housing, utilities, transportation), 30% to “wants” (entertainment, dining out), and 20% to “financial goals” (debt repayment, savings, investments).

Without an exact monthly income figure—especially for those with variable earnings—it is impossible to know if you are over-leveraged in your “needs” category. If your calculated net income is $5,000, but your fixed costs are $3,000, you are operating at 60%, which signals a need to either increase income or downsize fixed expenses.

Preparing for Quarterly Taxes and Irregular Expenses

For those with “1099” or side-hustle income, your calculated monthly income must account for tax liabilities that aren’t withheld by an employer. A professional approach involves calculating your “Effective Tax Rate.” If you earn $1,000 a month from a side hustle, you should immediately subtract roughly 25-30% for estimated taxes.

The most successful financial managers treat this tax obligation as a “negative income” line item. By calculating this ahead of time, you avoid the common pitfall of reaching the end of the fiscal year with a significant debt to the IRS that your monthly cash flow cannot support.

Conclusion: The Power of the Monthly Metric

Calculating your monthly income is not a one-time task but an ongoing financial discipline. By accurately distinguishing between gross and net, applying the 4.33 rule for hourly work, and averaging variable streams, you gain a transparent view of your economic reality. This clarity is the ultimate tool for debt reduction, wealth accumulation, and long-term financial security. When you know exactly what is coming in, you can finally take full control of what goes out.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.