Understanding the Power of Compounding

Compound interest is often hailed as the “eighth wonder of the world” by investors and financial experts alike, and for good reason. It’s the engine that drives significant wealth accumulation over time, transforming modest savings into substantial sums. At its core, compound interest means earning interest not only on your initial principal but also on the accumulated interest from previous periods. This creates an exponential growth effect that can dramatically accelerate your financial goals.

What is Compound Interest?

Imagine you deposit $1,000 into a savings account that earns 5% interest annually. After the first year, you would earn $50 in interest, bringing your total to $1,050. With simple interest, you’d continue to earn $50 each year on the original $1,000. However, with compound interest, in the second year, you would earn interest not just on the initial $1,000 but on the new total of $1,050. This means your interest earned in year two would be 5% of $1,050, which is $52.50, bringing your total to $1,102.50. This snowball effect, where your earnings generate further earnings, is the essence of compounding. The more frequently interest is compounded, the faster your money grows, making monthly compounding a particularly potent force.

Why Monthly Compounding Matters

While annual compounding is beneficial, monthly compounding takes the acceleration a step further. When interest is compounded monthly, it means that at the end of each month, the interest earned during that month is added to your principal, and the next month’s interest is calculated on this new, larger principal. This frequent recalculation allows your money to grow more quickly than if it were compounded less frequently (e.g., annually or semi-annually). Over long periods, the difference between monthly and annual compounding can be surprisingly significant, translating into thousands or even tens of thousands of dollars in additional earnings. For investors and savers, understanding and leveraging monthly compounding is key to maximizing returns and reaching financial milestones sooner.

Simple vs. Compound Interest: A Quick Comparison

To fully appreciate compound interest, it’s helpful to briefly contrast it with simple interest. Simple interest is calculated solely on the principal amount of a loan or deposit. The interest payment remains constant over the life of the investment or loan, as long as the principal does not change. For example, a $1,000 investment at a 5% simple annual interest rate will earn $50 every year, regardless of how many years pass.

Compound interest, on the other hand, calculates interest on the principal plus all accumulated interest from previous periods. This “interest on interest” effect is what makes it so powerful. While simple interest provides linear growth, compound interest provides exponential growth. For savers and investors, compound interest is almost always preferable, as it means their money works harder for them. However, it’s crucial to remember that this also applies to debt: compound interest on loans like credit cards can lead to rapidly escalating balances if not managed effectively.

The Formula for Compound Interest

Calculating compound interest, especially for monthly periods, requires a specific formula that accounts for the frequency of compounding. Understanding this formula is crucial for making informed financial decisions, whether you’re saving for retirement, investing, or evaluating loan offers.

Breaking Down the Components

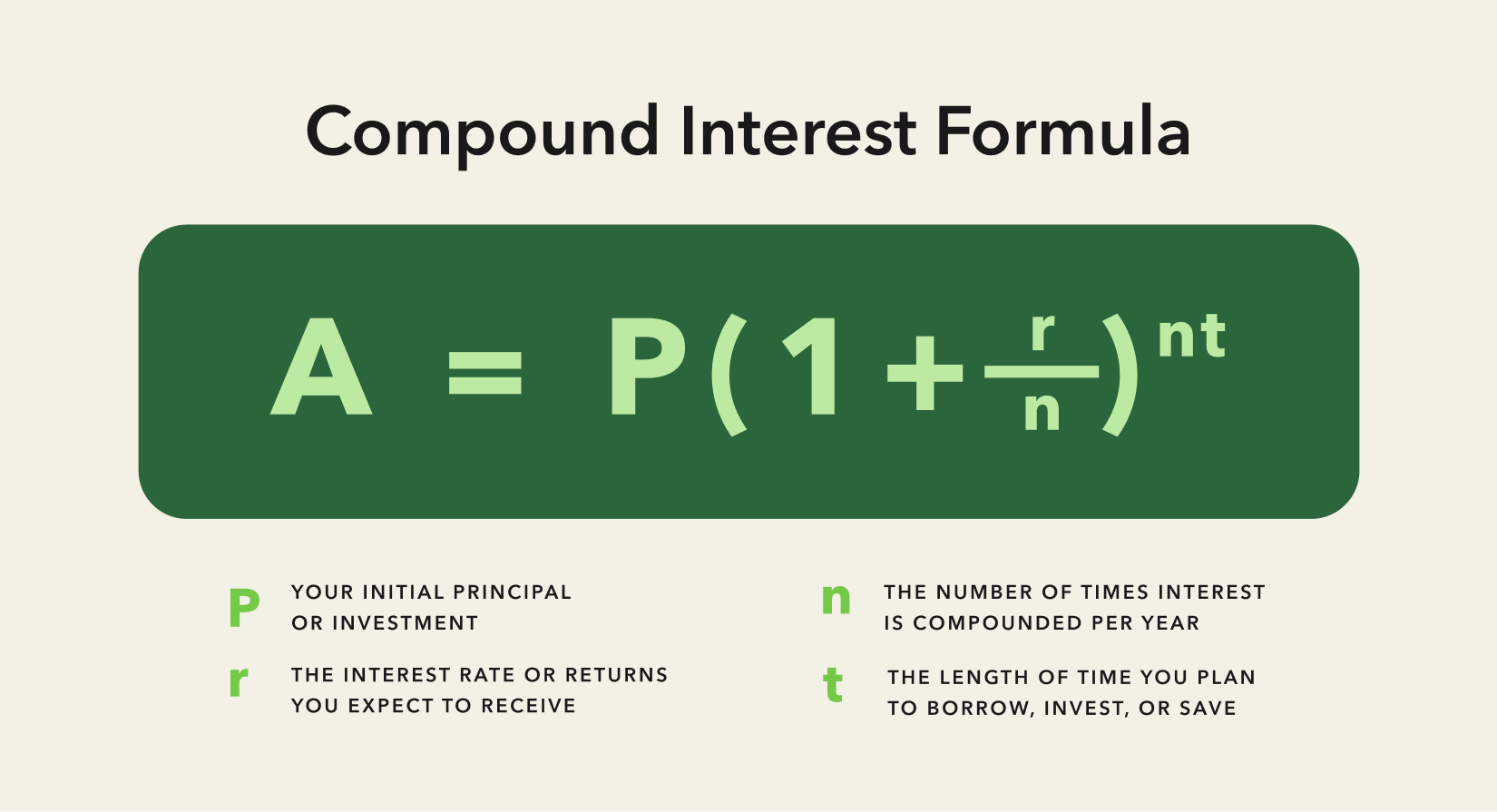

The general formula for compound interest is:

A = P (1 + r/n)^(nt)

Let’s break down each component:

- A = Future Value of the Investment/Loan, including interest: This is the total amount you will have at the end of the investment period.

- P = Principal Investment Amount (the initial deposit or loan amount): This is the starting sum of money.

- r = Annual Interest Rate (as a decimal): This is the stated interest rate per year. Remember to convert percentages to decimals (e.g., 5% becomes 0.05).

- n = Number of times that interest is compounded per year: This is where monthly compounding comes into play. For monthly compounding, ‘n’ will be 12.

- t = Number of years the money is invested or borrowed for: This is the total duration of the investment or loan in years.

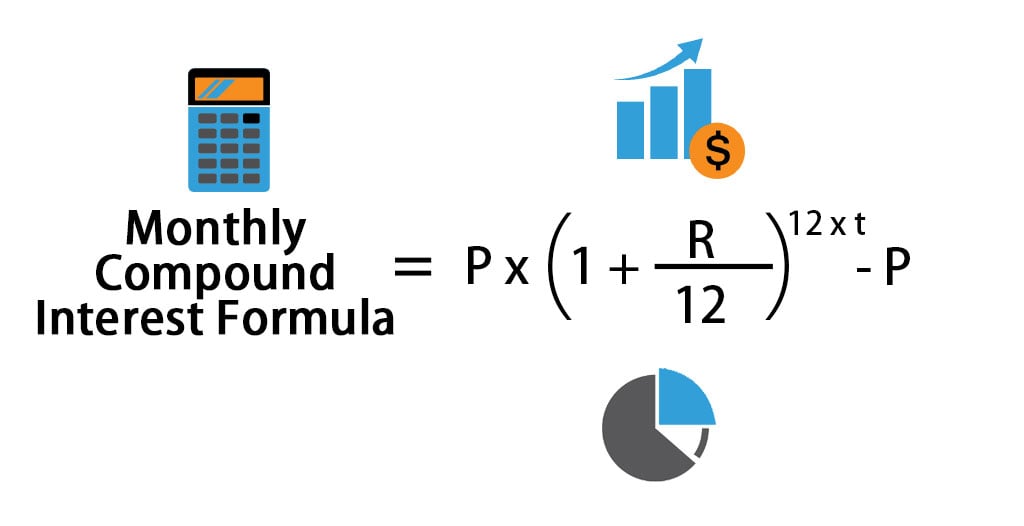

Adapting the Formula for Monthly Compounding

When the interest is compounded monthly, the value of ‘n’ becomes 12. This means the formula adjusts to reflect 12 compounding periods within each year. The annual interest rate ‘r’ is divided by 12 to get the monthly interest rate, and the number of years ‘t’ is multiplied by 12 to get the total number of compounding periods.

So, for monthly compounding, the formula looks like this:

A = P (1 + r/12)^(12t)

This modification ensures that the interest calculation accurately reflects the more frequent compounding schedule, leading to a higher future value compared to less frequent compounding over the same period and interest rate.

A Step-by-Step Calculation Example

Let’s walk through an example to illustrate how to calculate monthly compound interest.

Scenario: You invest $5,000 in a savings account that offers an annual interest rate of 6%, compounded monthly. You want to know how much your investment will be worth after 3 years.

Step 1: Identify the variables.

- P (Principal) = $5,000

- r (Annual Interest Rate) = 6% = 0.06 (as a decimal)

- n (Number of times compounded per year) = 12 (since it’s monthly)

- t (Number of years) = 3

Step 2: Plug the values into the monthly compound interest formula.

A = P (1 + r/12)^(12t)

A = 5000 (1 + 0.06/12)^(12*3)

Step 3: Perform the calculation within the parentheses first.

0.06 / 12 = 0.005

1 + 0.005 = 1.005

Step 4: Calculate the exponent.

12 * 3 = 36

Step 5: Raise the value in parentheses to the power of the exponent.

(1.005)^36 ≈ 1.196688

Step 6: Multiply the result by the principal.

A = 5000 * 1.196688

A ≈ $5,983.44

After 3 years, your $5,000 investment will grow to approximately $5,983.44 with monthly compounding.

To find the total interest earned, subtract the principal from the future value:

Interest Earned = A – P = $5,983.44 – $5,000 = $983.44.

Practical Applications and Scenarios

Understanding monthly compound interest extends beyond theoretical calculations; it has profound implications across various financial products and situations. Recognizing where and how it applies can empower individuals to make smarter choices for their money.

Savings Accounts and CDs

Most high-yield savings accounts and Certificates of Deposit (CDs) offered by banks compound interest monthly, or even daily in some cases. This is excellent news for savers because it means your money grows incrementally faster. While the difference might seem small month-to-month, over years, the compounding effect can add a significant amount to your principal. When comparing savings products, beyond just the annual percentage yield (APY), also consider the compounding frequency. An account with a slightly lower stated annual rate but more frequent compounding might, in some niche cases, yield more than one with a higher stated rate and less frequent compounding, though typically a higher APY is indicative of a better return regardless of compounding frequency. The key takeaway is that monthly compounding ensures your earnings start generating their own earnings as quickly as possible.

Investment Portfolios (Stocks, Bonds, Mutual Funds)

While direct interest calculation might be less overt than in a savings account, the principle of compounding is a cornerstone of investment growth. For investments like dividend-paying stocks or bond funds that distribute regular income, reinvesting these payouts allows you to buy more shares or units. This is the equivalent of compounding. Each new share you acquire can then generate its own dividends or capital appreciation, creating a powerful compounding loop. Over decades, this strategy of dividend reinvestment and the reinvestment of capital gains is one of the most effective ways to build substantial wealth in the stock market, amplifying returns far beyond initial contributions.

Loan Repayments (The Other Side of the Coin)

Just as compound interest can work in your favor for savings and investments, it can work against you with loans, especially those with high interest rates compounded frequently, like credit cards. Credit card interest is almost always compounded daily or monthly. If you carry a balance, the interest accrued one month is added to your principal, and then interest for the next month is calculated on this larger amount. This rapidly inflates your debt. Understanding this mechanism underscores the importance of paying off high-interest debt quickly. For mortgages and other installment loans, while interest is also compounded, the fixed payment structure helps manage the principal reduction over time, provided payments are consistent.

Retirement Planning and Long-Term Goals

For long-term financial goals such as retirement planning, a child’s education fund, or a down payment on a house, monthly compounding is an indispensable ally. The earlier you start investing, the more time your money has to compound, and the more significant the impact of this monthly growth. Even small, consistent monthly contributions, when compounded over several decades, can lead to surprisingly large sums. This illustrates the “time value of money” and highlights why early contributions are often more valuable than larger contributions made later in life. Leverage monthly compounding by automating your investments and consistently contributing to retirement accounts like 401(k)s and IRAs, which often allow for the reinvestment of earnings.

Tools and Resources for Calculation

While manual calculation is excellent for understanding the mechanics, various tools can simplify the process of calculating monthly compound interest, especially for complex scenarios or longer timeframes.

Online Compound Interest Calculators

Numerous free online compound interest calculators are available, offering quick and accurate results. These tools typically require you to input the principal, annual interest rate, compounding frequency (select “monthly”), and the investment period. Many even allow for additional monthly contributions, providing a more realistic projection for ongoing savings plans. Popular financial websites, bank sites, and investment platforms often host these calculators. They are ideal for quick estimations and comparing different scenarios without the need for manual formula application.

Spreadsheet Software (Excel/Google Sheets)

For more detailed analysis, custom scenarios, or integrating calculations into a broader financial plan, spreadsheet software like Microsoft Excel or Google Sheets is invaluable. You can easily set up the compound interest formula in a cell and then adjust variables to see immediate changes.

The basic formula in Excel/Google Sheets for future value is:

=FV(rate, nper, pmt, [pv], [type])

Where:

rate: The interest rate per period. For a 6% annual rate compounded monthly, this would be0.06/12.nper: The total number of payment periods in an annuity. For 3 years compounded monthly, this would be3*12.pmt: The payment made each period (e.g., additional monthly contributions). If there are no additional payments, this is0.pv: The present value, or the principal amount (as a negative number if it’s an outflow). So, for a $5,000 initial investment, you’d enter-5000.type: Optional.0for end of period,1for beginning.

For our earlier example (P=$5,000, r=6%, t=3 years, monthly compounding, no extra payments):

=FV(0.06/12, 3*12, 0, -5000)

This will yield approximately $5,983.44. Spreadsheets also allow you to create tables to track month-by-month growth, offering a granular view of your compounding journey.

Financial Apps and Their Features

Many personal finance and investment apps now incorporate sophisticated calculators and projections based on compound interest. Apps designed for budgeting, investing, or retirement planning often allow users to input their current savings, desired contributions, and target growth rates to project future wealth. Some apps even visually display the compounding effect over time. These tools are convenient for on-the-go tracking and provide intuitive interfaces for understanding the long-term impact of your financial decisions, helping you stay motivated and on track with your financial goals by making the invisible power of compounding visible.

Strategies to Maximize Your Compounding Gains

Understanding how to calculate monthly compound interest is merely the first step. The true power lies in strategically applying this knowledge to maximize your financial growth. A few key strategies can significantly amplify the benefits of compounding.

Start Early and Be Consistent

The single most impactful strategy for leveraging compound interest is to start as early as possible. Time is the most crucial variable in the compound interest formula. The longer your money has to grow, the more compounding cycles it undergoes, leading to exponential increases. Even small initial investments made early in life can outperform much larger investments made later. Consistency is equally vital; regular contributions, even modest ones, feed the compounding machine, ensuring a continuous principal increase upon which more interest can be earned. Automating monthly savings or investment contributions is an excellent way to ensure consistency.

Increase Your Contributions

While starting early is paramount, increasing your contributions over time further accelerates your wealth accumulation. As your income grows, try to increase the amount you save or invest each month. Every additional dollar contributed becomes part of the principal that compounds, directly increasing your future returns. Many financial advisors recommend increasing your retirement contributions whenever you get a raise or bonus, even by a small percentage point, to leverage this effect. This strategy effectively combines new capital with the power of existing compounding.

Seek Higher Interest Rates

The interest rate (r) is another critical variable. While high-interest rates often come with higher risk in investments, for savings accounts and Certificates of Deposit (CDs), comparing rates among different financial institutions can yield significant differences over time. Even a percentage point difference in the annual interest rate, especially when compounded monthly, can translate into thousands of dollars in extra earnings over long periods. Regularly review your savings accounts and low-risk investments to ensure you are earning competitive rates. For higher-risk investments, understanding the potential returns relative to the risk is crucial, as the compounding effect will amplify both gains and losses.

Reinvest Your Returns

To truly harness monthly compounding, make sure your earnings are reinvested. For savings accounts, the interest is automatically added to your principal. For investments like stocks or mutual funds that pay dividends or generate capital gains, choose to reinvest these distributions rather than taking them as cash. Reinvesting means those dividends are used to buy more shares, which then generate their own dividends and capital appreciation, creating a powerful feedback loop. This strategy ensures that your “interest on interest” is continuously put back to work, further accelerating your wealth accumulation and maximizing the long-term benefits of monthly compounding.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.