Purchasing a vehicle is one of the most significant financial commitments the average consumer will make. While the excitement of a new car is undeniable, the fiscal reality of managing a monthly payment requires precision, foresight, and a deep understanding of personal finance. Calculating a car payment is not merely about dividing the sticker price by a set number of months; it involves a complex interplay of interest rates, loan terms, taxes, and depreciation.

By mastering the mechanics of auto financing, you transition from a passive buyer to an informed negotiator. This guide provides a detailed roadmap for understanding the variables of a car loan, the mathematical formulas involved, and the strategic financial frameworks used to ensure a vehicle fits within a healthy personal budget.

Understanding the Core Components of a Car Loan

Before diving into the calculations, one must understand the variables that dictate the final number on a monthly bill. Each component acts as a lever; adjusting one will inevitably impact the others and the total cost of the debt.

Principal Amount: The Foundation of Your Loan

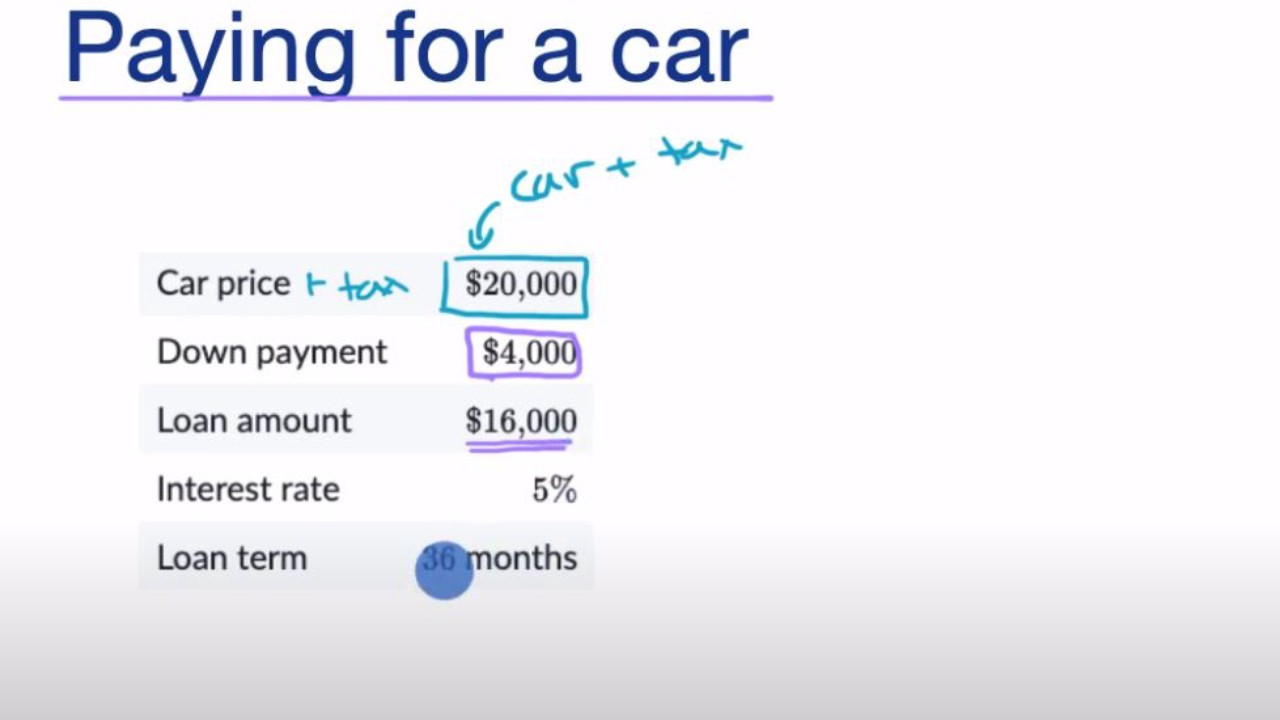

The principal is the total amount of money you are borrowing from a lender to cover the purchase price of the vehicle. However, the principal is rarely the same as the “MSRP” (Manufacturer’s Suggested Retail Price). It is the final “out-the-door” price—including sales tax, registration fees, and dealer documentation fees—minus your down payment and any trade-in equity. Reducing the principal is the most effective way to lower your monthly payment and the total interest paid over the life of the loan.

Annual Percentage Rate (APR) vs. Interest Rate

In the world of personal finance, these two terms are often used interchangeably, but they represent different costs. The interest rate is the basic cost to borrow the principal. The APR, however, is a more inclusive figure that includes the interest rate plus any additional lender fees or prepaid interest. When calculating your car payment, the APR provides the most accurate reflection of what you will actually pay. Even a 1% difference in APR can result in thousands of dollars of difference over the duration of a five-year loan.

Loan Term: Balancing Monthly Payments and Total Cost

The loan term is the duration you have to pay back the loan, typically expressed in months (e.g., 24, 36, 48, 60, or 72 months). While a longer-term loan—such as 72 or 84 months—will result in a lower monthly payment, it significantly increases the total interest paid. Furthermore, longer terms increase the risk of becoming “upside down” or having “negative equity,” where the vehicle’s value depreciates faster than the loan balance decreases.

The Step-by-Step Manual Calculation Process

While digital tools are convenient, understanding the manual calculation process reveals how interest is front-loaded and how your money is allocated over time.

The Amortization Formula Explained

Most auto loans are “simple interest” loans, which means interest is calculated based on the remaining principal balance. To find the monthly payment (M), you use the standard amortization formula:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1 ]

- P = Principal loan amount

- i = Monthly interest rate (Annual rate divided by 12)

- n = Number of months (loan term)

For example, if you borrow $30,000 at a 5% APR for 60 months, your monthly interest rate is 0.00416 (0.05 / 12). Plugging these numbers into the formula allows you to see exactly how the lender arrives at your monthly obligation.

Factoring in Sales Tax and Fees

A common mistake in car payment calculation is forgetting the “hidden” costs that are often rolled into the loan. Depending on your jurisdiction, sales tax can add 5% to 10% to the purchase price. Additionally, “doc fees,” title transfers, and registration can add several hundred to over a thousand dollars. If you do not pay these upfront, they become part of the principal, and you will pay interest on those taxes and fees for years.

The Impact of Down Payments and Trade-Ins

The down payment is your strongest tool in interest mitigation. Financially speaking, a down payment acts as an immediate “return on investment” because it reduces the amount of debt subject to interest. A trade-in works similarly; if you owe less on your current car than its market value, that “positive equity” acts as cash. By subtracting these amounts from the purchase price before applying the amortization formula, you can drastically see the reduction in your monthly commitment.

Utilizing Financial Tools for Accuracy

In the modern era, manual math serves as a foundation, but specialized tools ensure accuracy and allow for “what-if” scenario testing.

Online Car Payment Calculators

High-quality online calculators allow you to toggle variables instantly. These tools are invaluable for comparing different loan offers. A professional-grade calculator should allow you to input the vehicle price, down payment, trade-in value, interest rate, and term length. Some advanced calculators also allow for the inclusion of “sales tax by state,” providing a more realistic “out-the-door” monthly figure.

Using Spreadsheet Software (Excel/Google Sheets)

For those who prefer a granular view of their finances, spreadsheet software offers the PMT function. By typing =PMT(rate/12, nper, pv), where “rate” is your APR, “nper” is the number of months, and “pv” is the principal (expressed as a negative number), the software will return the exact monthly payment. The advantage of using a spreadsheet is the ability to create an “Amortization Schedule,” which shows exactly how much of each payment goes toward interest versus principal every month. This visual data is crucial for deciding when it might be beneficial to pay off a loan early.

Strategic Financial Considerations for Car Buyers

Calculating the payment is only half the battle; the other half is determining if that payment is a sound financial decision within the context of your broader wealth-building goals.

The 20/4/10 Rule of Thumb

Financial advisors often recommend the “20/4/10” rule to ensure a vehicle does not jeopardize your financial future:

- 20% Down: Put at least 20% down to avoid negative equity.

- 4 Years: Finance the car for no more than four years (48 months).

- 10% of Income: Total transportation costs (including insurance and fuel) should not exceed 10% of your gross monthly income.

Following this rule ensures that you are buying a car you can actually afford, rather than one the lender says you are “qualified” for.

How Credit Scores Influence Your Monthly Payment

In auto finance, your credit score is the primary determinant of your APR. Borrowers with “Super Prime” scores (780+) may qualify for 0% or 2% financing, while “Subprime” borrowers might see rates as high as 15% to 20%. On a $35,000 loan, the difference between a 3% APR and an 18% APR can be over $300 a month and over $15,000 in total interest. Before calculating a car payment, it is essential to check your credit report and, if possible, spend six months improving your score to secure a lower rate.

Total Cost of Ownership (TCO) Beyond the Payment

A car payment is not the only cost associated with a vehicle. To truly understand the financial impact, you must calculate the Total Cost of Ownership. This includes:

- Insurance Premiums: Newer, more expensive cars carry higher premiums.

- Maintenance and Repairs: European luxury brands often have significantly higher service costs than domestic or Japanese economy brands.

- Fuel/Energy: Whether it is gasoline or electricity, this is a recurring monthly cost.

- Depreciation: While not an out-of-pocket monthly cost, depreciation is the “silent killer” of wealth in auto finance.

Common Pitfalls and How to Avoid Them

Even with a calculator in hand, many consumers fall into psychological traps set by the automotive industry.

The Trap of Long-Term Loans

Lenders and dealerships often focus the conversation on the “monthly payment.” By stretching a loan to 72 or 84 months, they can make an expensive vehicle appear affordable. However, this is a financial illusion. Long-term loans often result in the borrower being “underwater”—owing more than the car is worth—for the majority of the loan’s life. This makes it impossible to sell or trade the car without paying the lender thousands of dollars out of pocket.

Ignoring the “Out-the-Door” Price

Salespeople may attempt to negotiate based solely on the monthly payment. This allows them to hide the true cost of the vehicle by adjusting the loan term or interest rate. Always negotiate the “out-the-door” price first. Once the total purchase price is locked in, you can then apply your calculations to determine the payment terms that best suit your financial strategy.

Conclusion

Calculating a car payment is a vital skill in the toolkit of personal finance. It requires a balance of mathematical accuracy and strategic planning. By understanding the components of a loan, using the right tools, and adhering to conservative financial rules like the 20/4/10 guideline, you can ensure that your next vehicle purchase is a source of mobility rather than a source of financial stress. Always remember: the goal is not just to afford the payment, but to own the asset while minimizing the cost of the debt.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.