In the world of personal and business finance, growth is the primary objective. Whether you are tracking the performance of a stock portfolio, evaluating a salary offer, or analyzing a company’s quarterly revenue, the ability to accurately calculate an increase is a fundamental skill. While the basic math may seem elementary, the implications of these calculations drive major fiscal decisions, from retirement planning to venture capital investments.

Understanding how to calculate an increase allows you to move beyond raw numbers and see the “rate of change.” This rate of change provides the context necessary to determine if a financial strategy is working or if a course correction is required. This guide explores the essential formulas, the nuances of different growth metrics, and how to apply these calculations to optimize your financial health.

The Fundamentals of Financial Growth Calculations

At its core, calculating an increase is about measuring the difference between two points in time. In finance, we rarely look at absolute numbers in isolation. For instance, a $1,000 profit might sound impressive, but its significance changes entirely depending on whether it was generated from a $10,000 investment or a $1,000,000 investment. This is why percentage increases are the universal language of finance.

The Standard Percentage Increase Formula

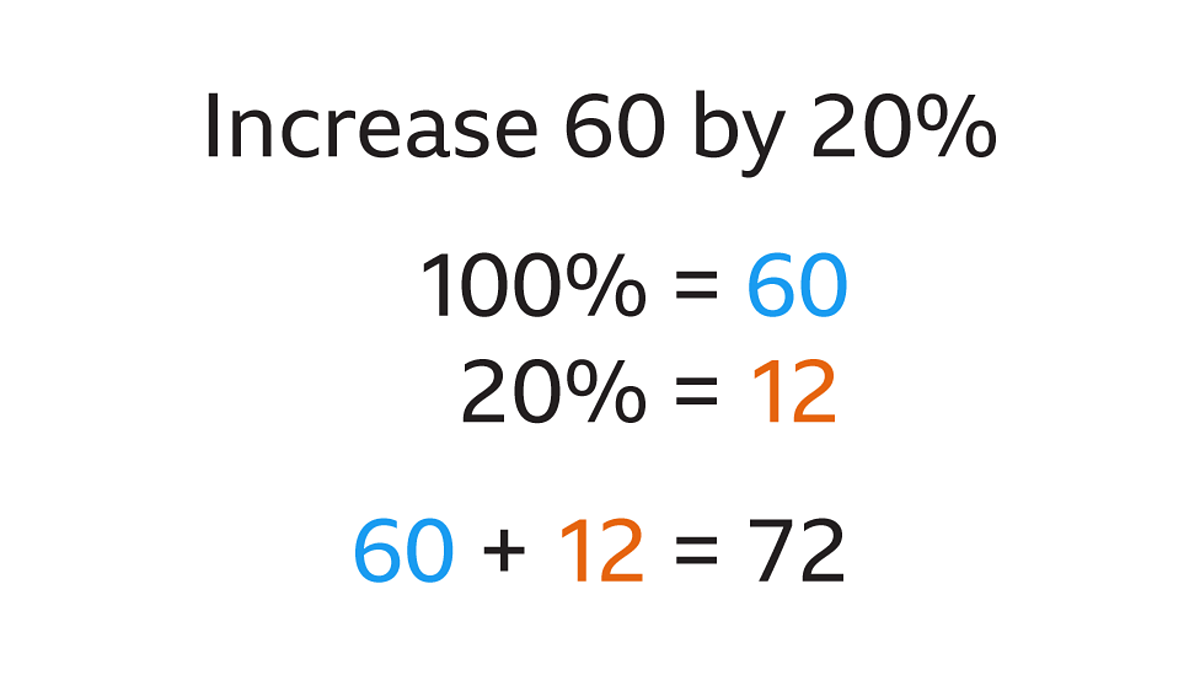

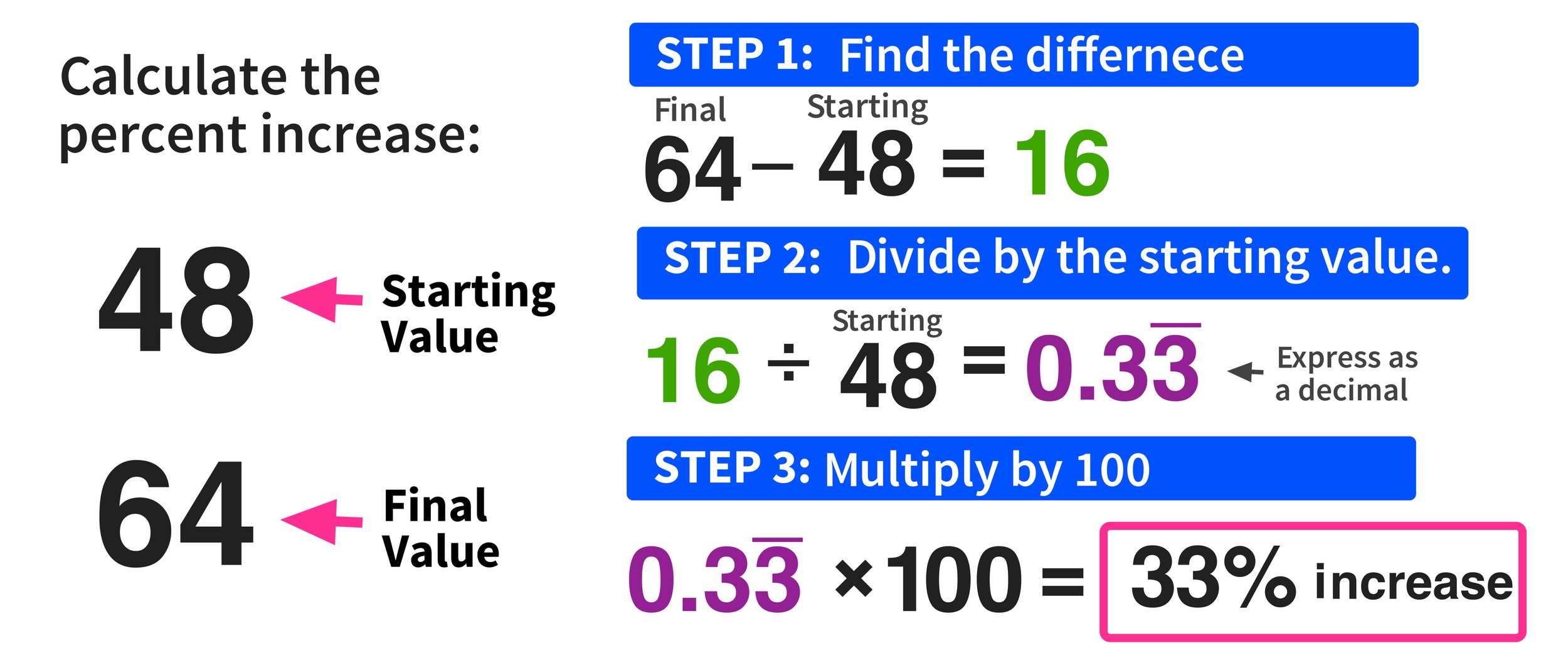

To calculate a percentage increase, you must follow a three-step mathematical process. First, subtract the original value from the new value to find the “absolute increase.” Second, divide that absolute increase by the original value. Finally, multiply the result by 100 to convert it into a percentage.

The formula is expressed as:

((New Value – Original Value) / Original Value) × 100 = Percentage Increase

For example, if your investment account grew from $5,000 to $5,750, the calculation would be:

($5,750 – $5,000) / $5,000 = 0.15.

0.15 × 100 = 15%.

Year-over-Year (YoY) vs. Month-over-Month (MoM)

When analyzing financial increases, the timeframe is just as important as the number itself. Investors and business owners typically use two main comparative lenses: Year-over-Year (YoY) and Month-over-Month (MoM).

YoY comparisons compare a specific period with the same period from the previous year. This is particularly useful in business finance because it accounts for seasonality. For example, a retail business may see a massive increase in revenue in December compared to November, but comparing December this year to December last year provides a more accurate picture of actual growth.

MoM comparisons, on the other hand, are used to track short-term volatility and immediate reactions to specific changes, such as a new marketing campaign or a shift in interest rates. While MoM provides high-frequency data, it can often be “noisy,” making it essential to use both metrics for a balanced view.

Personal Finance: Calculating Salary Raises and Cost of Living

For most individuals, the most significant “increase” they will calculate is their annual salary raise. However, a higher number on a paycheck does not always equate to increased wealth. To truly understand a salary increase, one must look at the “real” value versus the “nominal” value.

Evaluating a Merit Increase

When you receive a performance-based raise, it is vital to calculate the percentage to see how it aligns with industry standards. If you are promoted and your salary moves from $80,000 to $92,000, you have received a 15% increase.

In personal branding and career strategy, knowing your percentage increase history is a powerful tool for future negotiations. It allows you to demonstrate your rising value to an employer in concrete, mathematical terms. However, a 15% raise in a high-inflation environment carries a different weight than the same raise during a period of price stability.

Adjusting for Inflation: The “Real” Increase

Inflation is the silent eroder of purchasing power. To calculate your “Real Increase,” you must subtract the inflation rate from your nominal percentage increase.

Real Increase = Nominal Increase % – Inflation %

Suppose you receive a 5% raise, but the annual inflation rate (as measured by the Consumer Price Index) is 6%. Despite the nominal increase in your bank account, your real increase is actually -1%. This means that even with more dollars in your pocket, you can afford fewer goods and services than you could the year before. Mastering this calculation is essential for maintaining your standard of living and ensuring that your income growth outpaces the rising cost of goods.

Investment Performance and Portfolio Growth

In the realm of investing, calculating increases is how we separate winners from losers. However, simple percentage increases can be misleading when applied over long periods. Investors must use more sophisticated tools to measure the true velocity of their wealth.

Calculating Total Return on Investment (ROI)

The Return on Investment (ROI) is the most common metric used to evaluate the efficiency of an investment. In a financial context, ROI doesn’t just look at the price increase of an asset; it should also include any income generated by that asset, such as dividends from stocks or rental income from real estate.

ROI = ((Current Value of Investment + Income Received) – Cost of Investment) / Cost of Investment × 100

If you bought a stock for $1,000, sold it for $1,100, and received $50 in dividends during the holding period, your total increase is not just the 10% price appreciation, but a 15% total ROI. This comprehensive view is necessary to compare different asset classes fairly.

The Power of Compound Annual Growth Rate (CAGR)

The simple percentage increase fails to account for the “compounding effect” over many years. This is where the Compound Annual Growth Rate (CAGR) becomes indispensable. CAGR provides a smoothed annual rate of return, representing the rate at which an investment would have grown if it had grown at a steady rate each year with profits reinvested.

The formula for CAGR is:

[(Ending Value / Beginning Value)^(1 / Number of Years)] – 1

CAGR is the gold standard for comparing the performance of two different investments over varying time horizons. It allows an investor to see, for example, if a volatile tech stock that doubled over five years performed better than a steady index fund that grew by 8% consistently every year.

Business Finance: Revenue and Margin Increases

For business owners and corporate finance professionals, calculating increases is the primary way to measure the health and scalability of an enterprise. Two metrics stand above the rest: Revenue Growth and Margin Expansion.

Tracking Revenue Growth and Scalability

Revenue growth is the “top line” increase. It indicates how well a company is acquiring customers or increasing its market share. To calculate the revenue growth rate, businesses compare the current period’s sales to the previous period.

High revenue growth is often the hallmark of a successful startup, but it must be viewed in the context of “Customer Acquisition Cost” (CAC). If your revenue increases by 50%, but the cost to acquire those customers increased by 70%, the business is becoming less efficient despite the growth. Therefore, calculating the increase in revenue must always be paired with an analysis of the costs required to generate that increase.

Analyzing Profit Margin Expansion

While revenue is the top line, profit is the “bottom line.” Profit margin expansion occurs when a company’s net income grows at a faster rate than its revenue. This is a sign of operational efficiency.

If a company increases its revenue by 10% through price hikes but keeps its operating costs the same, its profit margins will expand. To calculate the increase in profit margin:

((New Margin % – Old Margin %) / Old Margin %) × 100

Margin expansion is often more valuable to investors than simple revenue growth because it proves that the company has “leverage.” It shows that for every additional dollar of sales, the company is keeping a larger slice of the pie.

Conclusion: The Strategic Value of Tracking Increases

Mastering the calculation of financial increases is more than just a mathematical exercise; it is a vital component of financial literacy. In personal finance, it helps you negotiate better salaries and protect yourself against the hidden tax of inflation. In investing, it provides the clarity needed to compare disparate assets and understand the long-term power of compounding. In business, it serves as the ultimate scorecard for efficiency and market dominance.

By consistently applying these formulas—from the simple percentage increase to the more complex CAGR—you gain a clearer perspective on your fiscal trajectory. Numbers provide the facts, but the calculation of their increase provides the story. Whether you are aiming for a comfortable retirement or building a corporate empire, knowing exactly how to measure your progress ensures that you are always moving toward your financial goals with precision and confidence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.