In an era defined by economic volatility and an ever-increasing array of spending temptations, mastering personal finance is no longer a luxury but a fundamental necessity. At the heart of sound financial management lies budgeting – a strategic process of planning how to spend and save money. Far from being a restrictive exercise, budgeting is an empowering tool that provides clarity, control, and ultimately, the freedom to achieve your financial aspirations. This comprehensive guide will demystify the art and science of budgeting, offering actionable strategies and profound insights to help you build a robust financial foundation and navigate your economic journey with confidence.

The Imperative of Financial Budgeting

Budgeting serves as the cornerstone of personal financial health, offering a panoramic view of your income and expenditures. It transforms abstract numbers into tangible insights, allowing you to make informed decisions that align with your long-term goals. Without a budget, financial decisions often become reactive, leading to stress, missed opportunities, and a perpetual cycle of financial uncertainty.

Understanding Your Current Financial Landscape

Before embarking on any budgeting journey, the crucial first step is to gain a crystal-clear understanding of your current financial situation. This involves a meticulous assessment of all incoming funds and outgoing expenses. It’s about confronting the reality of where your money is truly going, often revealing surprising patterns or hidden drains. This initial audit provides the baseline data necessary to construct a realistic and effective budget. It highlights areas of overspending, identifies opportunities for saving, and underscores the genuine capacity you have for investment or debt reduction. Embracing this truth, however uncomfortable it may initially seem, is the pivotal moment that transforms financial uncertainty into strategic planning.

The Long-Term Benefits of Disciplined Budgeting

The benefits of consistent budgeting extend far beyond simply having enough money to pay bills. A disciplined approach to managing your finances cultivates a powerful sense of control and significantly reduces financial stress. It acts as a proactive shield against unexpected financial shocks, ensuring that emergencies don’t derail your entire financial plan. Furthermore, effective budgeting is the direct pathway to achieving significant financial milestones, whether it’s buying a home, funding your children’s education, starting a business, or securing a comfortable retirement. It fosters a habit of intentional spending, enabling you to allocate resources towards what truly matters to you, transforming dreams into achievable objectives. The cumulative effect of these small, consistent actions over time builds substantial wealth and provides unparalleled peace of mind.

Core Principles of Effective Budgeting

While there are numerous budgeting methodologies, certain fundamental principles underpin every successful financial plan. Adhering to these core tenets ensures your budget is not just a theoretical exercise but a practical, living document that guides your financial decisions.

Tracking Income and Expenses: The Foundation

The absolute bedrock of any budget is accurate and consistent tracking of all money flowing in and out of your accounts. This isn’t just about knowing your salary; it’s about accounting for every side hustle income, every bonus, and every refund. Simultaneously, every single expenditure, from recurring bills like rent and utilities to daily coffees and impulse purchases, must be recorded. Many individuals underestimate the cumulative impact of small, seemingly insignificant expenses. By diligently tracking, you uncover patterns, identify leakage points, and gain a precise understanding of your financial footprint. Modern financial tools and apps have made this process incredibly streamlined, often linking directly to bank accounts and credit cards to automate much of the data collection, thereby reducing manual effort and increasing accuracy.

Categorizing Spending: Where Does Your Money Go?

Once you’ve tracked your transactions, the next vital step is to categorize them. Grouping expenses into logical categories – such as housing, transportation, groceries, entertainment, debt payments, and savings – provides invaluable insights. This categorization reveals where the bulk of your money is allocated and helps to pinpoint areas where adjustments might be necessary or desirable. For instance, you might discover that discretionary spending on dining out is significantly higher than anticipated, prompting a decision to reallocate some of those funds towards a savings goal. Clear categories transform raw data into actionable intelligence, enabling you to make conscious choices about your spending priorities rather than letting money simply slip away.

Setting Realistic Financial Goals

A budget without goals is like a ship without a destination. Effective budgeting is driven by clear, measurable financial objectives. These goals can range from short-term aims like saving for a new appliance or vacation, to medium-term targets such as paying off a credit card or building an emergency fund, and long-term ambitions like a down payment on a house or retirement planning. It’s crucial that these goals are realistic and specific. Instead of “save more money,” aim for “save $5,000 for a down payment in 12 months.” Realistic goals provide motivation, a sense of purpose for your budgeting efforts, and a framework against which to measure your progress. They transform the act of budgeting from a chore into a powerful mechanism for achieving your dreams.

Popular Budgeting Methods and Frameworks

While the core principles remain constant, various budgeting methods offer different approaches to help you manage your money. Choosing the right method often depends on your personality, financial complexity, and level of commitment.

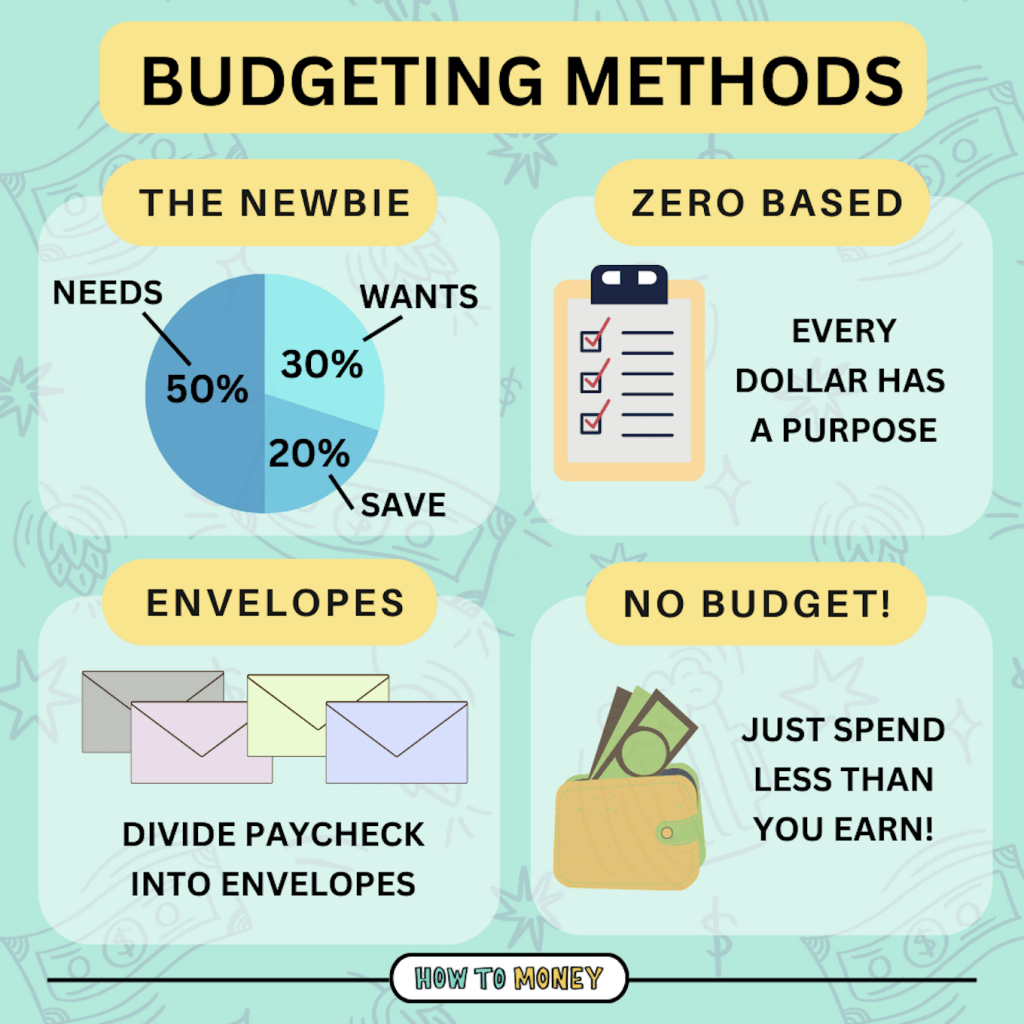

The 50/30/20 Rule: A Simple Approach

One of the most widely adopted and straightforward budgeting frameworks is the 50/30/20 rule. This method proposes dividing your after-tax income into three main categories:

- 50% for Needs: This covers essential expenses that are absolutely necessary for survival and cannot be easily cut. Examples include housing (rent/mortgage), utilities, groceries, transportation, health insurance, and minimum loan payments.

- 30% for Wants: This category includes discretionary spending that improves your quality of life but isn’t strictly essential. Examples are dining out, entertainment, hobbies, vacations, new clothes, and subscriptions.

- 20% for Savings & Debt Repayment: This portion is dedicated to building your financial future. It includes contributions to an emergency fund, retirement accounts, investment portfolios, and any additional payments towards high-interest debts beyond the minimum.

The beauty of the 50/30/20 rule lies in its simplicity and flexibility, making it an excellent starting point for those new to budgeting.

Zero-Based Budgeting: Every Dollar Has a Job

Zero-based budgeting (ZBB) is a more meticulous method where every dollar of your income is assigned a specific job – whether it’s for an expense, a saving goal, or debt repayment. The objective is that your income minus your expenses and savings equals zero. This doesn’t mean your bank account reaches zero, but rather that every dollar has been accounted for on paper. ZBB requires a higher level of discipline and attention to detail, as you must actively decide the purpose of every dollar before the month begins. This method is incredibly effective for gaining maximum control over your money, preventing overspending, and ensuring that your financial resources are precisely aligned with your priorities. It’s particularly powerful for those looking to aggressively pay down debt or build savings.

Envelope System: A Tangible Method

For those who prefer a more tactile approach or struggle with digital tracking, the envelope system can be highly effective. This method involves allocating physical cash into separate envelopes labeled with different spending categories (e.g., “Groceries,” “Entertainment,” “Transportation”). Once the cash in an envelope is depleted for the month, you cannot spend more in that category until the next budgeting cycle. While less practical for larger, recurring bills paid electronically, it’s excellent for managing discretionary spending and cultivating a strong awareness of how much cash is available for specific areas. The visual and physical nature of this system makes spending limits very tangible and immediate.

Digital Budgeting Tools and Apps

In the digital age, a plethora of software and mobile applications have emerged to simplify and automate the budgeting process. These financial tools typically link to your bank accounts and credit cards, automatically categorizing transactions, tracking spending against your budget, and providing visual reports on your financial health. Many offer features like goal tracking, bill reminders, and net worth calculations. Popular options range from free basic trackers to subscription-based services with advanced functionalities like investment tracking and financial planning. While these tools don’t replace the need for financial discipline, they significantly reduce the manual effort involved in tracking and analysis, making budgeting more accessible and engaging for many users. They are valuable resources within the “Money” niche, serving as practical extensions of financial management principles.

Strategies for Budgetary Success and Maintenance

Creating a budget is the first step; sticking to it and adapting it over time is where true financial mastery lies. Sustaining a budget requires ongoing effort, strategic adjustments, and a proactive mindset.

Regular Review and Adjustment: Staying Agile

A budget is not a static document; it’s a dynamic financial plan that needs to evolve with your life. Regularly reviewing your budget – ideally weekly or bi-weekly – allows you to assess your progress, identify discrepancies between your planned and actual spending, and make necessary adjustments. Life changes, such as a new job, a raise, an unexpected expense, or shifting priorities, all necessitate budget revisions. Staying agile and willing to adapt your budget prevents it from becoming irrelevant or unworkable. This continuous feedback loop ensures your budget remains a realistic and effective tool for achieving your goals.

Building an Emergency Fund: Your Financial Safety Net

One of the most critical components of a robust financial plan, supported by a solid budget, is an emergency fund. This dedicated savings account holds cash specifically for unforeseen circumstances like job loss, medical emergencies, or significant home/car repairs. Experts typically recommend saving three to six months’ worth of essential living expenses. An emergency fund acts as a crucial buffer, preventing you from going into debt when life inevitably throws a curveball. Prioritizing contributions to this fund within your budget provides immense financial security and peace of mind.

Tackling Debt Strategically

For many, managing existing debt is a significant part of budgeting. A well-constructed budget allows you to allocate funds strategically towards debt reduction. Popular methods include the “debt snowball” (paying off the smallest debt first for psychological wins) or the “debt avalanche” (paying off the highest interest rate debt first to save money). Whichever method you choose, your budget provides the framework to consistently make more than the minimum payments, accelerating your path to becoming debt-free and freeing up more income for savings and investments.

Automating Savings and Investments

One of the most powerful strategies for consistent financial growth is automation. By setting up automatic transfers from your checking account to your savings, investment accounts, or retirement funds immediately after you get paid, you remove the temptation to spend that money. This “pay yourself first” approach ensures that your financial goals are prioritized. Even small, consistent automated contributions accumulate significantly over time, leveraging the power of compound interest and building your wealth effortlessly.

Overcoming Common Budgeting Challenges

Even with the best intentions, budgeting can present challenges. Recognizing these obstacles and having strategies to overcome them is key to long-term success.

Dealing with Irregular Income

Budgeting can be particularly tricky for individuals with fluctuating or irregular income, such as freelancers, commission-based earners, or seasonal workers. The solution often lies in creating a “bare bones” budget that covers essential expenses, and then allocating surplus income during high-earning periods to cover lean months. Building a larger emergency fund is even more critical in these situations. Consider using an average income over several months to create a baseline budget, and then setting aside additional income into a “buffer” account to smooth out cash flow during lower-earning periods.

Avoiding Lifestyle Creep

Lifestyle creep, also known as lifestyle inflation, occurs when increased income leads to an automatic increase in spending, preventing any improvement in savings or financial security. As your income rises, it’s tempting to upgrade your living standards across the board. To combat this, consciously decide how much of any new income or raise will go towards savings, investments, or debt reduction before allocating any to discretionary spending. Maintaining a mindful approach to spending even as your income grows is crucial for building lasting wealth.

Staying Motivated and Resilient

Budgeting is a marathon, not a sprint. There will be months where you stick perfectly to your plan, and others where unexpected expenses or temptations throw you off course. The key is to avoid discouragement. View deviations not as failures, but as learning opportunities. Reassess your budget, understand what went wrong, and adjust for the next cycle. Celebrating small wins, sharing your progress with a trusted friend or partner, and regularly reminding yourself of your financial goals can help maintain motivation and foster the resilience needed to stay on track over the long haul.

Budgeting is more than just managing money; it’s about intentional living and taking control of your financial destiny. By understanding your finances, applying core principles, utilizing effective methods, and maintaining discipline, you can transform your relationship with money and build a future of financial security and abundance. The journey starts now, with a single, deliberate step towards a better financial you.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.