Applying for a mortgage is a significant milestone on the journey to homeownership, often representing the largest financial transaction an individual will undertake. It’s a process that can seem daunting, filled with terminology, paperwork, and critical decisions that will impact your financial future for decades. However, with the right preparation, understanding, and strategic approach, navigating the mortgage application landscape can be a smooth and empowering experience. This guide aims to demystify the process, providing a professional, insightful, and engaging roadmap for prospective homebuyers.

Understanding the Mortgage Landscape Before You Begin

Before diving into the specifics of an application, it’s crucial to grasp the fundamental concepts that underpin the mortgage world. A solid understanding here will empower you to make informed decisions and communicate effectively with lenders.

What is a Mortgage and Why Does it Matter?

At its core, a mortgage is a loan used to purchase or maintain a home, land, or other types of real estate. The borrower (you) agrees to pay back the lender (typically a bank or credit union) over a set period, usually 15 or 30 years, with interest. The property itself serves as collateral for the loan, meaning if you fail to make payments, the lender can seize the property through a process called foreclosure.

Why does it matter? Beyond simply enabling home purchase, a mortgage is a long-term financial commitment that affects your monthly budget, credit profile, and overall wealth accumulation. The interest rate, loan term, and type of mortgage you choose will have significant implications for the total cost of your home and your financial flexibility. Understanding this commitment from the outset is paramount.

Different Types of Mortgages: Choosing the Right Fit

The mortgage market offers a variety of loan products designed to cater to different financial situations and needs. Knowing the most common types will help you identify what might be best for you:

- Conventional Loans: These are not insured or guaranteed by a government agency. They often require a good credit score and a down payment of at least 3% (though 20% can help you avoid private mortgage insurance – PMI). They are typically the most common choice for borrowers with strong financial profiles.

- FHA Loans: Insured by the Federal Housing Administration, these loans are designed to make homeownership more accessible, especially for first-time homebuyers or those with lower credit scores. They require a minimum down payment of 3.5% and have less stringent credit requirements but come with mandatory mortgage insurance premiums (MIP) for the life of the loan.

- VA Loans: Backed by the U.S. Department of Veterans Affairs, these loans offer exceptional benefits to eligible veterans, service members, and surviving spouses. Key advantages include no down payment requirement, no private mortgage insurance, and competitive interest rates.

- USDA Loans: Guaranteed by the U.S. Department of Agriculture, these loans aim to promote homeownership in eligible rural and suburban areas. They often require no down payment for qualified low-to-moderate-income borrowers.

- Jumbo Loans: For properties that exceed conventional loan limits (which vary by region), jumbo loans are required. They typically have stricter eligibility requirements due to their larger loan amounts.

Each type has distinct advantages and disadvantages related to eligibility, down payment requirements, interest rates, and ongoing costs. Researching and discussing these options with a trusted mortgage professional is a critical early step.

Key Factors Lenders Consider

Lenders assess several critical factors to determine your eligibility and the terms of your loan. Understanding these will help you prepare:

- Creditworthiness: Your credit score and history are primary indicators of your reliability in managing debt.

- Income Stability: Lenders want to see a consistent and verifiable income source to ensure you can make monthly payments.

- Debt-to-Income Ratio (DTI): This compares your total monthly debt payments to your gross monthly income. A lower DTI indicates less risk.

- Assets and Savings: The amount of money you have for a down payment, closing costs, and reserve funds (emergency savings) is crucial.

- Property Value: The home you wish to purchase must appraise for a value that supports the loan amount.

Essential Preparations: Getting Your Finances in Order

The phrase “forewarned is forearmed” holds particular weight in mortgage applications. Proactive financial preparation can significantly improve your chances of approval, secure better terms, and streamline the entire process.

Credit Score: Your Financial Report Card

Your credit score is arguably the single most important number a lender considers. It’s a three-digit summary of your creditworthiness, derived from your credit report, which details your borrowing and repayment history. Lenders typically look for scores in the good to excellent range (generally FICO scores of 670 and above) for conventional loans to offer the best rates.

Actionable Steps:

- Check your credit report: Obtain free copies from AnnualCreditReport.com from all three major bureaus (Equifax, Experian, TransUnion).

- Dispute errors: Correct any inaccuracies that could negatively impact your score.

- Pay bills on time: Payment history is the biggest factor in your score.

- Reduce debt: Lowering credit card balances and other revolving debt can improve your credit utilization ratio, boosting your score.

- Avoid new debt: Refrain from opening new credit accounts or making large purchases on credit leading up to and during your mortgage application.

Income and Employment Stability

Lenders seek assurance that you have a stable and reliable income stream to meet your mortgage obligations. They typically prefer to see a consistent employment history, often at least two years in the same line of work or with the same employer.

Actionable Steps:

- Gather income documentation: This includes W-2s, pay stubs (recent 30-60 days), and tax returns (past two years).

- For self-employed individuals: You’ll need more extensive documentation, such as two years of tax returns, profit and loss statements, and bank statements. Be prepared for a more thorough review of your business’s financial health.

- Avoid job changes: If possible, try to avoid switching jobs or industries just before or during the application process, as this can raise red flags for lenders.

Debt-to-Income Ratio (DTI): A Critical Metric

Your DTI is a crucial metric that helps lenders gauge your ability to manage monthly payments. It’s calculated by dividing your total monthly debt payments (including the estimated new mortgage payment) by your gross monthly income. Most lenders prefer a DTI of 36% or less, though some programs allow up to 43% or even higher under specific circumstances.

Actionable Steps:

- Calculate your DTI: Sum up all your monthly debt payments (car loans, student loans, minimum credit card payments, etc.) and divide by your gross monthly income.

- Reduce existing debt: Pay down credit card balances, personal loans, or other debts to lower your monthly obligations.

- Avoid new debt: Taking on new loans or increasing credit card balances will raise your DTI, potentially jeopardizing your application.

Down Payment and Closing Costs: Saving Up

The down payment is the initial sum of money you pay upfront for the home, reducing the amount you need to borrow. Closing costs are additional fees and expenses incurred during the property transaction, typically ranging from 2% to 5% of the loan amount.

Actionable Steps:

- Start saving early: Create a dedicated savings plan for your down payment and closing costs.

- Research down payment assistance programs: Many states and local governments offer programs, especially for first-time homebuyers, to help with down payments and closing costs.

- Understand lender requirements: Different loan types have different minimum down payment requirements (e.g., 3.5% for FHA, 0% for VA/USDA, 3-20% for conventional).

- Factor in reserves: Lenders often want to see that you have several months’ worth of mortgage payments saved as a reserve after closing.

The Application Process: Step-by-Step

Once your finances are in order, you can confidently embark on the mortgage application journey. This multi-stage process requires diligence and clear communication.

Pre-Approval vs. Pre-Qualification: What’s the Difference?

These terms are often used interchangeably, but there’s a significant distinction:

- Pre-qualification: This is an informal estimate of how much you might be able to borrow based on a brief review of your financial information, often without a credit check. It’s useful for getting a general idea but carries little weight with sellers.

- Pre-approval: This is a much more thorough process where a lender reviews your credit report, verifies your income and assets, and conditionally commits to lending you a specific amount. A pre-approval letter is a powerful tool when making an offer on a home, showing sellers you are a serious and qualified buyer.

Actionable Step: Always get pre-approved before seriously shopping for a home.

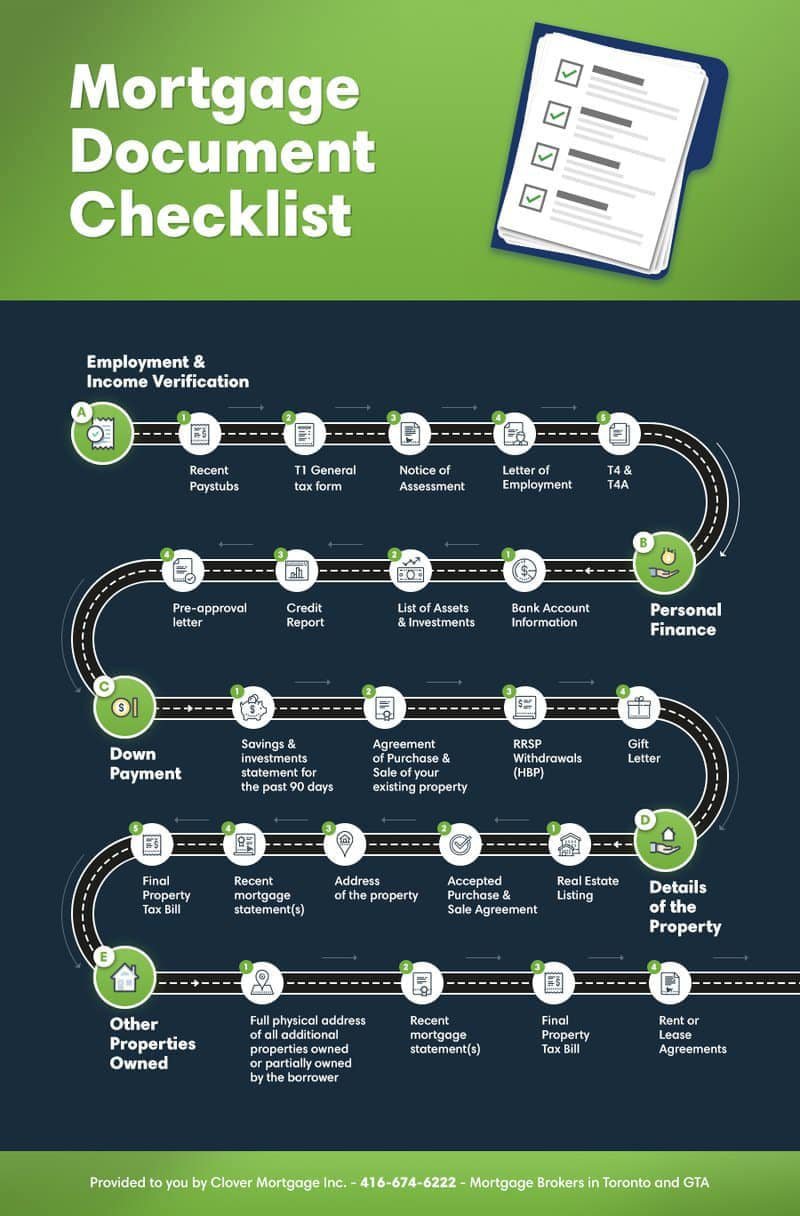

Gathering Required Documentation

Be prepared to provide an extensive array of documents. Having these organized and readily available will expedite your application.

Typical Documents Include:

- Identification: Driver’s license, Social Security card.

- Income: Recent pay stubs (30-60 days), W-2s (past two years), federal tax returns (past two years), profit and loss statements (for self-employed).

- Assets: Bank statements (past 2-3 months for all accounts), investment account statements, gift letters (if receiving down payment assistance from family).

- Debt: Statements for all loans (student, auto, personal) and credit cards.

- Housing History: Previous rental history or mortgage statements.

Submitting Your Application

With your documents in hand and having chosen a lender (or several for comparison), you’ll formally submit your application. This usually involves completing a Uniform Residential Loan Application (Form 1003). The lender will pull your credit report and begin the verification process.

Underwriting: The Deep Dive

After submission, your application moves to underwriting. This is where a mortgage underwriter meticulously reviews all your financial documents, credit history, and the property’s appraisal to assess the risk of lending to you. They are looking for consistency, stability, and adherence to lending guidelines. They may request additional information or clarification during this stage, so respond promptly.

Appraisal and Inspection

- Appraisal: The lender will order an independent appraisal of the property to ensure its value supports the loan amount. This protects both you and the lender from overpaying for the home.

- Inspection: While not strictly required by lenders, a home inspection is highly recommended. An inspector will identify any structural issues, necessary repairs, or potential problems that could impact the home’s value or your future costs. You can often negotiate with the seller based on inspection findings.

Navigating Offers and Closing the Deal

Once your application has successfully passed underwriting and the property has been appraised and inspected, you’re nearing the finish line.

Understanding Mortgage Offers and Interest Rates

Your lender will provide a Loan Estimate, detailing the loan amount, interest rate, monthly payment, and estimated closing costs. It’s crucial to compare Loan Estimates from multiple lenders to ensure you’re getting the most favorable terms. Pay close attention to:

- Interest Rate: A lower rate means lower monthly payments and less interest paid over the life of the loan.

- APR (Annual Percentage Rate): This reflects the total cost of the loan, including interest and some fees, expressed as an annual percentage.

- Points: Fees paid to the lender at closing to lower your interest rate.

- Closing Costs: Compare itemized fees across different lenders.

Closing Day: What to Expect

Closing day is when all the final documents are signed, and the ownership of the property legally transfers to you. You’ll typically meet with your real estate agent, the seller’s agent, and a closing agent (attorney or title company representative).

Key Activities:

- Reviewing the Closing Disclosure: This document outlines all the final costs and terms of your loan. You must receive it at least three business days before closing to review it thoroughly.

- Signing numerous documents: These include the promissory note (your promise to repay the loan), the mortgage or deed of trust (giving the lender a lien on the property), and various disclosures.

- Paying closing costs: You’ll typically bring a cashier’s check or wire transfer for the remaining funds needed for your down payment and closing costs.

- Receiving the keys: Once everything is signed and funds are transferred, the home is yours!

Post-Closing Responsibilities

While the excitement of closing is palpable, remember that your financial journey with your mortgage has just begun. Your responsibilities include:

- Making timely payments: This is paramount to avoiding late fees, negative credit impacts, and potential foreclosure.

- Understanding your escrow account: If you have one, your lender will collect funds for property taxes and homeowner’s insurance along with your monthly mortgage payment.

- Maintaining homeowner’s insurance: This protects your investment from damage or loss.

- Budgeting for home maintenance: Factor in ongoing costs for repairs, utilities, and general upkeep.

Common Pitfalls and Expert Tips

The mortgage application process, while structured, still presents opportunities for missteps. Being aware of these can save you time, money, and stress.

Avoiding Common Mistakes

- Changing jobs: As mentioned, maintaining employment stability is crucial.

- Making large purchases: Avoid buying a new car, furniture, or opening new credit cards. This can alter your DTI and credit score.

- Missing document requests: Respond promptly to all requests from your lender or underwriter. Delays can push back your closing date.

- Not shopping around: Compare offers from at least three different lenders to ensure you’re getting competitive rates and terms.

- Draining your savings: While a down payment is important, ensure you have an emergency fund post-closing.

- Co-signing loans for others: This adds their debt to your DTI and credit report, even if you’re not making the payments.

Seeking Professional Guidance

Navigating the complexities of mortgage application alone can be challenging. Leveraging the expertise of professionals is highly advisable:

- Mortgage Broker/Lender: These professionals can explain different loan products, help you compare rates, and guide you through the application process. A good broker can be invaluable.

- Real Estate Agent: A skilled agent can help you find suitable properties, negotiate with sellers, and recommend other professionals like inspectors and appraisers.

- Financial Advisor: If you’re planning your long-term financial health, a financial advisor can help you integrate your mortgage into your broader financial plan.

Maintaining Financial Health Post-Mortgage

Homeownership is an ongoing financial commitment. Once you have your mortgage, it’s vital to continue practicing sound financial habits:

- Regularly review your budget: Ensure your mortgage payments fit comfortably within your monthly spending.

- Build an emergency fund: Aim for 3-6 months of living expenses to cover unexpected repairs or job loss.

- Consider prepaying your mortgage: Even small extra payments can significantly reduce the total interest paid and shorten your loan term.

- Monitor your property taxes and insurance: These costs can change over time.

Applying for a mortgage is a journey that, while requiring diligence and patience, ultimately leads to the rewarding experience of homeownership. By understanding the process, preparing your finances meticulously, and seeking expert guidance, you can confidently navigate the application and secure the financing that helps turn your homeownership dreams into a tangible reality.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.