For many Americans, Social Security represents the cornerstone of their retirement strategy. Yet, despite its importance, the actual mechanics behind the monthly check remain a mystery to most. It is often viewed as a “black box” where years of payroll taxes go in, and a fixed amount comes out decades later.

In reality, the Social Security Administration (SSA) uses a specific, transparent, and highly structured mathematical formula to determine your benefits. Understanding this calculation is not just an academic exercise; it is a vital component of financial literacy that allows you to make informed decisions about when to retire, how much to save in private accounts, and how to maximize your lifetime wealth.

The Foundation: Lifetime Earnings and the AIME

Before a single dollar of benefits is calculated, the SSA looks at your entire work history. The calculation is rooted in your “covered” earnings—the income on which you paid Social Security taxes (FICA).

The 35-Year Rule

The most critical number in the Social Security formula is 35. The SSA calculates your benefit based on your highest 35 years of indexed earnings. If you have worked for more than 35 years, only the highest-earning years are used. However, if you have worked fewer than 35 years, the SSA averages in “zeros” for the remaining years.

This is a significant factor for those considering early retirement. Even a few years of part-time work or early departure from the workforce can lower your average if it results in zero-earning years being factored into the 35-year window.

Wage Indexing: Adjusting for Inflation

Because a dollar earned in 1985 had significantly more purchasing power than a dollar earned in 2024, the SSA uses “wage indexing” to bring your past earnings up to modern standards. Every year, the SSA updates the National Average Wage Index.

When you turn 60, your past earnings are “indexed” to the average wage level of that year. Earnings after age 60 are taken at face value. This ensures that the calculation reflects the relative standard of living you maintained during your working life, rather than penalizing you for the lower nominal wages of the past. Once these figures are indexed and the top 35 years are selected, they are summed and divided by 420 (the number of months in 35 years) to arrive at your Average Indexed Monthly Earnings (AIME).

From Earnings to Benefits: The Primary Insurance Amount (PIA) Formula

Once your AIME is established, the SSA applies a progressive formula to determine your Primary Insurance Amount (PIA). The PIA is the base amount you are entitled to receive if you claim benefits at your Full Retirement Age (FRA).

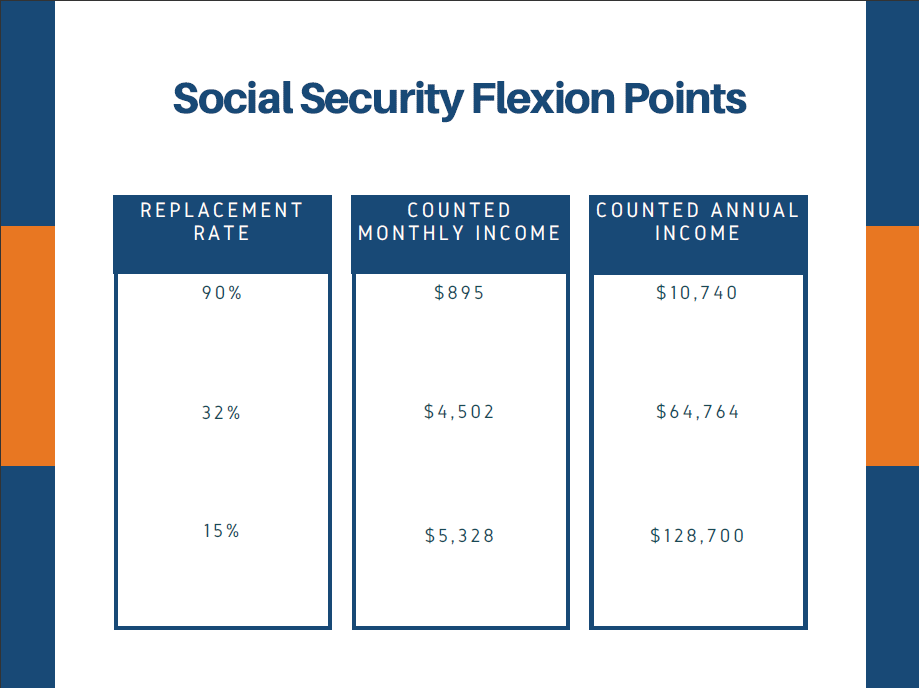

Identifying the “Bend Points”

The transition from your average earnings (AIME) to your benefit amount (PIA) is not a 1:1 ratio. Instead, the SSA uses “bend points”—specific dollar thresholds that change annually. For a worker reaching age 62 in 2024, the formula applies three distinct percentages to different portions of their AIME:

- 90% of the first $1,174 of AIME.

- 32% of AIME between $1,174 and $7,078.

- 15% of AIME exceeding $7,078.

These “bend points” are where the “bend” in the mathematical curve occurs, significantly affecting the return on your tax contributions.

The Progressive Nature of the Benefit Formula

The Social Security calculation is intentionally progressive. By applying a 90% multiplier to the first tier of earnings and only 15% to the highest tier, the system provides a higher “replacement rate” for lower-income workers.

For a low-income earner, Social Security might replace 75% of their pre-retirement income. For a high-income earner who consistently hit the taxable maximum, the replacement rate might be closer to 25% or 30%. This distinction is vital for personal finance planning; higher earners must recognize that they will need to rely more heavily on 401(k)s, IRAs, and other private investments to maintain their lifestyle in retirement.

The Impact of Timing: Full Retirement Age vs. Early or Delayed Filing

The PIA calculated in the previous step is not necessarily what you will receive. The actual monthly check depends heavily on when you choose to start receiving benefits.

Defining Full Retirement Age (FRA)

Your Full Retirement Age is the age at which you are entitled to 100% of your PIA. For anyone born in 1960 or later, the FRA is 67. For those born earlier, it ranges between 66 and 67. Filing before this age results in a permanent reduction, while filing after results in a permanent increase.

The Cost of Early Filing

You can begin taking Social Security as early as age 62. However, the SSA applies an “actuarial reduction” for every month you claim before your FRA. If your FRA is 67 and you claim at 62, your benefit is reduced by 30%.

This reduction is calculated based on a specific formula: 5/9 of 1% for each month early (up to 36 months) and 5/12 of 1% for each additional month. From a financial perspective, claiming early is often a choice made out of necessity or a belief in shorter-than-average life expectancy. However, for those with the means to wait, the monthly “penalty” for early filing is a significant loss of guaranteed, inflation-adjusted income.

The Reward of Delayed Retirement Credits

Conversely, for every month you delay claiming past your FRA (up to age 70), your benefit increases by 2/3 of 1%. This equates to an 8% simple interest increase for every year you wait.

In the current financial landscape, finding a guaranteed, inflation-indexed return of 8% per year is nearly impossible. Delaying from age 67 to age 70 results in a 24% increase over your base PIA. For many retirees, this “delayed credits” strategy serves as a powerful hedge against longevity risk—the danger of outliving your savings.

Key Factors That Can Alter Your Final Calculation

While the AIME and PIA form the core of the calculation, several external factors can shift the final number that lands in your bank account.

The Impact of Cost-of-Living Adjustments (COLA)

Social Security is one of the few retirement income sources that includes a built-in inflation hedge. Every year, the SSA evaluates the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). If prices have risen, a Cost-of-Living Adjustment (COLA) is applied to your benefits. This ensures that your purchasing power remains relatively stable even if the cost of housing, food, and healthcare increases.

Taxation of Social Security Benefits

A common surprise for retirees is that Social Security benefits can be taxable. The IRS uses a metric called “combined income” (Adjusted Gross Income + Non-taxable Interest + 1/2 of your Social Security benefits). If your combined income exceeds $25,000 (individual) or $32,000 (joint), up to 50% of your benefits may be taxable. If it exceeds $34,000 (individual) or $44,000 (joint), up to 85% may be taxable. This makes tax-bracket management in retirement essential.

The Windfall Elimination Provision (WEP) and Government Pension Offset (GPO)

For individuals who worked in “non-covered” employment—such as certain state or local government jobs where they earned a pension instead of paying into Social Security—the standard calculation changes. The WEP reduces the 90% multiplier in the first bend point, potentially lowering the monthly benefit. The GPO similarly reduces spousal or survivor benefits for those receiving government pensions. Understanding these provisions is critical for public sector employees to avoid overestimating their future income.

Strategic Planning: Maximizing Your Monthly Check

Knowing how the math works allows you to take proactive steps to influence the outcome.

Filling the 35-Year Gap

If you look at your Social Security statement and see years with zero earnings, you have a clear opportunity. Working even a few more years, even in a part-time capacity, can replace those zeros in the 35-year average. Because of the way the AIME is calculated, replacing a $0 year with a $40,000 year can have a measurable impact on your lifetime monthly benefit.

Coordinating with Your Spouse

Spousal benefits offer a unique planning opportunity. A lower-earning spouse is entitled to either their own benefit or 50% of their higher-earning spouse’s PIA, whichever is greater. Strategic coordination—such as the higher earner delaying until age 70 to maximize the survivor benefit—can significantly increase the total household wealth over the duration of retirement. This is especially important because when one spouse passes away, the smaller of the two Social Security checks disappears, leaving the survivor with only the larger one.

Conclusion

Social Security is not a fixed grant; it is a dynamic financial asset that responds to your career choices, your earnings history, and your timing. By understanding the interaction between the 35-year average, the progressive bend points of the PIA, and the credits or penalties associated with filing age, you can transform Social Security from a mystery into a manageable pillar of your financial future. Whether you choose to work longer to replace low-income years or delay filing to lock in an 8% annual increase, the power to influence your benefit lies in understanding the math behind the money.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.