Determining the exact worth of Facebook—now operating under its parent organization, Meta Platforms, Inc.—is a complex exercise in financial modeling, market sentiment analysis, and intrinsic value projection. For investors, analysts, and business enthusiasts, the question of “worth” goes far beyond the daily fluctuations of a stock ticker. It encompasses the company’s massive cash reserves, its unparalleled advertising infrastructure, and its speculative yet ambitious bets on the future of spatial computing.

As of the current fiscal landscape, Meta remains one of the most valuable companies on the planet, frequently oscillating within the elite circle of “Trillion Dollar” entities. To understand what drives this valuation, we must dissect the company through the lens of business finance, examining the metrics that professional fund managers use to decide whether the social media giant is an undervalued asset or a high-risk gamble.

The Pillars of Market Capitalization and Shareholder Equity

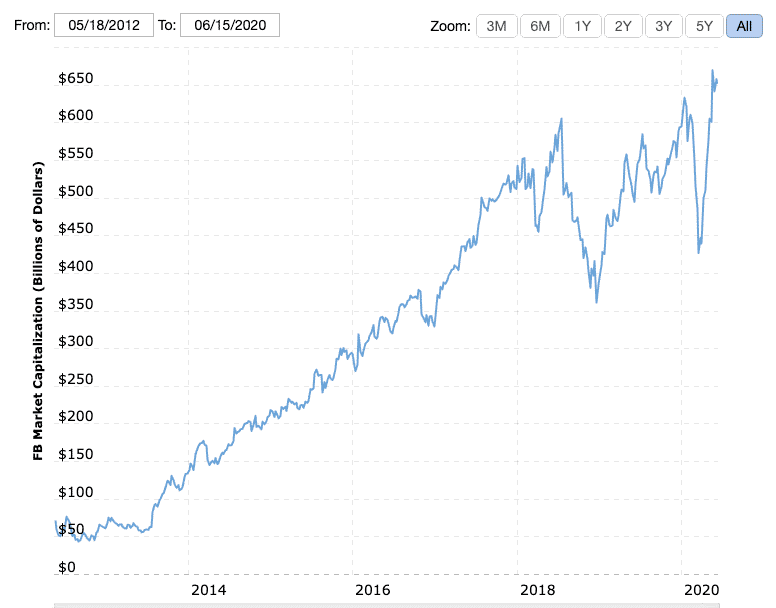

When most people ask how much Facebook is worth, they are referring to its Market Capitalization. This figure is calculated by multiplying the current share price by the total number of outstanding shares. However, market cap is often a reflection of public sentiment and future expectations rather than just current assets.

The Dynamics of the Stock Price and Ticker “META”

Meta’s stock price is the primary barometer of its perceived value. Over the last several years, we have seen extreme volatility. For instance, in 2022, the company saw a historic wipeout of market value due to concerns over privacy changes in mobile operating systems and massive spending on the “Metaverse.” Conversely, the subsequent “Year of Efficiency” led by CEO Mark Zuckerberg caused the valuation to skyrocket as the company focused on lean operations and share buybacks.

From a financial perspective, the stock price is influenced by “Earnings Per Share” (EPS). When Meta reports higher-than-expected profits, the demand for shares increases, driving up the company’s total worth. This cycle is fueled by institutional investors—mutual funds and pension funds—who hold the majority of the stock and base their “buy” or “sell” decisions on sophisticated DCF (Discounted Cash Flow) models.

Institutional vs. Retail Ownership

The distribution of ownership plays a significant role in the company’s financial stability. Institutional investors, such as Vanguard and BlackRock, provide a bedrock of capital that stabilizes the valuation. When these institutions increase their positions, it signals to the broader market that Facebook’s intrinsic value is higher than its current price.

Retail investors, on the other hand, often react to news cycles. The “worth” of the company is thus a tug-of-war between long-term financial health and short-term market psychology. To truly understand the balance sheet, one must look at “Book Value”—the total assets minus total liabilities. While Meta’s market cap is often 5 to 10 times its book value, this “premium” is what investors pay for the company’s brand power and future earnings potential.

Revenue Streams: How the Facebook Ecosystem Monetizes

A company is worth what it can earn. Facebook’s valuation is primarily supported by its status as one of the two most powerful advertising platforms in history (alongside Google). To understand the “worth,” we must look at how the company converts billions of users into billions of dollars.

Advertising Dominance in the Digital Age

Nearly 98% of Meta’s revenue is derived from digital advertising. The company’s worth is anchored in its ability to offer “Hyper-Targeting.” Because Facebook, Instagram, and WhatsApp collect vast amounts of first-party data, advertisers are willing to pay a premium to reach specific demographics.

The financial health of this segment is measured by “Ad Impressions” and the “Average Price per Ad.” Even during economic downturns, Facebook’s ad revenue tends to remain resilient because digital advertising offers a higher Return on Investment (ROI) than traditional media. This consistent cash flow is the “engine” that funds all other experimental ventures, providing a safety net for the company’s valuation.

The ARPU (Average Revenue Per User) Metric

For financial analysts, the most critical metric in Facebook’s quarterly reports is ARPU. This figure breaks down how much money the company makes from a single user. Interestingly, a user in the US or Canada is “worth” significantly more to Meta than a user in Southeast Asia or Africa, purely based on the maturity of the advertising market and the purchasing power of the demographic.

As Meta optimizes its monetization of Reels and integrates AI-driven ad placements, the ARPU continues to climb. When the market sees that Meta can squeeze more profit out of the same number of users, the company’s valuation receives a “multiple expansion,” meaning investors are willing to pay more for every dollar of profit the company generates.

The Impact of the “Metaverse” Pivot on Financial Valuation

In late 2021, the rebranding from Facebook to Meta signaled a shift in the company’s long-term financial strategy. This move initially cost the company hundreds of billions in market value as investors grew wary of the massive capital expenditures required to build a virtual reality ecosystem.

Reality Labs and Capital Expenditure

Reality Labs is the division responsible for VR headsets (Quest) and AR glasses. From a purely financial standpoint, this division has been a “money pit,” reporting billions of dollars in operating losses each quarter. For a value investor, these losses are a drag on the current worth of the company.

However, growth-oriented investors view this spending as “R&D” (Research and Development) that could lead to a monopoly on the next computing platform. If Meta succeeds in defining the “Metaverse,” the company’s current valuation will look like a bargain. The “worth” of Facebook today includes a “call option” on the future of VR/AR technology.

Diversification Beyond Traditional Social Media

The financial risk of being a “one-trick pony” (solely dependent on ads) is a major concern for Meta. To protect its valuation, the company is looking toward “Business Messaging” via WhatsApp and “On-platform Commerce.” By diversifying income streams, Meta reduces its “Beta” (volatility) and makes itself a more attractive long-term hold for conservative financial portfolios. The more successful WhatsApp is at charging businesses for customer service tools, the higher the floor for Meta’s valuation becomes.

Comparative Valuation: Facebook vs. The Magnificent Seven

To determine if Facebook is “worth” its price, we must compare it to its peers in the technology sector—companies like Apple, Microsoft, Alphabet, and Amazon. This is known as relative valuation.

P/E Ratios and Growth Projections

The Price-to-Earnings (P/E) ratio is the most common tool for this comparison. Historically, Meta has often traded at a lower P/E ratio than Apple or Microsoft. This “discount” is usually attributed to “regulatory risk” and the public’s fluctuating trust in social media.

If Meta trades at a P/E of 20 while the rest of the tech sector trades at 30, a financial analyst might argue that Facebook is “undervalued.” This suggests that for every dollar of profit Meta makes, the market is pricing it more cheaply than a dollar of profit from Google. Understanding this discrepancy is key to identifying the investment “worth” of the company.

Economic Moats and Regulatory Risks

A company’s “moat” is its ability to maintain its competitive advantage. Facebook’s moat is the “Network Effect”—the idea that the platform is valuable because everyone else is on it. This moat protects the company’s profit margins and, by extension, its valuation.

However, the “worth” is constantly threatened by regulatory intervention. Antitrust lawsuits in the US and the EU’s Digital Markets Act (DMA) represent potential liabilities. Financial models must account for these “tail risks.” If a government forced Meta to divest Instagram or WhatsApp, the sum-of-the-parts (SOTP) valuation might actually be higher than the current unified market cap, as independent entities often command different market multiples.

Conclusion: The Intrinsic Value of a Digital Empire

Ultimately, the question of “how much is Facebook worth” is answered in two ways. Numerically, it is defined by its trillion-dollar market cap, its tens of billions in annual net income, and its robust balance sheet characterized by low debt and high liquidity.

Strategically, however, its worth is defined by its dominance over human attention. In a digital economy, attention is the ultimate commodity. As long as Meta platforms continue to capture hours of daily usage from billions of people, the company’s financial valuation will remain at the top of the global food chain. Whether viewed as a value play based on its ad-revenue “cash cow” or a growth play based on its AI and Metaverse ambitions, Facebook remains a cornerstone of the modern financial landscape, possessing a scale and profitability that few companies in history have ever achieved.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.