Understanding the potential future value of your investments is a cornerstone of sound financial planning. It’s not merely a theoretical exercise; it’s a critical inquiry that empowers you to set realistic goals, make informed decisions, and navigate the complex landscape of personal finance with confidence. Whether you’re saving for retirement, a down payment on a home, your child’s education, or simply building wealth, projecting your investment’s growth allows you to visualize your future financial landscape and adjust your strategies accordingly. This article delves into the core principles, practical calculations, and influential factors that determine just how much your hard-earned money might be worth tomorrow.

The Fundamentals of Investment Growth

At the heart of every investment’s appreciation lies a set of foundational principles that dictate its trajectory. Grasping these concepts is essential before attempting any calculations or strategic planning.

Understanding Compounding: The Eighth Wonder of the World

Albert Einstein is often (perhaps apocryphally) quoted as calling compound interest the “eighth wonder of the world.” While its true origin may be debated, the power of compounding is undeniable. In simple terms, compounding is the process by which an investment’s earnings (interest or capital gains) are reinvested to generate additional earnings. It’s earning returns on your returns.

Imagine you invest $1,000 at a 5% annual interest rate. After the first year, you earn $50. With simple interest, you’d continue to earn $50 each year. With compound interest, that $50 is added to your principal, so in the second year, you earn 5% on $1,050, resulting in $52.50. While the difference seems small initially, over extended periods, the effect is exponential. The longer your money is invested and compounding, the more significant its impact becomes, turning modest initial sums into substantial wealth.

Key Variables: Principal, Time, and Interest Rate

Three primary variables intertwine to determine your investment’s ultimate worth:

- Principal (P): This is the initial amount of money you invest. The larger your principal, the larger your potential returns, assuming all other factors remain constant. Regular additional contributions also increase your effective principal over time.

- Time (t): This refers to the duration your money remains invested. As demonstrated by compounding, time is arguably the most powerful variable. Starting early, even with smaller amounts, can often outperform larger, later investments due to the extended period available for compounding.

- Interest Rate/Rate of Return (r): This is the percentage gain or loss on your investment over a specified period, typically annually. A higher consistent rate of return naturally leads to faster wealth accumulation. However, higher potential returns often come hand-in-hand with higher risk. It’s crucial to distinguish between guaranteed returns (rare in investing beyond basic savings accounts) and expected or historical average returns (common for stocks, bonds, and mutual funds).

Inflation’s Silent Impact

While focusing on growth is vital, it’s equally important to acknowledge inflation. Inflation is the rate at which the general level of prices for goods and services is rising, and consequently, the purchasing power of currency is falling. If your investments grow at 5% per year, but inflation is also 3% per year, your real rate of return (and therefore your increase in purchasing power) is only 2%. Failing to account for inflation means overestimating your future financial capacity, making it a silent but significant factor in assessing your investment’s true worth.

Calculating Your Investment’s Future Value

With the fundamentals understood, let’s explore practical ways to estimate how much your investment will be worth. These methods range from quick rules of thumb to more precise calculations.

Simple vs. Compound Interest Formulas

While simple interest is rarely used for long-term investments, understanding its formula is a good starting point:

Simple Interest (I) = P * r * t

Where P = Principal, r = annual interest rate, t = number of years.

Future Value (FV) with Simple Interest = P + I = P * (1 + r * t)

For compound interest, the formula for a single lump sum investment, compounded annually, is:

Future Value (FV) = P * (1 + r)^t

Where P = Principal, r = annual interest rate (as a decimal), t = number of years.

If interest is compounded more frequently (e.g., monthly, quarterly), the formula becomes:

FV = P * (1 + r/n)^(n*t)

Where n = number of times interest is compounded per year.

For investments with regular, additional contributions (like a monthly savings plan), the calculation becomes more complex, often requiring a future value of an annuity formula or financial calculators.

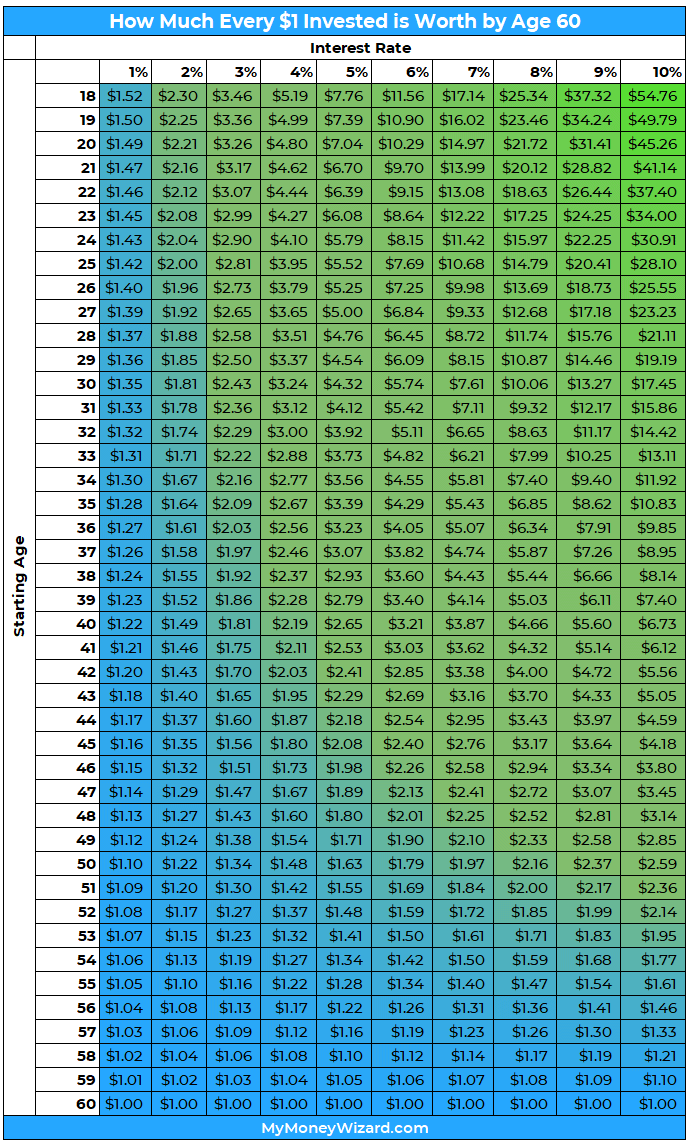

The Rule of 72: A Quick Estimation Tool

The Rule of 72 is a remarkably simple and useful heuristic for estimating the time it takes for an investment to double in value.

Years to Double = 72 / Annual Rate of Return

For example, if your investment earns an average of 8% annually, it will take approximately 72 / 8 = 9 years for your money to double. While an approximation, it offers a quick mental gauge of growth potential and highlights the power of higher returns over time.

Leveraging Online Calculators and Financial Software

For most individuals, manual calculations of compound interest, especially with recurring contributions, are cumbersome. Fortunately, a plethora of online investment calculators, financial planning apps, and spreadsheet software (like Excel or Google Sheets) are readily available. These tools allow you to input your principal, regular contributions, expected rate of return, and time horizon to generate precise future value projections. Many even allow you to factor in inflation, taxes, and varying contribution schedules, providing a more comprehensive view. These are invaluable tools for scenario planning and goal setting.

The Role of Regular Contributions

While a lump sum investment benefits immensely from compounding, the true power of consistent wealth building often comes from regular contributions. Adding funds to your investment portfolio on a monthly or annual basis significantly boosts the principal amount available to earn returns. This strategy, sometimes called “dollar-cost averaging,” also helps mitigate risk by spreading purchases over time, reducing the impact of short-term market fluctuations. When combined with compounding, regular contributions can lead to astonishing long-term results.

Factors Influencing Investment Returns

Beyond the mathematical formulas, a multitude of real-world factors can significantly impact the actual return your investment generates. Understanding these influences is crucial for developing a robust investment strategy.

Market Volatility and Risk Tolerance

Financial markets are inherently volatile. Prices of stocks, bonds, and other assets fluctuate daily, driven by economic news, corporate performance, geopolitical events, and investor sentiment. This volatility means that your actual annual return might differ significantly from your expected average return in any given year.

Your personal risk tolerance—your ability and willingness to stomach these fluctuations without panic selling—plays a critical role. High-growth investments (like growth stocks) tend to be more volatile but offer higher potential returns, while lower-risk investments (like government bonds) offer more stability but generally lower returns. Aligning your investment choices with your risk tolerance is vital for long-term success.

Asset Allocation and Diversification Strategies

“Don’t put all your eggs in one basket” is a timeless investment adage. Asset allocation refers to how you divide your investment portfolio among different asset classes, such as stocks, bonds, real estate, and cash equivalents. Diversification involves spreading your investments within each asset class (e.g., investing in various industries, company sizes, or geographies within stocks).

The goal of diversification is to reduce overall portfolio risk. When one asset class or sector performs poorly, another might perform well, balancing out returns. A well-diversified portfolio, strategically allocated based on your age, goals, and risk tolerance, can help smooth out returns and improve your chances of achieving your long-term objectives.

Fees, Taxes, and Their Erosion of Returns

Every dollar paid in fees or taxes is a dollar that doesn’t compound for you. Investment fees can include management fees for mutual funds or ETFs, trading commissions, advisory fees, and administrative charges. Even seemingly small percentages can accumulate significantly over decades, silently eroding your returns. It’s crucial to be aware of all fees associated with your investments and choose cost-effective options where possible.

Taxes on investment gains (capital gains, dividends, interest) also reduce your net returns. Understanding tax-advantaged accounts (like 401(k)s, IRAs, HSAs in the US, or ISAs in the UK) can significantly boost your after-tax returns by deferring or eliminating taxes on growth. Strategic tax planning is an integral part of maximizing your investment’s worth.

Economic Conditions and Global Events

The broader economic environment and global events exert considerable influence on investment performance. Factors like interest rates set by central banks, inflation rates, GDP growth, employment figures, geopolitical conflicts, technological advancements, and even pandemics can all impact corporate profits, consumer spending, and investor confidence, thereby affecting asset prices. While individual investors cannot control these macro factors, being aware of them and understanding their potential implications can help in making informed decisions and adjusting strategies.

Practical Steps to Maximize Your Investment’s Worth

Understanding the theory is one thing; putting it into practice effectively is another. Here are actionable steps to enhance your investment’s future value.

Start Early, Invest Consistently

This is perhaps the single most impactful piece of advice. The power of compounding makes time your greatest ally. Even small amounts invested early can grow into substantial sums due to the extended period available for earnings to earn more earnings. Once you start, commit to consistent contributions. Automate your investments to remove the temptation to skip a month, ensuring you benefit from dollar-cost averaging and continuous growth.

Embrace Diversification Across Asset Classes

Resist the urge to chase hot stocks or put all your money into a single asset. Build a diversified portfolio that spreads your investments across different asset classes (stocks, bonds, real estate, etc.) and within those classes (e.g., large-cap, small-cap, international stocks; government, corporate bonds). Rebalance your portfolio periodically to maintain your desired asset allocation as market values shift.

Minimize Fees and Taxes Where Possible

Be diligent about understanding and minimizing the fees associated with your investments. Opt for low-cost index funds or ETFs over actively managed funds with high expense ratios, especially for core holdings. Utilize tax-advantaged retirement accounts to defer or avoid taxes on investment growth, which allows more of your money to compound untouched by the taxman until withdrawal (or entirely in some cases).

Reinvesting Dividends and Earnings

Many investments, particularly stocks and mutual funds, pay out dividends or generate earnings that could be distributed. Opting to automatically reinvest these dividends and earnings back into the investment itself is a powerful way to accelerate compounding. Each reinvested dividend essentially purchases more shares, which then generate their own dividends, creating a virtuous cycle of growth.

Calculating how much your investment will be worth is more than just a numbers game; it’s an exercise in strategic planning, disciplined execution, and continuous learning. By understanding the core principles of compounding, diligently calculating potential future values, acknowledging the myriad influencing factors, and taking proactive steps to optimize your portfolio, you empower yourself to build significant wealth over time and achieve your most ambitious financial aspirations. The journey to financial freedom begins with asking, and answering, “how much will my investment be worth?”

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.