The annual ritual of filing taxes often comes with a burning question: “How much will I receive in my tax return?” For many, a tax refund isn’t just a pleasant surprise; it’s a significant financial event, representing a potential boost to savings, a means to pay down debt, or an opportunity for a much-needed indulgence. Yet, the journey from submitting your return to seeing that direct deposit hit your account can be shrouded in mystery for those unfamiliar with the underlying mechanisms. Understanding how your refund is calculated, what factors influence its size, and how to accurately estimate it can demystify the process and empower you to make more informed financial decisions throughout the year.

This comprehensive guide will demystify the tax refund process, helping you understand not only the “how much” but also the “why” behind your tax return amount. We’ll delve into the foundational concepts, explore the intricate factors at play, equip you with strategies for estimation, and discuss how to optimize your financial strategy for both current and future tax seasons.

Understanding the Basics of Your Tax Refund

Before we can estimate or discuss the amount, it’s crucial to grasp what a tax refund truly represents and how it differs from your overall tax liability. This foundational knowledge is key to making sense of your annual tax filing.

What is a Tax Refund, Really?

In its simplest terms, a tax refund is money you get back from the government because you overpaid your taxes throughout the year. Think of it as an interest-free loan you’ve given the government. Each payday, your employer withholds a portion of your earnings and sends it to the IRS (and often your state tax agency). This withholding is an estimate of the income taxes you’ll owe for the year. If the total amount withheld throughout the year, plus any estimated tax payments you made, exceeds your actual tax liability as determined when you file your return, the government owes you a refund.

It’s a common misconception that a large refund indicates a financial windfall. In reality, it often means you allowed too much of your paycheck to be withheld. While getting a refund feels good, from a purely financial planning perspective, having too much withheld means you’re missing out on having that money available for savings, investments, or spending throughout the year.

The Difference Between a Refund and a Tax Liability

Your tax liability is the total amount of tax you legally owe for the year, based on your income, deductions, and credits. It’s the final bill. Your tax refund, on the other hand, is the difference between the total amount of tax you’ve already paid (through withholdings or estimated payments) and your actual tax liability.

- If Payments > Liability: You get a refund.

- If Payments < Liability: You owe additional tax.

- If Payments = Liability: You owe nothing and get no refund.

Understanding this distinction is fundamental. The goal of effective tax planning isn’t necessarily to get the largest possible refund, but to align your withholdings and payments as closely as possible with your actual tax liability, minimizing both overpayments and underpayments.

Key Components Influencing Your Initial Withholding

The amount of tax withheld from your paycheck is determined primarily by the information you provide on your Form W-4, Employee’s Withholding Certificate. When you start a new job or wish to adjust your withholdings, you complete this form, indicating factors such as:

- Marital Status: Single, Married Filing Jointly, Married Filing Separately, Head of Household, or Qualifying Widow(er). This impacts standard deduction amounts and tax bracket thresholds.

- Number of Dependents: Primarily children under 17, which can qualify you for the Child Tax Credit.

- Other Income: If you have income from other jobs, self-employment, or investments, you might want to adjust your withholding to avoid underpaying.

- Deductions and Credits: You can estimate other deductions (like student loan interest or itemized deductions) and credits you expect to claim, which can reduce your withholdings.

The more allowances or adjustments you claim on your W-4, the less tax will be withheld. Conversely, fewer allowances or electing for additional withholding will mean more tax is taken out, increasing the likelihood of a refund.

Decoding the Factors That Determine Your Refund Amount

The final calculation of your tax refund is a complex interplay of various financial elements throughout the year. Understanding these factors will give you a clearer picture of why your refund is what it is.

Income and Withholdings: The Primary Drivers

Your total gross income for the year is the starting point. This includes wages, salaries, bonuses, tips, interest, dividends, capital gains, rental income, and more. From this, certain adjustments are made to arrive at your Adjusted Gross Income (AGI). Your AGI is a critical number as many deductions and credits are limited based on it.

As discussed, your withholdings from your paycheck are the main way you prepay your taxes. If these withholdings are significantly higher than your eventual tax liability, a larger refund is imminent. Conversely, if your withholdings are too low, you might owe additional tax or receive a smaller refund.

Deductions: Lowering Your Taxable Income

Deductions reduce the amount of your income subject to tax. They don’t directly reduce your tax bill dollar-for-dollar; rather, they reduce the income that your tax rate is applied to. There are two main types:

- Standard Deduction: A fixed dollar amount that nearly everyone can claim. The amount varies based on your filing status and whether you are blind or over 65. For many taxpayers, the standard deduction provides a greater tax benefit than itemizing.

- Itemized Deductions: If your eligible expenses (such as state and local taxes, mortgage interest, charitable contributions, and medical expenses exceeding a certain AGI threshold) exceed the standard deduction, you can choose to itemize. This requires careful record-keeping.

By reducing your taxable income, deductions effectively lower your overall tax liability, increasing the potential for a refund if your withholdings remain constant.

Credits: Directly Reducing Your Tax Bill

Tax credits are far more powerful than deductions because they directly reduce the amount of tax you owe, dollar-for-dollar. For example, a $1,000 credit reduces your tax bill by $1,000. There are two main categories of credits:

- Nonrefundable Credits: These can reduce your tax liability to zero, but you won’t get any money back if the credit amount exceeds your tax liability. Examples include the Child and Dependent Care Credit, Education Credits, and the Credit for Other Dependents.

- Refundable Credits: These can not only reduce your tax liability to zero but can also result in a refund even if you don’t owe any tax. The most common refundable credits include the Earned Income Tax Credit (EITC), the refundable portion of the Child Tax Credit (Additional Child Tax Credit), and the Premium Tax Credit (for health insurance purchased through the marketplace).

These credits can significantly impact your refund amount, especially refundable ones, which are often a major contributor to large refunds for eligible low- and moderate-income taxpayers.

Life Changes and Their Impact on Your Refund

Your personal and financial circumstances are rarely static, and significant life events can have a profound impact on your tax situation and, consequently, your refund:

- Marriage or Divorce: Changes in filing status can drastically alter standard deduction amounts, tax bracket applications, and eligibility for certain credits.

- Birth or Adoption of a Child: This often triggers eligibility for the Child Tax Credit and potentially other dependent-related credits or deductions.

- Buying or Selling a Home: Homeownership brings potential deductions for mortgage interest and property taxes, while selling a home can involve capital gains or losses.

- Job Changes or Unemployment: A change in income level, switching jobs, or periods of unemployment will directly affect your total income and withholdings.

- Retirement: Income sources typically shift, and new deductions or credits might become available (e.g., retirement savings contributions).

- Education Expenses: Paying for higher education can make you eligible for education credits or deductions for student loan interest.

It’s crucial to update your W-4 with your employer when major life changes occur to ensure your withholdings accurately reflect your new tax situation.

Strategies for Estimating Your Tax Return Accurately

While the exact refund amount is only known after filing, several tools and methods can help you get a reasonable estimate throughout the year or as you prepare to file.

Leveraging Online Tax Software Tools

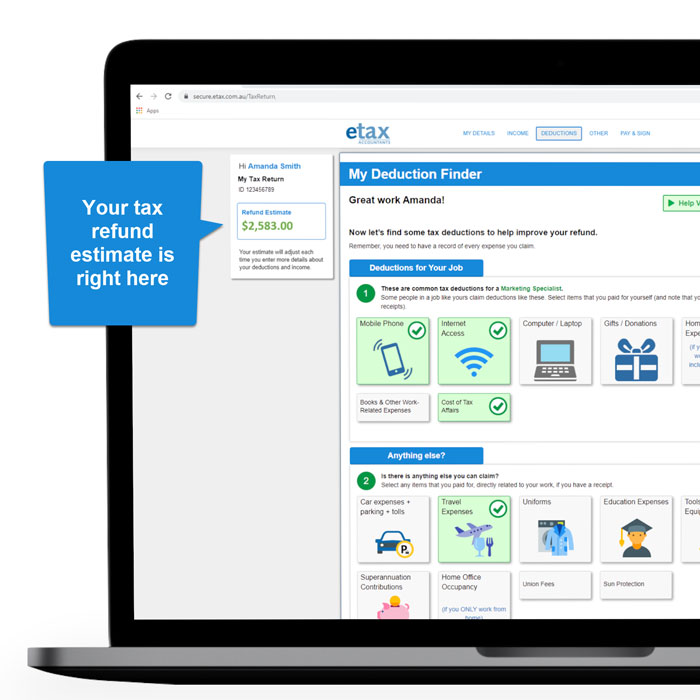

Most reputable tax preparation software (like TurboTax, H&R Block, TaxAct, etc.) offers free online estimators. These tools allow you to input your income, withholdings, deductions, and credits in a simplified manner, providing an instant estimate of your potential refund or amount owed. As you near tax season, these same platforms guide you through the full filing process, continuously updating your refund estimate as you enter more detailed information. This is often the most accessible and accurate method for most taxpayers.

Consulting a Tax Professional

For those with complex tax situations (e.g., self-employment income, investments, rental properties, multiple states, significant itemized deductions, or major life changes), a qualified tax professional (CPA, Enrolled Agent, or tax attorney) can provide a more precise estimate. They can review your financial documents, offer personalized advice, and help identify deductions and credits you might otherwise miss. While there’s a cost involved, the value of expert guidance can often outweigh the expense, especially if it leads to a larger legitimate refund or avoids costly errors.

Manual Calculation: A Step-by-Step Approach

While more labor-intensive, understanding the manual calculation process provides deep insight into your tax situation:

- Gather All Income Documents: W-2s, 1099s, K-1s, etc.

- Calculate Total Gross Income.

- Calculate Adjustments to Income: Deduct items like IRA contributions, student loan interest, HSA contributions to arrive at your AGI.

- Determine Your Filing Status.

- Choose Between Standard Deduction or Itemized Deductions: Calculate both and select the higher amount.

- Subtract Deductions from AGI: This gives you your Taxable Income.

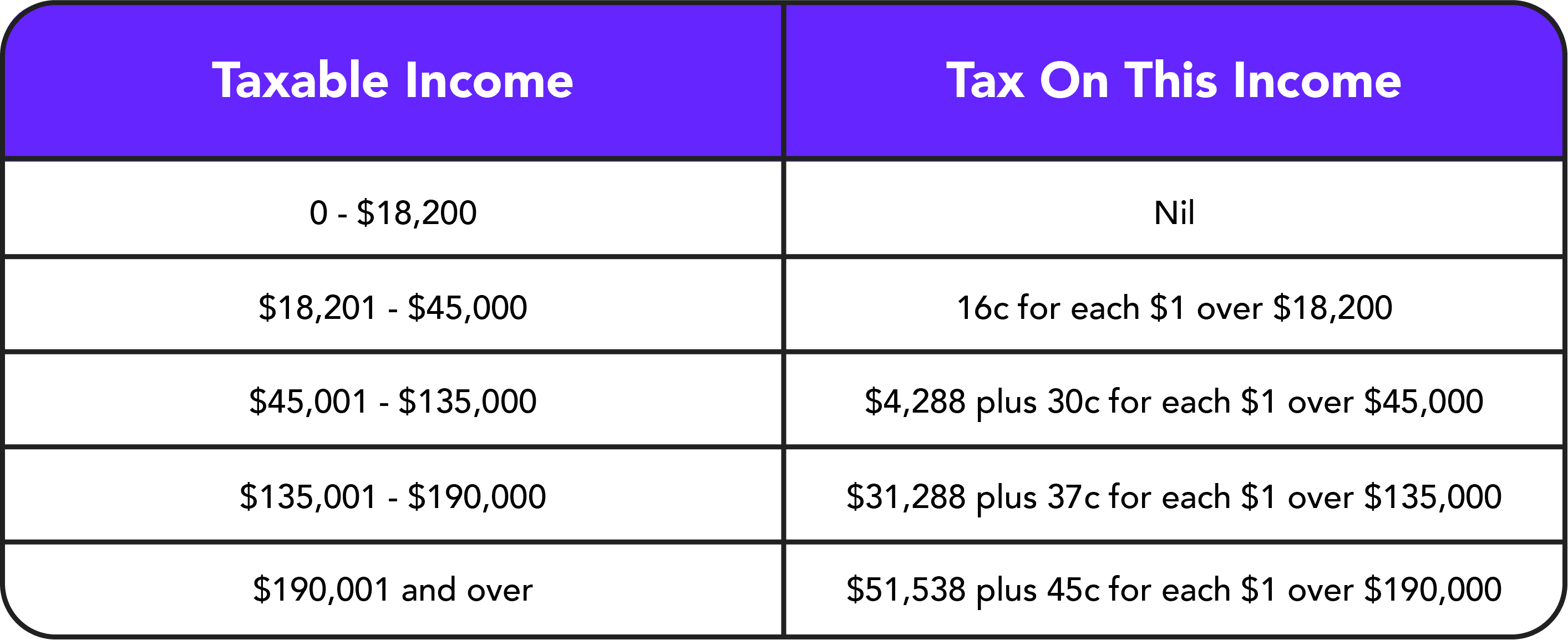

- Calculate Your Tax Liability: Apply the appropriate tax brackets to your taxable income based on your filing status.

- Identify and Apply Tax Credits: Subtract any eligible nonrefundable and then refundable credits from your tax liability.

- Compare Tax Liability to Total Payments: If your total withholdings and estimated payments exceed your final tax liability after credits, the difference is your refund.

The IRS Tax Withholding Estimator tool is also an excellent resource for a manual-assisted approach, particularly for adjusting W-4 information.

Common Pitfalls to Avoid in Estimation

- Ignoring Major Life Changes: Failing to account for a new job, marriage, birth of a child, or home purchase will lead to inaccurate estimates.

- Overlooking Deductions or Credits: Many taxpayers miss out on legitimate tax breaks. Keep thorough records of all potentially deductible expenses and research applicable credits.

- Assuming Prior Year’s Refund: Your financial situation rarely mirrors the previous year perfectly. Always re-evaluate from scratch.

- Estimating Without Documentation: Relying on memory or rough figures instead of actual W-2s, 1099s, and expense records will lead to errors.

- Not Factoring in State Taxes: Remember that state income taxes are separate and often have their own set of rules and withholding considerations.

Optimizing Your Tax Situation for Future Returns

Receiving a large refund can feel great, but it often signifies an opportunity to improve your year-round financial strategy. Proactive planning can help you keep more of your money throughout the year or strategically direct your refund.

Adjusting Your W-4 for Better Accuracy

The most direct way to influence your refund amount is by adjusting your Form W-4 with your employer. The goal is to have your withholdings as close as possible to your actual tax liability.

- If you consistently get large refunds: Consider increasing the amount of money you want withheld from each paycheck by adjusting your W-4, which means more take-home pay throughout the year. Use the IRS Tax Withholding Estimator to guide you.

- If you consistently owe tax: You might need to decrease your withholdings or have an additional amount withheld from each paycheck to avoid a tax bill or penalties at year-end.

Reviewing your W-4 annually, especially after major life events, is a best practice.

Maximizing Deductions and Credits Proactively

Don’t wait until tax season to think about deductions and credits. Adopt proactive strategies:

- Track Expenses Meticulously: Keep detailed records (receipts, mileage logs, medical bills) for all potential itemized deductions or business expenses. Use budgeting apps or spreadsheets.

- Contribute to Tax-Advantaged Accounts: Maximize contributions to 401(k)s, IRAs (Traditional IRA contributions can be deductible), and Health Savings Accounts (HSAs), which offer tax benefits.

- Research New Credits: Stay informed about new or expanded tax credits for which you might qualify (e.g., energy-efficient home improvement credits).

- Plan Charitable Giving: If you itemize, strategize your charitable contributions to maximize their tax benefit.

The Debate: Large Refund vs. More Take-Home Pay

This is a central philosophical question in personal finance.

- Large Refund Supporters: See it as a forced savings plan or a “bonus” that arrives once a year, providing a lump sum for large purchases or debt repayment.

- More Take-Home Pay Supporters: Argue that it’s financially savvier to have access to your money throughout the year. This allows you to earn interest on savings, pay down high-interest debt faster, or invest regularly, compounding your returns. Why give the government an interest-free loan?

There’s no single “right” answer; it depends on your financial discipline and goals. However, from a purely economic standpoint, having access to your money sooner is generally preferable, provided you can manage it responsibly.

Financial Planning Beyond the Refund Check

Your tax refund should be an integrated part of your broader financial plan. Don’t view it in isolation. Think about:

- Emergency Fund: Does your refund bolster your emergency savings?

- Debt Reduction: Can it significantly reduce high-interest debt?

- Investment Goals: Could it kickstart or accelerate your investment strategy?

- Budgeting: Does your year-round budget account for your actual take-home pay, rather than anticipating a large refund to cover gaps?

What to Do When Your Refund Arrives

Congratulations! Your refund has arrived. Now what? This “found money” presents an excellent opportunity to advance your financial goals.

Smart Spending: Prioritizing Debt or Savings

Before indulging, consider the most impactful use of your refund:

- High-Interest Debt: Prioritize paying down credit card balances, personal loans, or other high-interest debt. The interest savings can be substantial.

- Emergency Fund: If you don’t have 3-6 months of living expenses saved, this is a prime opportunity to build or top off your emergency fund.

- Savings Goals: Allocate funds towards specific savings goals like a down payment on a house, a new car, or a child’s education.

Investing Your Refund for Long-Term Growth

If your emergency fund is solid and high-interest debt is managed, consider investing your refund:

- Retirement Accounts: Contribute to a Roth IRA or Traditional IRA, taking advantage of tax benefits and long-term growth potential.

- Brokerage Account: Invest in a diversified portfolio of stocks, bonds, or exchange-traded funds (ETFs) for general wealth building.

- Educational Savings: Contribute to a 529 plan for future education expenses.

Even a modest refund, invested wisely, can grow significantly over time due to the power of compounding.

Treating Yourself (Responsibly)

While financial prudence is key, there’s nothing wrong with allocating a portion of your refund to something enjoyable. Whether it’s a small splurge, a vacation, or a much-desired purchase, doing so responsibly can boost morale and help maintain long-term financial discipline. The key is balance: perhaps an 80/20 split (80% towards financial goals, 20% for fun) or whatever ratio aligns with your personal circumstances.

Planning for the Next Tax Season

The arrival of one year’s refund is the perfect time to start thinking about the next tax season.

- Review Your W-4: Are your withholdings still appropriate?

- Set Financial Goals: What do you want your refund (or lack thereof) to look like next year? Do you want more take-home pay or a similar refund?

- Organize Records: Start a dedicated folder or digital system for tracking income, expenses, and other tax-relevant documents throughout the year.

- Stay Informed: Keep an eye on any new tax laws or changes that might affect your situation.

Your tax refund is more than just a check from the government; it’s a direct reflection of your year-round financial activities and decisions. By understanding how it’s calculated, actively managing your withholdings, and strategically planning for its arrival, you can transform this annual event into a powerful tool for achieving your personal finance goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.