The decision to claim Social Security benefits at age 62 is one of the most pivotal financial choices many Americans face as they approach retirement. While it offers the immediate gratification of income, it also comes with a permanent reduction in monthly benefits compared to waiting until your Full Retirement Age (FRA) or even later. Understanding the nuances of this decision – how much you’ll receive, the factors influencing that amount, and the long-term implications – is crucial for a financially secure retirement. This guide aims to demystify the complexities of claiming Social Security at the earliest possible age, providing insights to help you make an informed choice that aligns with your personal financial goals and life circumstances.

Understanding Social Security Retirement Benefits at 62

Claiming Social Security at age 62 means opting for what the Social Security Administration (SSA) refers to as “early retirement.” This is the earliest age at which an individual can begin receiving retirement benefits based on their work record. However, it’s vital to understand that this comes with a trade-off: a permanent reduction in your monthly benefit amount.

The Concept of Early Retirement Age (ERA)

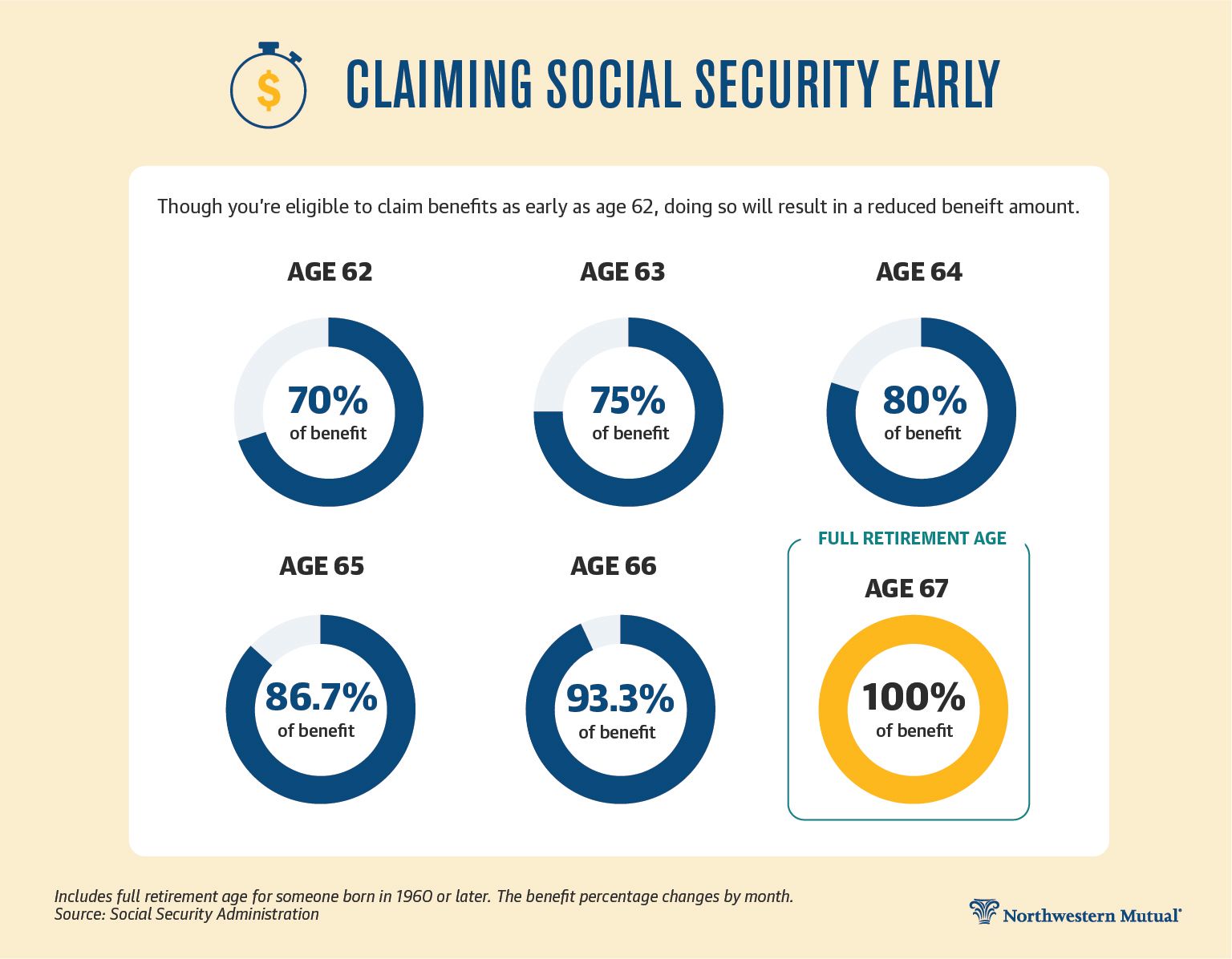

Age 62 is designated as the Early Retirement Age for Social Security. While it provides flexibility for those who wish or need to retire sooner, it’s important to distinguish it from your Full Retirement Age (FRA). Your FRA depends on your birth year:

- Born 1943-1954: FRA is 66

- Born 1955-1959: FRA gradually increases from 66 and 2 months to 66 and 10 months

- Born 1960 or later: FRA is 67

The benefit you receive at your FRA is considered your “primary insurance amount” (PIA). Claiming at 62 means your PIA will be permanently reduced.

How Your Benefits Are Calculated

To determine your Social Security benefits, the SSA first calculates your Average Indexed Monthly Earnings (AIME). This involves indexing your highest 35 years of earnings to account for wage growth over time, then averaging them. A specific formula, including “bend points” that are updated annually, is applied to your AIME to determine your Primary Insurance Amount (PIA) – the amount you would receive at your Full Retirement Age.

Once your PIA is established, the reduction for claiming at 62 is applied. The reduction is approximately 5/9 of one percent for each month before your FRA, up to 36 months, and 5/12 of one percent for each month beyond 36. For someone with an FRA of 67, claiming at 62 means a 60-month reduction, resulting in a benefit that is approximately 30% lower than their PIA. If your FRA is 66, claiming at 62 (48 months early) results in a reduction of about 25%.

The Impact of Claiming Social Security at 62

The decision to claim Social Security at the earliest possible age carries significant financial implications, primarily a permanent reduction in your monthly benefit check. Understanding this impact is crucial for long-term financial planning.

The Permanent Reduction Factor

As noted, claiming at 62 means your monthly benefit will be permanently reduced compared to what you would receive at your Full Retirement Age (FRA). For an individual whose FRA is 67, claiming at 62 results in a 30% reduction in their Primary Insurance Amount (PIA). This reduction is not temporary; it persists for the rest of your life. For example, if your PIA is $2,000, claiming at 62 would reduce your monthly benefit to approximately $1,400. This seemingly small difference can accumulate to hundreds of thousands of dollars over a typical retirement lifespan.

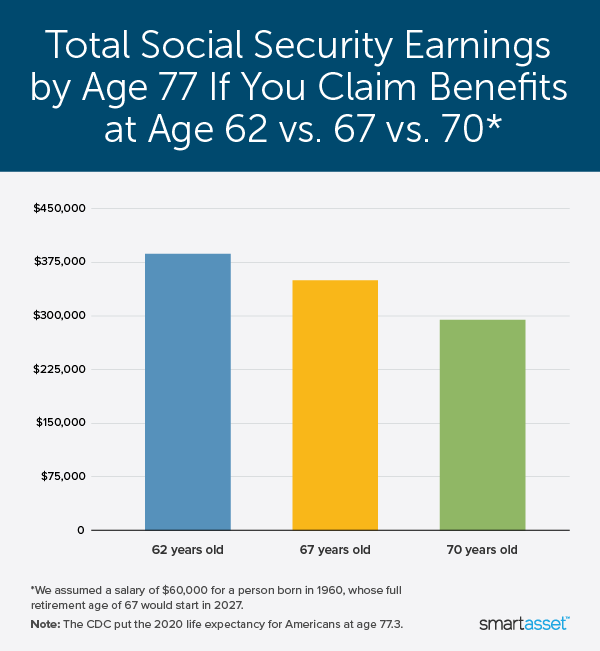

Break-Even Analysis: Is It Worth It?

A common analytical tool used by financial planners is a “break-even analysis.” This helps determine at what age the cumulative benefits received from delaying outweigh the cumulative benefits received from claiming early. While claiming early means receiving more checks initially, each check is smaller. Delaying means fewer checks initially, but each check is larger. For many, the break-even point often falls somewhere in their late 70s or early 80s. If you live beyond this point, delaying benefits typically results in a higher total lifetime payout. This analysis is highly individualized and depends on your specific PIA, FRA, and personal life expectancy projections.

Spousal and Survivor Benefits Considerations

The decision to claim early also affects potential spousal and survivor benefits. If you claim early, your spouse’s spousal benefit (which can be up to 50% of your PIA) will also be permanently reduced if they claim based on your record before their own FRA. If you pass away, your surviving spouse or children may be eligible for survivor benefits. These benefits are also impacted by your claiming decision; if you claimed early, the survivor benefit amount will be based on your reduced benefit, not your full PIA. Delaying your benefits can provide a larger survivor benefit for your loved ones.

Factors to Consider Before Claiming Early

Deciding when to claim Social Security is a complex personal finance decision, influenced by a multitude of individual circumstances. Before opting for age 62, it’s essential to carefully evaluate several key factors.

Your Health and Life Expectancy

Perhaps the most personal factor is your health and projected life expectancy. If you come from a family with a history of longevity and you are in good health, delaying benefits could result in a significantly higher total lifetime payout. Conversely, if you have chronic health issues or a family history of shorter lifespans, claiming earlier might be a prudent strategy to ensure you receive benefits for as long as possible. This is a highly personal assessment and should consider quality of life in later years.

Other Income Sources and Retirement Savings

Your current financial situation and the robustness of your other retirement income streams play a critical role. Do you have sufficient savings (401(k)s, IRAs, pensions, taxable investments) to comfortably cover your expenses until your Full Retirement Age, or even later, if you choose to delay Social Security? If your personal savings are substantial, you might be able to afford to wait for a larger Social Security check. If your savings are modest, claiming at 62 might be a necessity to cover living expenses, despite the reduction.

Employment Status and the Earnings Limit

If you plan to continue working after claiming Social Security at 62, you must be aware of the Social Security earnings limit. If you earn above a certain threshold (which changes annually), the SSA will temporarily withhold a portion of your benefits. For example, in the year you turn 62 and prior to your FRA, the SSA will deduct $1 from your benefits for every $2 you earn above the annual limit (e.g., $22,320 in 2024). Once you reach your Full Retirement Age, the earnings limit no longer applies, and you can earn any amount without your Social Security benefits being reduced. If you anticipate working full-time or earning significantly above the limit, claiming early might mean many of your benefits are withheld anyway, potentially negating the advantage of early claiming.

Future Financial Needs and Goals

Consider your long-term financial picture. Do you have significant upcoming expenses, such as home repairs, medical costs not covered by insurance, or desire to travel extensively in early retirement? How will your Social Security benefits integrate with these plans? A smaller, guaranteed income stream starting at 62 might provide crucial stability for immediate needs, but it could also limit your ability to handle unexpected future expenses without dipping heavily into other savings.

Strategies for Maximizing Your Social Security Benefits

Even with the option to claim at 62, there are various strategies and considerations that can help you maximize your lifetime Social Security income, or at least optimize it given your personal circumstances.

Understanding Your Full Retirement Age (FRA)

The bedrock of any Social Security claiming strategy is a clear understanding of your Full Retirement Age (FRA). This is the age at which you are entitled to 100% of your Primary Insurance Amount (PIA). As established, your FRA is determined by your birth year and typically ranges from 66 to 67. Knowing your FRA allows you to precisely calculate the reduction you’ll face by claiming early or the delayed retirement credits you’ll earn by waiting. Use the SSA’s online tools or your annual Social Security statement to confirm your specific FRA and PIA.

Delaying Benefits Beyond FRA

While the focus here is on age 62, it’s crucial to acknowledge the advantage of delaying benefits beyond your FRA. For each year you delay claiming past your FRA, up to age 70, you earn “delayed retirement credits.” These credits increase your annual benefit by 8% per year. For someone with an FRA of 67, delaying until age 70 would result in a 24% increase in their monthly benefit compared to their PIA. This can be a powerful strategy for those who are healthy, have sufficient other income or savings, and want to ensure the highest possible guaranteed income stream for the longest possible duration.

Coordinating with a Spouse

For married couples, Social Security becomes a joint financial planning exercise. Strategic coordination can significantly enhance total household lifetime benefits. Often, the higher-earning spouse might benefit from delaying their claim as long as possible (up to age 70) to maximize their own benefit, which will also become the basis for a higher survivor benefit for the lower-earning spouse. The lower-earning spouse might consider claiming their own benefits as early as 62, providing some income while the higher earner’s benefits grow.

Navigating the Application Process and Beyond

Once you’ve carefully considered all the factors and decided that claiming Social Security at 62 is the right path for you, the next step is to navigate the application process.

Required Documentation

To apply for Social Security retirement benefits, you’ll generally need: your Social Security card, birth certificate, proof of U.S. citizenship (if applicable), W-2 forms or self-employment tax returns for the previous year, U.S. military service papers (if applicable), your bank account number and routing number for direct deposit, and marriage information. Always check the SSA website (ssa.gov) for the most current and complete list of required documents.

Applying Online, By Phone, or In-Person

The Social Security Administration offers several convenient ways to apply:

- Online (Recommended): The fastest and easiest way for most people to apply for retirement benefits is online at ssa.gov.

- By Phone: You can call the SSA’s toll-free number at 1-800-772-1213.

- In-Person: You can visit your local Social Security office; calling ahead for an appointment is advisable.

It’s recommended to apply three months before you want your benefits to start to ensure a smooth transition.

What Happens After You Start Receiving Benefits

Once your application is approved, your benefits will typically be deposited directly into your bank account on a specific date each month. Your benefit amount will likely increase over time due to annual Cost-of-Living Adjustments (COLAs). A portion of your Social Security benefits may be subject to federal income tax if your combined income exceeds certain thresholds. While the decision to claim at 62 is generally permanent, there is a one-time opportunity within the first 12 months to withdraw your application, repay all benefits received, and then reapply later for a higher benefit. This is a complex maneuver and should only be considered after thorough consultation with the SSA or a financial advisor.

Conclusion

The question of “how much Social Security at 62” is more than just a number; it’s a doorway to a complex financial decision that impacts the rest of your retirement journey. While claiming at the earliest possible age offers immediate income, it comes at the cost of a permanently reduced monthly benefit. A thoughtful approach involves a deep dive into your personal health and life expectancy, the adequacy of your other retirement savings, your intentions to continue working, and your overall financial goals. By weighing these factors carefully and understanding the various strategies available, you can make an informed choice that sets the stage for a financially secure and fulfilling retirement. Consulting with the Social Security Administration directly or a qualified financial advisor can provide personalized guidance tailored to your unique circumstances.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.