Car insurance stands as a pivotal financial commitment for vehicle owners, yet its monthly cost is far from a fixed figure. Unlike a standard utility bill, the premium for car insurance is a highly individualized calculation, subject to a complex interplay of numerous variables. Understanding these factors is crucial for any driver aiming to budget effectively and secure optimal coverage without overspending. This article delves into the intricate financial landscape of car insurance, dissecting the elements that determine your monthly outlay and providing actionable strategies for smart money management in this essential expenditure.

Understanding the Variables That Drive Premiums

The seemingly simple question of “how much per month” quickly unravels into a detailed financial analysis, with insurers assessing a multitude of risk factors to determine your premium. These factors fall broadly into categories related to the driver, the vehicle, the location, and the specifics of the policy chosen.

Driver Demographics and History

Your personal profile is a significant determinant. Age, for instance, plays a substantial role, with younger, less experienced drivers typically facing higher premiums due to a statistically greater likelihood of accidents. Rates tend to decrease as drivers mature and gain more experience, often leveling off in middle age, before potentially rising again for very senior drivers. Gender can also be a minor factor in some regions, though its influence is diminishing. More critically, your driving record – including accidents, traffic violations, and claims history – directly impacts your premium. A clean record signifies lower risk and can lead to substantial savings, while infractions will invariably elevate costs. Furthermore, many insurers utilize a credit-based insurance score, where a strong credit history can signal greater financial responsibility and, consequently, a lower risk profile, leading to more favorable rates.

Vehicle Characteristics

The car you drive is another primary factor in the cost equation. The make, model, year, and even the body style contribute to the risk assessment. High-performance or luxury vehicles, which are more expensive to repair or replace, naturally command higher premiums for collision and comprehensive coverage. Similarly, vehicles with higher theft rates or those lacking advanced safety features may also incur increased costs. Conversely, cars with excellent safety ratings, anti-theft devices, and lower repair costs can often lead to discounts and lower overall premiums. The cost of parts and labor for your specific vehicle also plays a role in the insurer’s calculation of potential payouts.

Geographical Location

Where you live and park your car profoundly impacts your insurance rates. Urban areas, with higher traffic density, greater incidences of accidents, and increased risks of theft and vandalism, typically face higher premiums than rural locales. Even within the same city, specific zip codes can have vastly different rates based on local crime statistics, accident rates, and population density. State-specific regulations, mandatory minimum coverage limits, and local market competition among insurers also contribute to regional variations in pricing.

Coverage Types and Limits

Perhaps the most direct financial lever you can pull is your choice of coverage. Every policy is a mosaic of different types of protection, each with its own cost. State-mandated liability coverage is the baseline, but adding collision, comprehensive, uninsured/underinsured motorist, personal injury protection (PIP), or medical payments (MedPay) will increase your premium. The limits you choose for each coverage (e.g., $100,000 vs. $250,000 for bodily injury liability) and your deductible amounts (the portion you pay out-of-pocket before insurance kicks in for collision and comprehensive claims) directly correlate with your monthly payment. Higher limits offer greater financial protection but come at a higher cost, while increasing your deductible typically lowers your monthly premium, albeit at the expense of a larger out-of-pocket expense in the event of a claim.

Deconstructing Average Monthly Costs

While no universal answer exists for the exact monthly cost of car insurance, examining averages can provide a useful benchmark for financial planning. It’s crucial, however, to view these averages with the understanding that personal circumstances will dictate individual premiums.

National Averages vs. Personal Reality

Nationally, the average full coverage car insurance premium in the United States often hovers around $150-$200 per month, or roughly $1,800-$2,400 per year. For minimum liability coverage, these averages can drop significantly, often in the range of $50-$100 per month. However, these figures are broad strokes. Your actual quote will be meticulously tailored to your unique risk profile. Factors like your age, driving record, vehicle, and chosen coverage can easily push your premium significantly above or below these averages. For example, a young, inexperienced driver with a brand-new sports car in an urban area could pay $300-$500 per month or more, whereas a mature driver with a clean record and an older sedan in a rural setting might pay less than $100.

State-by-State Variations

The cost of car insurance varies dramatically by state due to differing legal requirements, accident rates, weather patterns, population densities, and competition among insurers. States with high population densities and mandatory no-fault insurance laws, such as Michigan or New York, often see some of the highest average premiums. Conversely, less densely populated states with lower minimum requirements might have some of the lowest average costs. It’s not uncommon for average premiums to differ by hundreds of dollars per month between the most and least expensive states, making geographical location a primary financial influencer.

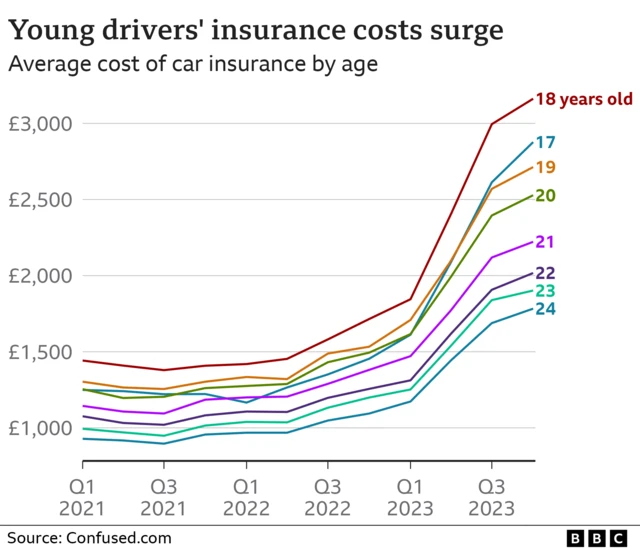

Impact of Age and Driving Experience

Age is a powerful statistical indicator for insurers. Teen drivers, particularly males, face the highest insurance rates due to their lack of experience and higher accident rates. A 16-year-old driver might pay upwards of $400-$600 per month, an astronomical sum for many budgets. Rates generally begin to decrease in the early 20s, stabilize through the 30s, 40s, and 50s, and may see a slight increase again after age 65 or 70. The drop from teen rates to those of a 25-year-old can be substantial, often representing a 50% reduction or more, underscoring the financial benefit of years of safe driving experience.

Essential Coverage Types and Their Financial Implications

Understanding the various types of coverage is not just about knowing what they protect; it’s also about recognizing their contribution to your overall monthly premium and making financially informed decisions.

Liability Coverage: The Non-Negotiable Minimum

Liability insurance is the foundation of every car insurance policy and is legally mandated in almost every state. It covers damages you cause to other people or their property in an at-fault accident. It’s typically split into bodily injury liability (covering medical expenses, lost wages, and pain and suffering for others) and property damage liability (covering repairs or replacement of another person’s vehicle or property). While it’s tempting to opt for state minimum limits to keep monthly costs low, this can be a significant financial risk. If an accident’s damages exceed your liability limits, you are personally responsible for the remaining balance, potentially leading to devastating financial consequences. Savvy financial planning often dictates choosing higher liability limits to safeguard your assets.

Protecting Your Investment: Collision and Comprehensive

Collision coverage pays for damages to your own vehicle resulting from a collision with another car or object, regardless of fault. Comprehensive coverage protects your vehicle from non-collision incidents, such as theft, vandalism, fire, natural disasters, or impacts with animals. These two coverages are often required if you have a car loan or lease and significantly increase your monthly premium, particularly if you have a newer or more expensive vehicle. However, for a vehicle of considerable value, the financial protection they offer can be invaluable, preventing massive out-of-pocket repair or replacement costs. As a vehicle ages and depreciates, the financial wisdom of retaining these coverages needs to be re-evaluated against their monthly cost.

Beyond the Basics: PIP, MedPay, and UM/UIM

Personal Injury Protection (PIP) and Medical Payments (MedPay) coverage pay for medical expenses for you and your passengers, regardless of fault. PIP, mandatory in “no-fault” states, can also cover lost wages and other non-medical expenses. Uninsured/Underinsured Motorist (UM/UIM) coverage protects you if you’re involved in an accident with a driver who has no insurance or insufficient insurance to cover your damages. These coverages add to your monthly bill but offer crucial financial safety nets, especially given the rising costs of healthcare and the prevalence of uninsured drivers. Deciding on these additions requires weighing your personal financial risk tolerance and health insurance coverage against the added premium.

Proven Strategies to Reduce Your Monthly Premiums

While many factors are fixed, drivers have significant control over several elements that can directly reduce their monthly car insurance costs. Implementing these strategies requires a proactive approach to financial management.

The Power of Comparison Shopping

One of the most effective ways to lower your monthly premium is to regularly compare quotes from multiple insurance providers. The same coverage from different companies can vary by hundreds of dollars per year, or tens of dollars per month, because each insurer has its own proprietary risk assessment models and target markets. Using online comparison tools or working with an independent insurance agent can streamline this process, ensuring you find the most competitive rates for your specific needs. This isn’t a one-time exercise; reviewing your options annually or whenever your personal circumstances change can yield continuous savings.

Leveraging Discounts

Insurers offer a wide array of discounts that can significantly chip away at your monthly payment. Common discounts include:

- Multi-policy/Bundling: Combining car insurance with home, renters, or life insurance from the same provider.

- Multi-car: Insuring more than one vehicle on the same policy.

- Good Driver/Safe Driver: For maintaining a clean driving record over several years.

- Good Student: For young drivers who maintain a high GPA.

- Defensive Driving Course: Completing an approved defensive driving program.

- Vehicle Safety Features: For cars equipped with anti-lock brakes, airbags, anti-theft systems, etc.

- Low Mileage: For drivers who don’t drive frequently.

- Telematics/Usage-Based Insurance: Programs that monitor your driving habits (speed, braking, mileage) via a device or app, offering discounts for safe driving.

Actively inquiring about and qualifying for all applicable discounts is a smart financial move.

Optimizing Your Deductibles and Coverage Levels

Adjusting your deductibles for collision and comprehensive coverage is a direct way to influence your monthly premium. Opting for a higher deductible (e.g., $1,000 instead of $500) will lower your monthly payment, as you’re agreeing to bear more of the initial financial burden in case of a claim. However, it’s crucial to ensure you have sufficient emergency savings to cover that higher deductible if an incident occurs. Additionally, as your car ages and depreciates, you might consider dropping collision and comprehensive coverage entirely if the vehicle’s cash value is less than the annual premium plus your deductible. This requires a careful cost-benefit analysis based on your car’s value and your financial risk tolerance.

Maintaining a Strong Financial Profile

Your credit score often plays a role in insurance pricing in many states. Insurers use credit-based insurance scores as a predictor of future claims. A higher credit score can lead to lower premiums, reflecting responsible financial behavior. Therefore, proactively managing your credit by paying bills on time, keeping credit utilization low, and regularly checking your credit report can indirectly lead to car insurance savings. Furthermore, avoiding traffic violations and accidents helps maintain a clean driving record, which is arguably the most impactful factor in long-term premium reduction.

The Long-Term Financial Planning Perspective

Car insurance is not just a monthly bill; it’s an ongoing financial commitment that requires strategic planning. Integrating insurance costs into your broader financial picture ensures you’re adequately protected without draining your resources.

Annual Policy Reviews and Adjustments

Life circumstances change, and so should your insurance policy. Getting married, moving, buying a new car, or adding a teen driver all impact your risk profile and potential discounts. Make it a point to review your policy at least once a year, or whenever a major life event occurs. This allows you to adjust coverage, apply for new discounts, and re-evaluate your deductibles. Such vigilance ensures your coverage remains appropriate for your current needs and that you are not paying for unnecessary protection or, conversely, are underinsured.

The Balance Between Cost and Protection

Ultimately, the question of “how much per month is car insurance” boils down to finding the optimal balance between affordability and adequate protection. While reducing costs is a valid financial goal, it should never come at the expense of leaving yourself vulnerable to catastrophic financial loss in the event of a serious accident. A robust policy provides peace of mind and safeguards your assets, making the monthly investment a wise expenditure. Financial prudence dictates understanding your risks, comparing options diligently, and selecting a policy that aligns with both your budget and your comprehensive financial security strategy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.