The question of how much of one’s paycheck to save is a cornerstone of personal finance, a dilemma faced by individuals across all income levels and life stages. It’s a question that doesn’t have a single, universal answer, but rather a spectrum of optimal strategies tailored to individual circumstances, goals, and financial health. In an increasingly complex economic landscape, mastering the art of consistent saving is not just about accumulating wealth; it’s about building resilience, securing future aspirations, and achieving genuine financial peace of mind.

This article delves into the principles, strategies, and practical steps you can take to determine your ideal savings rate, transforming vague intentions into actionable financial habits. From understanding your current financial reality to leveraging time-tested benchmarks and adapting to life’s evolving demands, we’ll explore how to craft a savings plan that truly works for you.

Understanding Your Financial Landscape

Before you can determine an appropriate savings rate, you must first gain a clear, honest understanding of your current financial situation. This foundational step is crucial for setting realistic goals and identifying areas for improvement.

Assessing Your Current Income and Expenses

The first order of business is to map out your cash flow. This involves accurately tracking all sources of income and diligently categorizing every expense.

- Income: This includes your net take-home pay from your primary job, as well as any income from side hustles, investments, or other sources. Ensure you’re working with the after-tax amount, as this is what you actually have available to save and spend.

- Expenses: Go through bank statements, credit card bills, and cash transactions for at least one to three months. Categorize expenses into fixed (rent/mortgage, loan payments, insurance premiums) and variable (groceries, entertainment, utilities, transport). Many people are surprised to discover where their money truly goes once they see it laid out in black and white. This exercise often reveals “money leaks”—small, regular expenditures that add up significantly over time.

Differentiating Between Needs, Wants, and Savings Goals

With your income and expenses clearly defined, the next step is to distinguish between what you absolutely need to spend money on, what you want to spend money on, and what you should be allocating towards your future.

- Needs: These are essential living expenses that keep a roof over your head, food on your table, and ensure your basic well-being. Examples include housing, utilities, groceries, transportation to work, basic healthcare, and minimum debt payments.

- Wants: These are discretionary expenses that improve your quality of life but are not strictly necessary for survival. Examples include dining out, entertainment, subscriptions, vacations, designer clothes, and non-essential gadgets. While wants contribute to happiness, they are often the first place to cut back when aiming to increase savings.

- Savings Goals: These are specific financial objectives that you are actively working towards. They could be short-term (emergency fund, down payment for a car), medium-term (house down payment, child’s education), or long-term (retirement, financial independence). Each goal should ideally have a target amount and a timeline.

The Importance of a Realistic Budget

Once you’ve assessed your income and categorized your spending, you can construct a realistic budget. A budget isn’t a restrictive cage; it’s a financial roadmap that empowers you to make informed decisions about your money. It formalizes your understanding of your cash flow and allows you to proactively allocate funds towards your needs, wants, and, crucially, your savings goals. Without a budget, saving becomes a sporadic, often frustrating, endeavor. A well-constructed budget makes saving an intentional and achievable part of your financial routine.

The Golden Rules of Saving: Common Benchmarks and Strategies

While your personal situation dictates the exact percentage, several well-established guidelines offer excellent starting points for determining how much of your paycheck you should be saving.

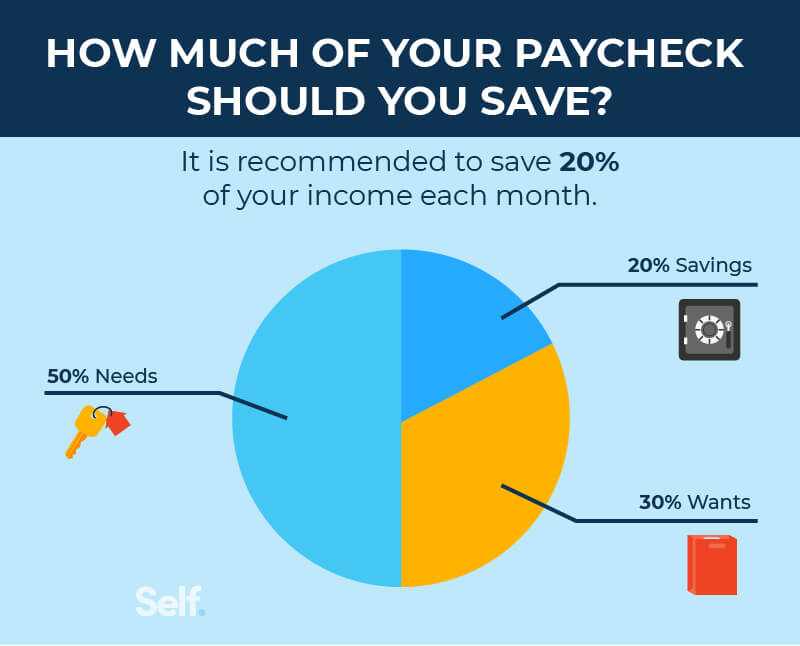

The 50/30/20 Rule: A Popular Guideline

One of the most widely cited and accessible budgeting frameworks is the 50/30/20 rule, popularized by Senator Elizabeth Warren. It suggests allocating your after-tax income as follows:

- 50% to Needs: This portion covers your essential living expenses, such as housing, utilities, groceries, transportation, and minimum loan payments. If your needs are consuming more than 50% of your income, it signals an area where you might need to make adjustments, such as finding more affordable housing or reducing other fixed costs.

- 30% to Wants: This discretionary portion allows for lifestyle choices and personal enjoyment, like dining out, entertainment, hobbies, and vacations. It’s important to be honest about what truly falls into this category.

- 20% to Savings & Debt Repayment: This crucial segment is dedicated to building your financial future. It includes contributions to an emergency fund, retirement accounts (401k, IRA), investment accounts, and any extra payments towards high-interest debt (like credit cards). For many, this 20% is the minimum target to aim for to build substantial wealth over time.

Automating Your Savings: The Path of Least Resistance

One of the most powerful strategies for consistent saving is automation. By setting up automatic transfers from your checking account to your savings or investment accounts, you remove the need for willpower and decision-making each payday.

- Set it and Forget It: Arrange for a fixed amount or percentage of your paycheck to be transferred directly to your savings accounts immediately after you get paid. Many employers offer direct deposit options that allow you to split your paycheck across multiple accounts.

- Treat Savings as a Bill: Just as you wouldn’t forget to pay your rent or utility bill, treat your savings contribution as a non-negotiable expense. By prioritizing it at the beginning of your pay cycle, you ensure that you “pay yourself first.” This psychological shift is incredibly effective in building a robust savings habit.

Setting SMART Savings Goals

Vague goals yield vague results. To make your savings efforts effective and motivating, define your goals using the SMART criteria:

- Specific: What exactly are you saving for? (e.g., “$10,000 for an emergency fund,” “down payment for a house in three years”)

- Measurable: How much do you need, and how will you track progress? (e.g., “$500 per month,” “increase balance by X% annually”)

- Achievable: Is the goal realistic given your income and expenses?

- Relevant: Does this goal align with your broader financial aspirations and values?

- Time-bound: When do you want to achieve this goal? (e.g., “within 18 months,” “by age 65”)

Having clear, SMART goals provides direction and motivation, making it easier to stick to your savings plan and adjust as needed.

Tailoring Your Savings Plan to Life Stages and Goals

The ideal savings rate isn’t static; it evolves significantly based on your age, income, family situation, and major life milestones. What’s appropriate for someone in their early twenties just starting out will differ from someone nearing retirement.

Early Career: Building an Emergency Fund and Debt Repayment

In the early stages of your career, priorities often revolve around establishing a stable financial foundation.

- Emergency Fund: Your absolute first savings goal should be an emergency fund, ideally covering 3-6 months of essential living expenses. This fund acts as a critical buffer against job loss, medical emergencies, or unexpected car repairs, preventing you from going into debt when unforeseen events occur. Aim to save at least 10-15% of your paycheck until this is fully funded.

- High-Interest Debt Repayment: Once a small starter emergency fund (e.g., $1,000) is in place, aggressively tackle high-interest debts like credit card balances or personal loans. The interest rates on these debts can quickly erode any savings gains. Prioritizing their elimination frees up significant cash flow for future savings.

- Initial Retirement Contributions: Even if it’s just a small percentage, start contributing to a retirement account, especially if your employer offers a matching program. This “free money” is invaluable for long-term growth due to the power of compounding.

Mid-Career: Retirement Planning and Major Milestones (Home, Education)

As you advance in your career and potentially gain higher earning potential, your savings capacity and goals typically expand.

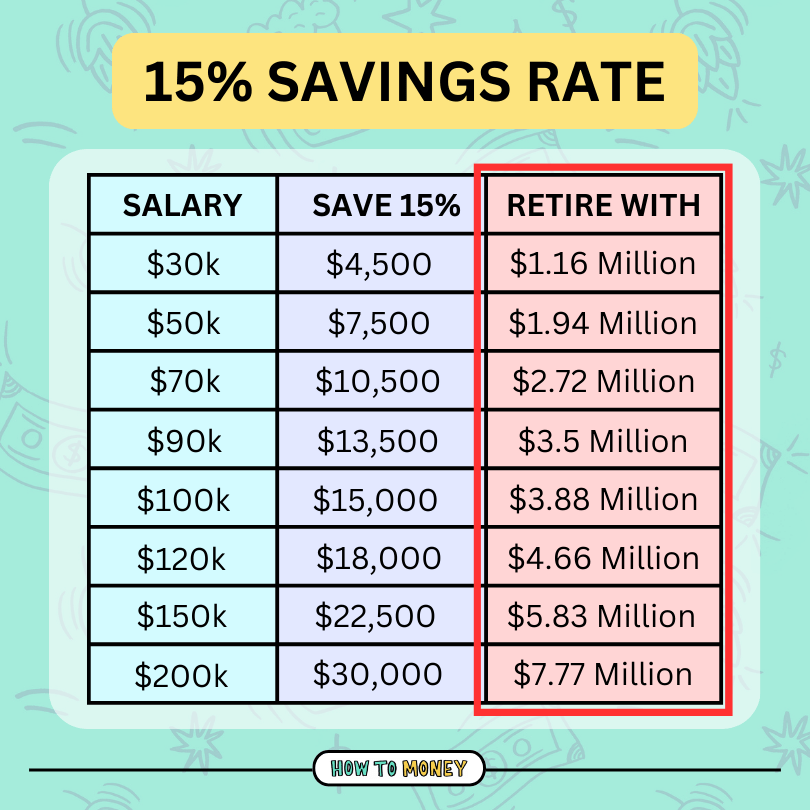

- Increased Retirement Contributions: Aim to increase your retirement savings to 15% or even 20% of your income. Maximize contributions to tax-advantaged accounts like 401(k)s, 403(b)s, and IRAs.

- Major Down Payments: Saving for a house down payment, a significant car purchase, or other large assets often becomes a priority. This may require temporarily increasing your savings rate even further, perhaps by reducing discretionary spending.

- Child’s Education: If you have children, planning for their future education costs through 529 plans or other investment vehicles becomes a new savings goal.

- Diversified Investments: Beyond retirement accounts, consider opening a taxable brokerage account for broader investment opportunities and financial growth.

Approaching Retirement: Maximizing Contributions and Drawdown Strategies

In the decade or two leading up to retirement, the focus shifts to maximizing contributions and ensuring your nest egg is robust enough for your desired lifestyle.

- Catch-Up Contributions: If you’re over 50, take advantage of “catch-up” contributions allowed by the IRS for 401(k)s and IRAs, which enable you to save extra amounts beyond the standard limits.

- Refining Investment Strategy: As retirement nears, you might shift your investment strategy from aggressive growth to more conservative, income-generating assets to protect your accumulated capital.

- Healthcare Costs: Begin to factor in potential healthcare costs in retirement, which can be significant. Consider contributions to a Health Savings Account (HSA) if eligible, as it offers a triple tax advantage.

- Withdrawal Strategy: Start planning your income sources and withdrawal strategy for retirement, including Social Security, pensions, and personal savings, to ensure a sustainable income stream.

Maximizing Your Savings Potential and Overcoming Challenges

Even with a solid plan, staying on track can be challenging. Proactive management and adaptability are key to maximizing your savings and navigating financial hurdles.

Reviewing and Adjusting Your Budget Regularly

Life is dynamic, and so should be your budget. Review your income, expenses, and savings goals at least quarterly, or whenever there’s a significant life change (e.g., a new job, marriage, birth of a child, major expense).

- Identify Opportunities: Regular reviews help identify areas where you can save more, perhaps by cutting unnecessary subscriptions, negotiating better rates for services, or optimizing your grocery spending.

- Stay Realistic: If your initial savings goal proves too ambitious, it’s better to adjust it to an achievable level than to become discouraged and abandon saving altogether. Small, consistent savings are more effective than sporadic, large contributions.

Boosting Income Through Side Hustles and Skill Development

Sometimes, cutting expenses isn’t enough, or there’s simply no more fat to trim. In such cases, increasing your income can significantly accelerate your savings goals.

- Side Gigs: Explore opportunities for side hustles that leverage your skills or interests, such as freelancing, consulting, delivery services, or online tutoring. The extra income can be directed entirely towards savings or debt repayment.

- Skill Enhancement: Invest in yourself through further education, certifications, or professional development to increase your earning potential in your primary career. A raise or promotion can dramatically boost your capacity to save.

Handling Unexpected Expenses Without Derailing Your Plan

Life inevitably throws curveballs. Having a well-funded emergency fund is your primary defense. However, if an expense exceeds your emergency fund or occurs before it’s fully funded, avoid derailing your entire savings plan.

- Prioritize and Reallocate: Address the immediate expense, then adjust your budget temporarily to replenish your emergency fund or get back on track with other savings goals. It might mean a temporary pause on non-essential wants, but it prevents long-term damage.

- Avoid High-Interest Debt: Whenever possible, avoid using high-interest credit cards for unexpected expenses. If you must, have a clear plan to pay it off as quickly as possible.

Leveraging Financial Tools and Apps

Modern technology offers a plethora of tools to simplify budgeting and saving.

- Budgeting Apps: Apps like Mint, YNAB (You Need A Budget), or Personal Capital can automate expense tracking, categorize spending, and provide real-time insights into your financial health.

- Investment Platforms: Robo-advisors (e.g., Betterment, Wealthfront) or traditional brokerage platforms (e.g., Fidelity, Vanguard) make it easy to set up automated investments into diversified portfolios aligned with your risk tolerance and goals.

- High-Yield Savings Accounts: Ensure your emergency fund and short-term savings are in a high-yield savings account to earn more interest than traditional banks offer.

The Long-Term Impact: Why Consistent Saving Matters

The seemingly small decisions you make about your paycheck today have a profound, compounding impact on your financial future. Consistent saving is not merely an act of discipline; it’s an investment in your freedom, security, and aspirations.

The Power of Compounding

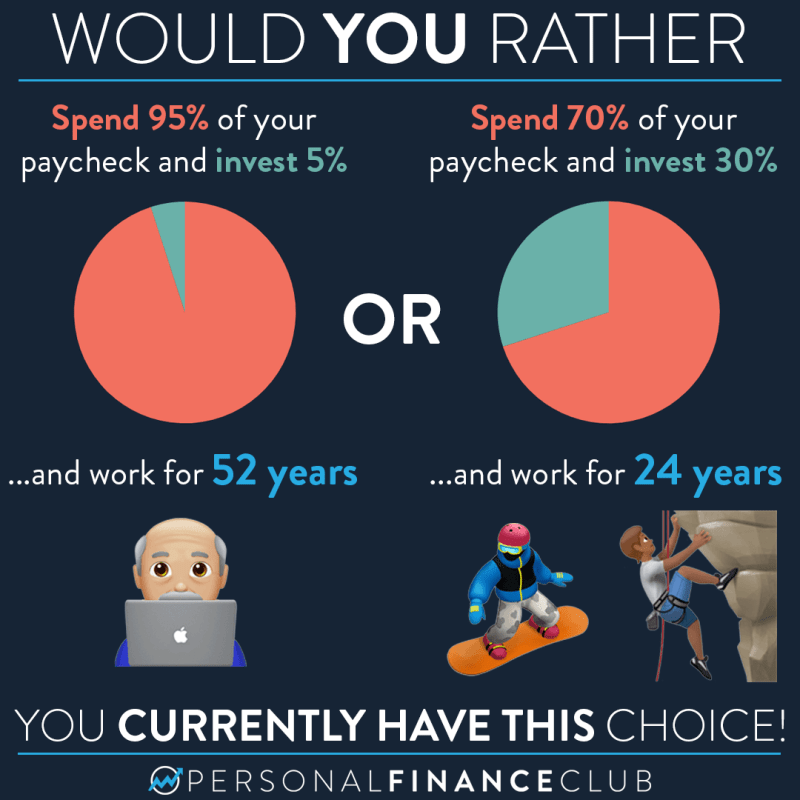

Albert Einstein reportedly called compound interest the “eighth wonder of the world.” When your savings earn returns, and those returns, in turn, earn their own returns, your money grows exponentially over time. The earlier you start saving, even small amounts, the more dramatically this effect benefits you. A modest monthly contribution sustained over decades can grow into a substantial nest egg, often far exceeding the total amount you personally contributed.

Financial Security and Peace of Mind

Having a robust savings buffer provides an unparalleled sense of security. Knowing you have funds set aside for emergencies, future goals, or even unexpected opportunities reduces stress and provides a safety net against life’s uncertainties. This peace of mind allows you to make decisions based on what’s best for your long-term well-being, rather than being driven by immediate financial pressures.

Achieving Financial Freedom

Ultimately, consistent saving is the pathway to financial freedom—the ability to make life choices without being constrained by money. Whether that means retiring early, pursuing a passion project, starting a business, or simply enjoying a comfortable and stress-free lifestyle, robust savings provide the options and flexibility to live life on your own terms. It’s about empowering yourself to design the future you truly desire, one saved paycheck at a time.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.