Securing a business loan is a pivotal step for growth, expansion, or simply managing working capital. However, one of the most common questions entrepreneurs face is not just “how do I get a loan?” but rather, “how much can my business actually qualify for?” The amount of financing available to your business is not a arbitrary figure; it’s the product of a complex evaluation by lenders, rooted deeply in your business’s financial health, industry standing, and the type of financing sought. Understanding these underlying factors is crucial for setting realistic expectations and effectively preparing your loan application.

Understanding the Factors Influencing Loan Amounts

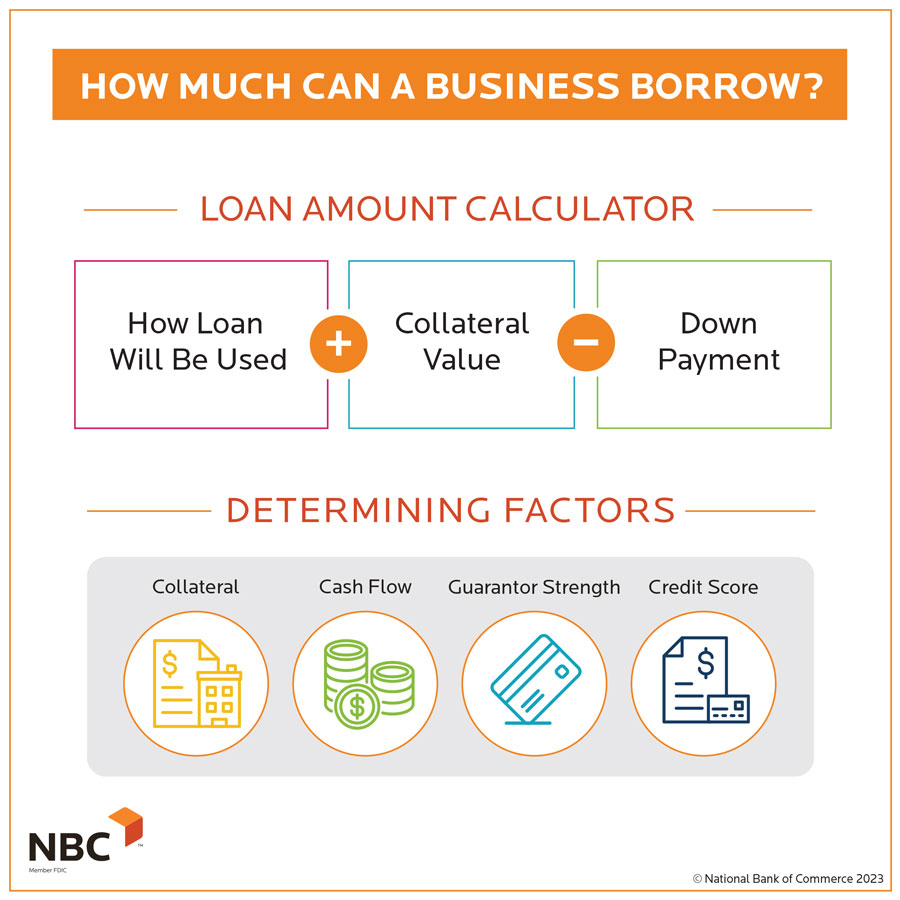

Lenders assess a multitude of variables to determine a business’s creditworthiness and, consequently, the maximum loan amount they are willing to extend. These factors create a comprehensive picture of your business’s risk profile and repayment capacity.

Your Business’s Financial Health and History

The cornerstone of any loan application is your business’s financial performance. Lenders scrutinize historical data to project future viability and repayment ability.

- Revenue and Profitability: Consistent and growing revenue indicates a healthy business capable of generating income. Profitability demonstrates efficient management and the ability to retain earnings. Lenders look for strong gross and net profit margins.

- Cash Flow: Perhaps the most critical metric, positive and consistent cash flow assures lenders that you can service debt obligations. They will analyze your cash flow statements to understand how cash moves in and out of your business. A strong cash flow minimizes the risk of default.

- Debt-to-Equity Ratio: This ratio reveals how much debt your business uses to finance its assets relative to the value of shareholders’ equity. A high ratio suggests a business is heavily leveraged and may struggle with additional debt.

- Credit Score (Business and Personal): Your business credit score (e.g., Dun & Bradstreet PAYDEX score) reflects your company’s payment history with suppliers and other creditors. For small businesses, especially startups, lenders will also heavily weigh the owner’s personal credit score. A strong credit history (both business and personal) signals financial responsibility and can significantly increase your borrowing potential and secure better terms.

Industry and Business Type

The industry in which your business operates plays a substantial role in a lender’s risk assessment.

- Industry Risk: Certain industries are perceived as inherently riskier due to volatility, high startup costs, or unpredictable revenue streams. For instance, a tech startup in a rapidly changing market might face different lending criteria than a long-established manufacturing firm.

- Business Model: Lenders evaluate the stability and scalability of your business model. Businesses with recurring revenue, diversified customer bases, or strong competitive advantages are generally viewed more favorably.

- Time in Business: Established businesses with a proven track record (typically 2+ years) often qualify for larger loan amounts and more favorable terms than startups, which present higher risk due to lack of operating history.

Loan Type and Lender

Different loan products are designed for specific purposes and come with varying qualification criteria and maximum limits. The type of lender also dictates available amounts.

- SBA Loans: Backed by the U.S. Small Business Administration, these loans often have more flexible terms and lower down payments, offering up to $5 million for general business purposes (7(a) loan) or specific real estate and equipment financing (504 loan).

- Traditional Bank Loans: Banks typically offer term loans, lines of credit, and commercial mortgages. They often have stringent requirements but can provide substantial funding amounts for well-established businesses with strong financials.

- Online Lenders/Alternative Lenders: These platforms often provide quicker approvals and cater to businesses that might not qualify for traditional bank loans, though they may come with higher interest rates and potentially smaller maximum amounts. Options include short-term loans, merchant cash advances, or invoice factoring, with limits varying widely based on the lender’s model.

- Equipment Financing: Loans specifically for purchasing equipment are often secured by the equipment itself, allowing businesses to finance up to 100% of the asset’s value.

Collateral and Guarantees

Collateral significantly mitigates a lender’s risk, directly influencing the loan amount.

- Secured vs. Unsecured Loans: Secured loans require assets (real estate, equipment, inventory, accounts receivable) as collateral. The value of these assets often determines the maximum loan amount. Unsecured loans, relying solely on your business’s creditworthiness, typically offer smaller amounts.

- Personal Guarantees: Many small business loans, especially for newer companies, require a personal guarantee from the business owner. This means the owner is personally liable for the debt if the business defaults, further reducing the lender’s risk and potentially increasing the accessible loan amount.

Calculating Your Business’s Borrowing Capacity

Lenders employ specific financial ratios to objectively determine how much debt your business can realistically handle. Understanding these metrics can help you assess your own capacity before approaching a lender.

Debt Service Coverage Ratio (DSCR)

The DSCR is a critical measure used by lenders to evaluate a business’s ability to cover its debt payments. It compares the cash flow available to service debt against the total annual debt service (principal and interest payments).

- Calculation: Net Operating Income / Total Annual Debt Service

- Interpretation: A DSCR of 1.0 means your business generates just enough cash flow to cover its debt payments. Lenders typically look for a DSCR of 1.25 or higher, indicating a healthy buffer. A higher DSCR suggests your business can comfortably take on more debt. For example, a DSCR of 1.50 means your net operating income is 1.5 times your debt obligations, making you a more attractive borrower for larger sums.

Loan-to-Value (LTV) Ratio for Secured Loans

When a loan is secured by specific assets, the LTV ratio is used to determine the maximum loan amount based on the asset’s appraised value.

- Calculation: Loan Amount / Asset’s Appraised Value

- Interpretation: Lenders rarely finance 100% of an asset’s value. For real estate, LTVs might range from 70% to 85%, meaning if your property is valued at $1 million, you might be eligible for a loan up to $700,000 – $850,000. For equipment or inventory, LTVs can vary, often lower due to faster depreciation or liquidity concerns. The lower the LTV from the borrower’s perspective (i.e., the more equity you put in), the less risk for the lender, potentially enabling a larger overall loan or better terms.

Analyzing Your Cash Flow

Beyond the DSCR, a detailed analysis of your cash flow statements provides deeper insights into your borrowing capacity. Lenders will examine:

- Operating Cash Flow: The cash generated from your core business operations. Consistent positive operating cash flow is essential.

- Free Cash Flow: Cash remaining after accounting for capital expenditures. This shows how much cash is truly available for debt repayment or other investments.

- Cash Flow Projections: For growth-oriented loans, lenders will want to see detailed projections of future cash flow, demonstrating how the new funds will contribute to increased revenue and sufficient cash to repay the loan.

Common Loan Types and Their Typical Limits

Understanding the typical ranges for various loan products helps in identifying which type of financing aligns best with your needs and potential eligibility.

SBA Loans

- SBA 7(a) Loan: The most popular SBA program, offering flexible financing for various business purposes (working capital, equipment, real estate, refinancing). Maximum loan amount is $5 million.

- SBA 504 Loan: Designed for long-term fixed assets like real estate or machinery. This program involves a bank loan, an SBA-backed portion (through a Certified Development Company), and borrower equity. The CDC portion has a maximum of $5 million (or $5.5 million for specific public policy goals).

- SBA Microloans: Smaller loans up to $50,000, primarily for startups or businesses needing smaller amounts for working capital or inventory.

Traditional Bank Term Loans

These loans provide a lump sum of capital that is repaid over a fixed period with regular installments.

- Limits: Can range from tens of thousands to several million dollars, heavily dependent on the business’s size, financial strength, and collateral. Well-established companies with strong revenue and collateral can access substantial amounts.

Business Lines of Credit

A flexible financing option that allows businesses to draw funds as needed, up to a pre-set limit, and repay them to free up available credit.

- Limits: Typically range from $5,000 to $500,000, used for managing cash flow fluctuations, inventory purchases, or unexpected expenses. Larger lines of credit are available for highly qualified businesses.

Equipment Financing

Specific loans used to purchase new or used business equipment, with the equipment itself often serving as collateral.

- Limits: Can finance up to 100% of the equipment’s value, as the asset provides inherent security for the lender. Amounts depend directly on the cost of the equipment.

Merchant Cash Advances (MCAs)

An advance on future credit card sales. While not a traditional loan, MCAs provide quick access to capital based on your business’s daily credit card receipts.

- Limits: Usually range from $2,500 to $250,000, though some providers go higher. These are often used by businesses with inconsistent cash flow or those unable to secure traditional financing, often at a higher cost.

Preparing Your Application to Maximize Your Loan Potential

Strategic preparation is key to not only securing a loan but also maximizing the amount and obtaining favorable terms.

Develop a Robust Business Plan

A well-articulated business plan demonstrates your understanding of your market, your operational strategy, and your financial projections. It should include:

- Executive Summary: A concise overview of your business and loan request.

- Market Analysis: Demonstrate a clear understanding of your industry, target market, and competitive landscape.

- Management Team: Highlight the experience and expertise of your leadership.

- Financial Projections: Detailed 3-5 year projections for profit & loss, balance sheets, and cash flow, clearly showing how the loan will be repaid and contribute to growth.

Organize Financial Statements

Lenders require comprehensive financial documentation to assess your business’s health. Have these ready:

- Profit & Loss Statements (Income Statements): Typically for the past 2-3 years, plus year-to-date.

- Balance Sheets: For the past 2-3 years, plus year-to-date.

- Cash Flow Statements: For the past 2-3 years, plus year-to-date.

- Business Tax Returns: For the past 2-3 years.

- Personal Tax Returns: For the business owner(s), usually for the past 2-3 years.

- Bank Statements: Recent months of business bank statements.

Improve Your Credit Profile

Proactively work on strengthening your credit scores:

- Business Credit: Ensure timely payments to all vendors and suppliers. Monitor your business credit reports for accuracy.

- Personal Credit: Maintain a strong personal credit score by paying bills on time, keeping credit utilization low, and addressing any errors on your report.

Understand Your Needs and Loan Purpose

Clearly define why you need the loan and how the funds will be used. A vague purpose can undermine a lender’s confidence. Whether it’s for equipment purchase, working capital, expansion, or inventory, be specific and provide a compelling rationale for how the loan will generate a return or support business stability. A well-defined purpose can often justify a higher loan amount.

Navigating the Application Process and Beyond

The journey to securing a business loan doesn’t end with preparation; careful navigation of the application process and responsible management post-approval are equally critical.

Shop Around for Lenders

Don’t accept the first offer. Different lenders specialize in different types of businesses and industries, and their risk appetites vary. Compare interest rates, fees, repayment terms, and specific requirements from various banks, credit unions, SBA-preferred lenders, and online platforms. A slight difference in interest rate or fees can amount to significant savings over the life of a loan.

Be Realistic with Your Ask

While it’s important to aim for the funding your business genuinely needs, asking for an unrealistic amount can signal a lack of financial acumen or an inability to accurately assess your business’s capabilities. Conversely, asking for too little might suggest you haven’t fully planned for future needs, potentially requiring another loan application sooner than ideal. Strike a balance between your absolute needs and what your business can realistically support. A lender’s role is not just to provide capital but to ensure the borrower can handle it responsibly.

Focus on Debt Management

Once your loan is approved and funds are disbursed, responsible debt management becomes paramount. Adhere strictly to the repayment schedule. Timely payments not only prevent defaults but also contribute positively to your business credit score, enhancing your ability to secure future financing at better terms. Regularly review your cash flow and financial performance to ensure you remain on track, making adjustments to your business operations if necessary to safeguard your ability to meet your obligations.

The amount of a business loan you can get is a direct reflection of your business’s financial health, strategic planning, and the specific needs you present. By understanding these multifaceted factors, preparing thoroughly, and engaging with lenders strategically, you can significantly enhance your chances of securing the optimal funding for your business’s success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.