For millions of service members, veterans, and eligible surviving spouses, the VA home loan program stands as one of the most significant and well-deserved benefits earned through their dedication to our nation. When contemplating this powerful financial tool, the question “how much is the VA home loan?” often arises. However, this isn’t a simple query with a single dollar figure answer. Instead, understanding “how much” involves delving into the multifaceted value of the program, encompassing not just loan amounts but also unparalleled savings, flexible terms, and increased accessibility to homeownership. This article aims to demystify the VA home loan, explaining its financial advantages and empowering eligible individuals to leverage this invaluable benefit.

Understanding the VA Home Loan: More Than Just a Number

The VA home loan program is not a loan from the Department of Veterans Affairs itself, but rather a guarantee to approved private lenders. This guarantee significantly reduces the risk for lenders, enabling them to offer more favorable terms than conventional mortgages. It’s a testament to the nation’s commitment to those who have served, providing a tangible pathway to achieving the American dream of homeownership.

What is a VA Home Loan?

At its core, a VA home loan is a mortgage program designed to help eligible veterans, service members, and certain military spouses purchase, construct, or refinance a home. Established in 1944 as part of the GI Bill, its primary goal was to aid returning World War II veterans in re-establishing their civilian lives. Today, it remains a cornerstone of veteran benefits, characterized by its unique advantages that distinguish it from virtually all other mortgage options. The most celebrated feature, and often the first benefit people associate with the program, is the possibility of purchasing a home with 0% down payment. This single feature can dramatically lower the barrier to entry for homeownership, especially for younger service members or those who haven’t had the chance to save a substantial down payment.

The Concept of “How Much” in VA Loans

When people ask “how much is the VA home loan?”, they’re typically trying to ascertain two main things:

- What is the maximum amount I can borrow?

- What are the financial benefits and savings associated with it?

The VA home loan isn’t a direct cash payout; it’s an entitlement that the VA provides to an eligible borrower. This entitlement guarantees a portion of the loan amount to the lender, typically 25%. This guarantee is what allows lenders to be so flexible with their terms, particularly regarding the down payment. For most eligible borrowers with full entitlement, there are no maximum VA loan limits, meaning they can finance the full purchase price of a home without a down payment, even for larger loans, as long as they qualify with the lender. This is a significant recent change from previous years when VA loan limits mirrored conforming loan limits. However, lenders still have their own internal lending limits based on a borrower’s financial qualifications.

Key Benefits Beyond the Down Payment

While the 0% down payment is a tremendous draw, the VA home loan program offers a suite of other financial advantages that significantly impact the “how much” in terms of long-term savings:

- No Private Mortgage Insurance (PMI): Unlike conventional loans with less than 20% down, VA loans do not require PMI, which can save borrowers hundreds of dollars per month. This alone can translate into tens of thousands of dollars in savings over the life of the loan.

- Competitive Interest Rates: Due to the VA guarantee, lenders view VA loans as lower risk, often resulting in interest rates that are lower than or comparable to conventional loans. Over a 30-year mortgage, even a slightly lower interest rate can save a substantial amount.

- Limited Closing Costs: The VA limits the closing costs that veterans can be charged, and in some cases, sellers are permitted to pay all of a buyer’s loan-related closing costs and even offer concessions to cover other expenses. This further reduces the out-of-pocket expenses for the buyer.

- Easier Qualification Compared to Conventional Loans: While lenders still scrutinize creditworthiness and income, VA loan guidelines are often more forgiving regarding credit scores and debt-to-income (DTI) ratios compared to conventional mortgages, making homeownership accessible to a wider range of service members and veterans.

Demystifying VA Loan Limits and Entitlement

To truly grasp “how much” you can borrow with a VA loan, it’s essential to understand the concepts of entitlement and loan limits. These two elements define the VA’s financial backing and how much a lender is willing to extend.

Full Entitlement vs. Partial Entitlement

Your VA loan entitlement is the amount the VA will guarantee to the lender on your behalf.

- Full Entitlement: This is the most common scenario for first-time VA loan users. With full entitlement, you can purchase a home with no money down, regardless of the loan amount, as long as you meet the lender’s income and credit requirements. The VA guarantees 25% of the loan amount, up to the maximum VA loan limits if those limits are still applicable (which for most with full entitlement, they are not).

- Partial Entitlement: This applies if you’ve used your VA loan benefit before and haven’t fully restored your entitlement (e.g., you still own a home financed with a VA loan, or you’ve defaulted on a previous VA loan). In such cases, the VA will guarantee a remaining portion of your entitlement. If your remaining entitlement is less than 25% of the new loan amount, you may need to make a down payment to cover the difference. The calculation can be complex, but an experienced VA lender can help determine your specific situation.

Understanding VA Loan Limits (and When They Apply)

A significant change took effect on January 1, 2020. For eligible veterans with full entitlement, the VA removed the VA loan limits, meaning there’s no cap on the loan amount for which the VA will guarantee 25%. This is a huge benefit, especially in high-cost housing markets.

However, VA loan limits do still come into play in specific situations:

- Borrowers with Partial Entitlement: If you have partial entitlement, the VA will use the applicable loan limits for your area to determine your remaining entitlement and whether a down payment is required for a new purchase.

- Jumbo VA Loans: While the VA itself doesn’t cap the loan amount for those with full entitlement, lenders may have their own internal “jumbo” loan limits. If your loan amount exceeds the conventional conforming loan limits (set by the Federal Housing Finance Agency, or FHFA), it might be considered a jumbo loan. Even without VA limits, lenders might apply stricter underwriting rules or require higher credit scores for very large loans.

- County-Specific Limits: While the blanket VA loan limits are gone for those with full entitlement, some lenders still refer to the FHFA conforming loan limits, which can vary by county in high-cost areas. It’s crucial to work with a lender who understands how these nuances might affect your specific borrowing power.

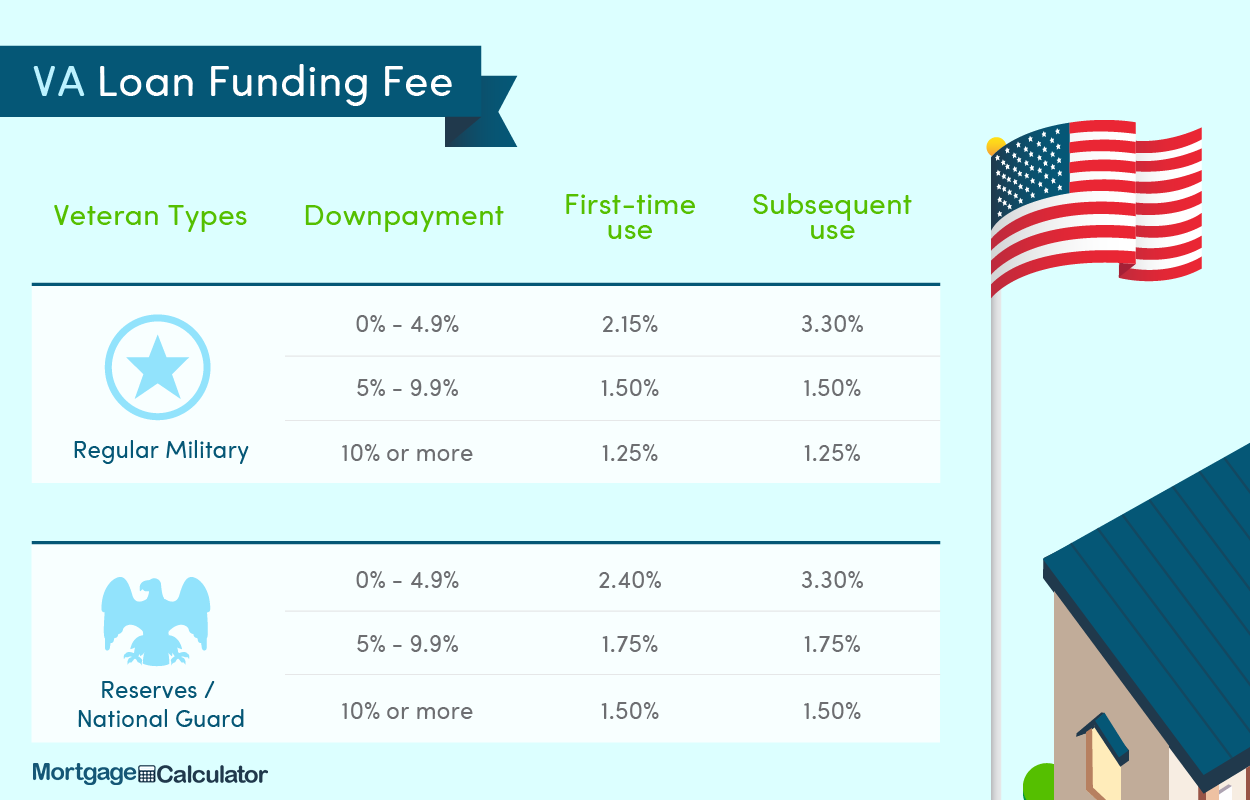

The VA Funding Fee Explained

The VA funding fee is another crucial component of “how much” a VA loan costs. This one-time fee is paid directly to the VA to help offset the program’s costs to U.S. taxpayers and reduce its burden on the federal budget. It’s a percentage of the loan amount and varies based on several factors:

- Loan Type: Purchase, refinance (IRRRL vs. Cash-Out).

- Down Payment Amount: For purchase loans, a larger down payment can reduce the fee.

- Previous Use: Whether it’s your first time using the VA loan or a subsequent use.

For instance, a first-time VA loan user purchasing with 0% down might pay a funding fee of 2.15% of the loan amount. A subsequent user with 0% down might pay 3.3%. This fee can typically be financed into the loan, increasing your total loan amount but avoiding an upfront out-of-pocket expense.

Exemptions: Crucially, some veterans are exempt from paying the VA funding fee. These generally include:

- Veterans receiving VA compensation for a service-connected disability.

- Veterans who would be entitled to receive VA compensation for a service-connected disability if they didn’t receive retirement or active duty pay.

- Surviving spouses of veterans who died in service or from a service-connected disability.

If you are exempt, this represents another significant saving, adding to the overall value of the VA home loan benefit.

Calculating Your Potential VA Home Loan Power

While the VA provides the entitlement, it’s the lender who ultimately determines “how much” they are willing to lend you. This calculation involves a thorough assessment of your financial health.

Factors Influencing Your Loan Amount

Lenders look at a holistic view of your financial situation to determine your maximum loan amount:

- Credit Score: While VA guidelines are more flexible than conventional loans, a higher credit score (typically 620+) demonstrates a strong repayment history and can lead to better interest rates and easier approval.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. The VA typically looks for a DTI of 41% or lower, though exceptions can be made with strong compensating factors.

- Income Stability and Employment History: Lenders want to see a consistent and reliable income stream. This means stable employment, typically for at least two years. Military income (base pay, BAH, BAS, special pay) is generally considered very stable.

- Residual Income Requirements: Unique to VA loans, residual income is the amount of discretionary income left over each month after all major expenses (debts, housing costs, taxes) are paid. The VA sets minimum residual income guidelines based on family size and geographic region, ensuring borrowers have enough money for living expenses. This requirement acts as an extra layer of protection for borrowers, making sure they aren’t overleveraged.

The Role of the Lender in “How Much”

While the VA sets broad guidelines, individual VA-approved lenders can implement their own lender overlays. These are additional requirements on top of the VA’s minimums. For example, a lender might require a slightly higher credit score than the VA’s unofficial minimum, or they might have stricter DTI limits. This is why it’s critical to:

- Get Pre-Approved: A VA loan pre-approval is a vital first step. It involves a lender reviewing your financial information and giving you a realistic estimate of how much you can borrow. This not only clarifies your budget but also makes your offer more attractive to sellers.

- Work with a VA-Experienced Lender: Not all lenders are equally proficient in handling VA loans. Choosing a lender with extensive experience in the program can make a significant difference in navigating the process efficiently and maximizing your benefits.

Comparing VA Loans to Other Options

To truly appreciate the value of “how much” the VA home loan offers, it’s useful to compare it with alternatives:

- Conventional Loans: Typically require a minimum of 3-5% down payment, often more to avoid PMI. They have stricter credit score and DTI requirements.

- FHA Loans: Allow for down payments as low as 3.5% but require both an upfront mortgage insurance premium and annual mortgage insurance premiums, which are similar to PMI but cannot be removed without refinancing or selling.

The VA loan consistently stands out for its 0% down payment (for most), no PMI, and often more flexible underwriting, translating into lower monthly payments and reduced upfront costs for eligible borrowers.

The Application Process: From Eligibility to Closing

Navigating the VA home loan process doesn’t have to be daunting. Understanding the key steps will streamline your journey to homeownership.

Obtaining Your Certificate of Eligibility (COE)

The Certificate of Eligibility (COE) is the official document from the VA that proves you meet the eligibility requirements for a VA loan and states your entitlement amount. You can obtain your COE in several ways:

- Online through the VA’s eBenefits portal: This is often the quickest method.

- Through your chosen VA-approved lender: Most lenders can retrieve your COE electronically on your behalf.

- By mail: You can apply by mail using VA Form 26-1880, “Request for Certificate of Eligibility.”

Your COE will confirm your eligibility and detail how much entitlement you have available, which is crucial for the lender to determine your maximum loan amount and any potential down payment requirements.

Finding a VA-Approved Lender and Realtor

The success of your VA home loan journey often hinges on the professionals you choose:

- VA-Approved Lender: As mentioned, select a lender with a strong track record and specialized knowledge of VA loans. They will guide you through the specific documentation, requirements, and nuances of the program.

- VA-Experienced Realtor: A realtor who understands the VA loan process is equally important. They will be familiar with VA appraisal requirements (Minimum Property Requirements, or MPRs), can help you find suitable properties, and can effectively negotiate with sellers who may not be fully informed about VA loans.

Understanding Key Steps and Documents

The VA home loan process involves standard mortgage steps with a few VA-specific considerations:

- Loan Application: Provide your financial information, employment history, and authorization for a credit check.

- Appraisal and Property Requirements: The VA requires a VA-specific appraisal to determine the home’s value and ensure it meets Minimum Property Requirements (MPRs). MPRs are designed to ensure the home is safe, sanitary, and structurally sound.

- Underwriting: The lender reviews all your documentation (income, assets, credit, COE, appraisal) to determine if you qualify for the loan.

- Closing: Once approved, you’ll sign all the necessary documents to finalize the loan and transfer property ownership.

Maximizing Your VA Home Loan Benefit

The VA home loan is a lifelong benefit, and understanding how to use it strategically can yield even greater financial advantages.

Leveraging Your Entitlement Wisely

- First-Time Use vs. Subsequent Uses: While the first use typically comes with a lower funding fee, subsequent uses are also incredibly valuable. If you sell your home and pay off your VA loan, you can apply to restore your full entitlement and use the benefit again. In some cases, you can even use a portion of your entitlement a second time without selling, if you have sufficient “remaining entitlement.”

- Restoring Entitlement: The most common way to restore your full entitlement is to sell your home financed by a VA loan and pay off the loan in full. In certain situations, you can also restore entitlement by refinancing out of a VA loan into a non-VA loan.

Financial Planning Around Your VA Loan

While a VA loan offers significant savings, responsible financial planning is still crucial:

- Budget for Property Taxes, Insurance, and Maintenance: These costs are not included in your VA loan principal and interest payment. Ensure you budget for property taxes, homeowners insurance, and ongoing home maintenance to avoid financial strain.

- Understanding Long-Term Financial Implications: The decision to take on a mortgage, even a highly beneficial VA loan, is a long-term financial commitment. Consider your career plans, family growth, and other financial goals.

Beyond Home Purchase: VA Refinance Options

The VA also offers robust refinance options, allowing you to maximize your benefit even after you’ve purchased your home:

- Interest Rate Reduction Refinance Loan (IRRRL): Often called a “VA Streamline Refinance,” the IRRRL is designed to help veterans refinance an existing VA loan to get a lower interest rate, or convert an adjustable-rate mortgage (ARM) to a fixed-rate mortgage. It typically requires less paperwork, no appraisal, and no credit underwriting.

- Cash-Out Refinance: This option allows you to refinance an existing VA or non-VA loan into a VA loan, taking cash out from your home equity. This cash can be used for anything, from home improvements to debt consolidation, and is limited by the amount of equity you have in your home.

Conclusion

The question “how much is the VA home loan?” opens the door to a comprehensive understanding of one of the most powerful financial benefits available to our nation’s service members, veterans, and eligible spouses. It’s not about a fixed dollar amount but rather the immense value derived from 0% down payment options, the absence of private mortgage insurance, competitive interest rates, and overall flexible qualification requirements. These advantages translate into substantial savings—tens or even hundreds of thousands of dollars—over the life of a loan, making homeownership more accessible and affordable.

By understanding your entitlement, navigating loan limits, and working with experienced professionals, you can fully leverage this earned benefit. The VA home loan is more than just a mortgage; it’s a testament to appreciation for service, a gateway to financial stability, and a cornerstone for building a future. For those who have sacrificed so much for our country, exploring and utilizing this invaluable program is a wise and deserved financial decision.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.