Navigating the world of car insurance can often feel like deciphering a complex financial puzzle, especially when trying to understand the cost of “full coverage” from a major provider like Progressive. As a cornerstone of personal finance, understanding your insurance expenditures is crucial for effective budgeting and safeguarding your assets. This article aims to demystify what full coverage car insurance entails, explore the myriad factors that influence its cost specifically with Progressive, and provide actionable insights into managing your premiums. By the end, you’ll have a clearer picture of what to expect and how to make informed financial decisions regarding your vehicle protection.

Understanding “Full Coverage” in Car Insurance: More Than Just a Catchphrase

The term “full coverage” is ubiquitous in the car insurance industry, yet it’s often misunderstood. Contrary to popular belief, it’s not a single, all-encompassing policy type that covers every possible scenario. Instead, “full coverage” is a colloquial term that typically refers to a combination of several distinct insurance coverages designed to provide comprehensive financial protection against a wide range of incidents. For any financially prudent individual, grasping these components is the first step toward understanding their investment.

Demystifying Common Misconceptions

Many consumers assume “full coverage” means absolutely nothing is excluded. However, every policy has its limits, deductibles, and exclusions. For instance, while it protects your car, it generally doesn’t cover personal items stolen from your vehicle or mechanical breakdowns not caused by an accident. The “full” aspect refers to protecting you not just from damage you cause to others, but also from damage to your own vehicle, and often from non-collision events as well. This robust approach to protection is what makes it a significant line item in many household budgets.

Components of a Comprehensive Full Coverage Policy

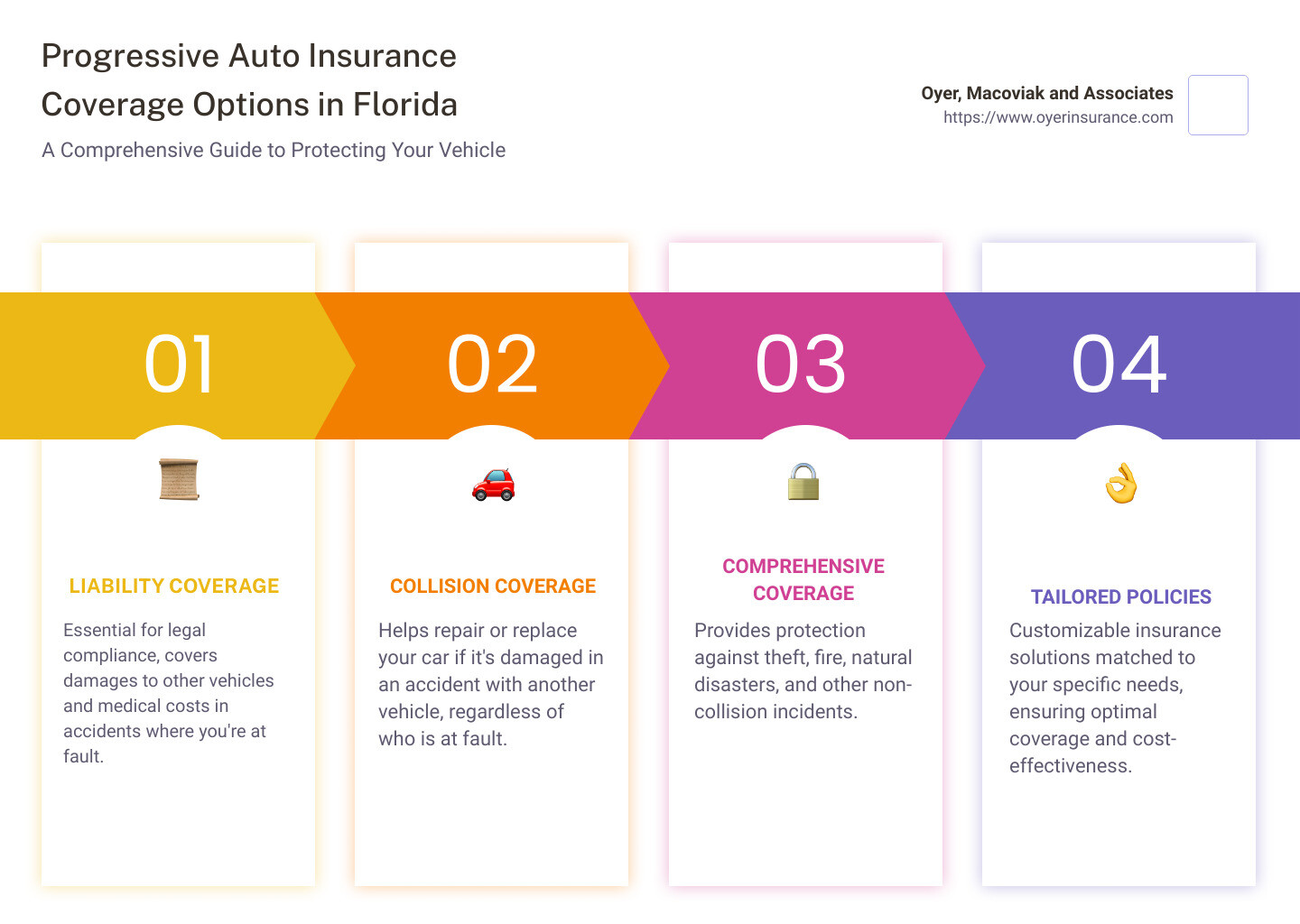

A standard “full coverage” policy with Progressive, or any insurer, typically bundles three core types of protection:

- Liability Coverage: This is the foundational component and often legally mandated. It comprises:

- Bodily Injury Liability (BIL): Covers medical expenses, lost wages, and pain and suffering for others if you’re at fault in an accident. State laws dictate minimum coverage limits, but financially savvy individuals often opt for higher limits to protect their assets from potential lawsuits.

- Property Damage Liability (PDL): Covers damage you cause to another person’s property (e.g., their car, fence, building) in an at-fault accident.

- Collision Coverage: This pays for damages to your vehicle resulting from a collision with another car or object, regardless of who is at fault. This includes hitting a tree, another car, or rolling over. It’s an indispensable coverage for protecting your investment in your vehicle.

- Comprehensive Coverage: Often called “Other Than Collision,” this protects your vehicle from damages not caused by a collision. This includes theft, vandalism, fire, natural disasters (hail, floods), falling objects, and animal collisions. For those with car loans or leases, both collision and comprehensive coverage are almost always mandatory requirements from the lender, highlighting their financial importance.

Beyond the Basics: Add-ons for Enhanced Protection

While the core three define “full coverage,” Progressive also offers additional endorsements that can be bundled to further enhance your financial security:

- Uninsured/Underinsured Motorist (UM/UIM) Coverage: Protects you if you’re hit by a driver who has no insurance or insufficient insurance to cover your damages and medical bills. This is a critical financial safeguard in many states.

- Medical Payments (MedPay) or Personal Injury Protection (PIP): Covers medical expenses for you and your passengers, regardless of fault. PIP can also cover lost wages and essential services.

- Roadside Assistance: Provides help with flat tires, dead batteries, lockouts, and towing. A small annual fee can save significant costs in an emergency.

- Rental Car Reimbursement: Covers the cost of a rental car while your vehicle is being repaired after a covered incident.

- Gap Insurance: Crucial for newer cars, this pays the difference between your car’s actual cash value (ACV) and the amount you still owe on your loan or lease if your car is totaled. Without it, you could face substantial out-of-pocket costs.

Each of these add-ons increases your premium but offers a layer of financial protection that can prevent much larger expenses down the line. Deciding which ones are necessary involves a careful assessment of your personal financial situation, risk tolerance, and car’s value.

Factors Influencing Your Progressive Full Coverage Premium

The question “how much is Progressive car insurance full coverage” doesn’t have a single answer because premiums are highly individualized. Progressive, like other insurers, uses a sophisticated algorithm that analyzes a vast array of data points to assess risk and set prices. Understanding these factors is key to predicting and potentially lowering your financial outlay.

Personal Profile: Driver Demographics and Driving Record

Your personal characteristics are paramount in determining your premium:

- Age and Gender: Younger, less experienced drivers, particularly males, often face higher premiums due to statistical higher accident rates. As drivers mature, rates generally decrease, assuming a clean record.

- Driving Record: This is arguably the most significant factor. Accidents, traffic violations (speeding tickets, DUIs), and claims history directly correlate with higher premiums. A clean driving record is your best financial asset for lower insurance costs.

- Credit Score: In many states, your credit-based insurance score (which is related to, but distinct from, your credit score) plays a role. Statistically, individuals with higher credit scores tend to file fewer claims. Maintaining good credit can thus contribute to lower insurance costs, emphasizing its broader financial impact.

- Marital Status: Married individuals often receive slightly lower rates, as statistics suggest they are less likely to be involved in accidents.

Vehicle Characteristics: Make, Model, Age, and Safety Features

The car you drive significantly impacts the cost of collision and comprehensive coverage:

- Make, Model, and Year: Luxury, sports, and high-performance vehicles typically cost more to insure due to higher repair costs, greater likelihood of theft, and higher potential for speed-related accidents. Conversely, older, more common models are often cheaper.

- Safety Features: Cars equipped with advanced safety features (e.g., anti-lock brakes, airbags, adaptive cruise control, lane departure warning) often qualify for discounts because they reduce the risk of accidents or severe injuries.

- Anti-Theft Devices: Vehicles with alarm systems, GPS trackers, or immobilizers can also receive discounts on comprehensive coverage.

Geographic Location: Where You Live and Drive

Your address has a surprising financial impact on your premiums:

- Zip Code: Urban areas with higher traffic density, crime rates (leading to more theft/vandalism claims), and higher accident frequencies generally have higher premiums than rural areas.

- Garaging Location: Where your car is typically parked (e.g., in a secure garage vs. on the street) can also influence rates.

- Commute Distance: Drivers with longer daily commutes or those who drive during peak hours may face higher premiums due to increased exposure to accident risks.

Policy Details: Deductibles, Limits, and Payment Plans

The choices you make when configuring your policy directly affect the premium:

- Deductibles: This is the amount you pay out-of-pocket before your insurance kicks in for collision and comprehensive claims. Choosing a higher deductible (e.g., $1,000 instead of $500) will lower your premium, but you must ensure you have the emergency funds available to cover that deductible should a claim arise. This is a crucial financial decision.

- Coverage Limits: Higher liability limits, while offering greater protection, also result in higher premiums. Balancing financial protection against affordability is key.

- Payment Frequency: Paying your premium in full for the entire policy period (usually six months or a year) often results in a small discount compared to monthly installments, saving you money on administrative fees.

Progressive’s Approach to Full Coverage and Cost Savings

Progressive is known for its innovative approach to insurance and its direct-to-consumer model. They offer various tools and discounts designed to help policyholders manage their costs, making them a competitive option for financially astute consumers.

Progressive-Specific Discounts You Can Leverage

Progressive provides a robust suite of discounts that can significantly reduce your full coverage premium:

- Multi-Policy Discount (Bundling): This is one of the most substantial discounts. By bundling your auto insurance with other policies like home, renters, motorcycle, or RV insurance, you can often save a considerable percentage on your total premiums. This is a smart financial strategy for consolidating insurance needs.

- Snapshot® Program: This telematics program monitors your driving habits (miles driven, braking, time of day, etc.) via a mobile app or a device plugged into your car. Safe drivers can earn significant discounts. It requires a willingness to share data but can be very rewarding financially.

- Multi-Car Discount: Insuring more than one vehicle on the same Progressive policy can lead to savings.

- Good Driver/Accident Forgiveness: While not a discount per se, their “Accident Forgiveness” feature (sometimes an add-on, sometimes earned) prevents your rates from increasing after your first minor accident, safeguarding your financial stability post-incident.

- Online Quote & Sign Discount: Simply getting a quote online and purchasing your policy digitally can yield a small discount.

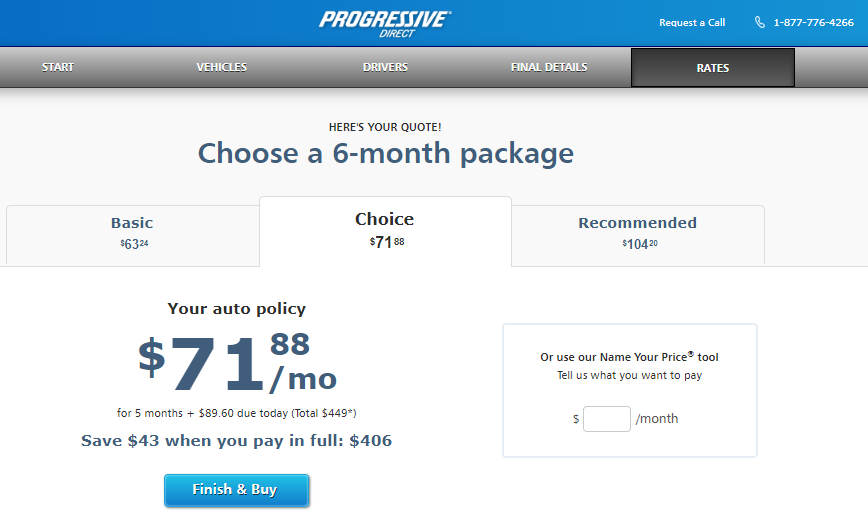

- Name Your Price® Tool: While not a direct discount, this unique tool allows you to specify a budget and see the coverage options that fit, helping you tailor your policy to your financial constraints.

- Other Discounts: Look for discounts related to good student status, distant student, homeowner, paperless billing, and automatic payments. Each small discount adds up.

Tools and Programs to Personalize Your Quote

Progressive’s online platform is designed to empower consumers to customize their coverage and understand pricing:

- Online Quoting System: Progressive’s user-friendly online quote tool allows you to input your information, select coverages, and see estimated premiums instantly. This transparency helps you compare options and adjust deductibles/limits to fit your budget.

- Snapshot® and the “Name Your Price®” Tool: These are key financial planning tools offered by Progressive, allowing for dynamic pricing adjustments based on real-world data and personal budget constraints.

- Customer Service Agents: While online tools are great, Progressive’s agents are available to walk you through options, explain complex coverages, and help you uncover additional savings tailored to your situation.

The Importance of Regular Policy Reviews

Your insurance needs and financial situation are not static. It’s financially prudent to review your Progressive full coverage policy at least annually or whenever significant life changes occur (e.g., buying a new car, moving, marriage, adding a new driver, paying off a car loan). These reviews ensure you’re not overpaying for coverage you no longer need or under-insured for new risks.

Strategies for Reducing Your Progressive Full Coverage Costs

While many factors influence your premium, you have considerable control over several elements that can help you reduce the financial burden of full coverage.

Maximizing Discounts and Bundling Opportunities

Actively seek out every discount you qualify for. The multi-policy discount is often the most impactful. If you have homeowners or renters insurance elsewhere, get a quote for bundling it with Progressive auto insurance. Don’t shy away from the Snapshot program if you’re a safe driver; the savings can be substantial. Regularly check Progressive’s website or speak with an agent to ensure you’re aware of all available discounts.

Adjusting Deductibles and Coverage Limits Wisely

Evaluate your emergency fund. If you have sufficient savings to comfortably cover a $1,000 deductible, increasing it from $500 could save you hundreds annually on your premium. However, never choose a deductible you can’t afford. Similarly, review your liability limits. While higher limits offer more protection, if your assets are minimal, you might consider lower, state-minimum-plus limits to reduce costs, though this carries higher personal risk. For older cars with low market value, you might even consider dropping collision and comprehensive coverage altogether, weighing the cost of premiums against the car’s actual cash value.

Maintaining a Clean Driving Record

This cannot be overstated. A clean driving record is the golden ticket to lower insurance rates. Avoid accidents, speeding tickets, and other traffic violations. These incidents not only increase your premium for several years but can also make you ineligible for certain good driver discounts. Defensive driving courses can sometimes also offer a small discount.

Comparing Quotes (Even with Progressive)

Even if you love Progressive, it’s financially smart to periodically compare quotes from other insurers. The insurance market is competitive, and rates can change. Progressive offers their “Name Your Price” tool, and while useful, also use independent comparison sites or work with an independent agent to get a broad view of the market. Loyalty doesn’t always pay when it comes to insurance; securing the best financial value often requires shopping around.

Is Progressive Full Coverage Right For You?

The decision to opt for full coverage, and specifically with Progressive, boils down to a personal financial assessment.

Weighing the Benefits Against the Costs

Full coverage offers unparalleled peace of mind, protecting your assets from significant financial setbacks resulting from accidents, theft, or natural disasters. For new cars, financed vehicles, or those with significant equity, it’s often a non-negotiable financial safeguard. However, for older cars with low market value, the cost of full coverage might outweigh the potential payout in a total loss scenario. A simple calculation: if your annual premium for collision and comprehensive coverage approaches 10% or more of your car’s actual cash value, it might be time to reconsider these specific coverages.

The Value of Peace of Mind

For many, the slightly higher premium for full coverage is a worthwhile investment for the financial security and emotional relief it provides. Knowing that your vehicle is protected and that you won’t face astronomical out-of-pocket expenses after an unexpected event can significantly reduce financial stress. This intangible benefit is a crucial part of the value proposition.

When to Consider Alternative Coverage Levels

If your car is paid off, older, and has a low resale value, you might consider reducing your coverage to liability-only. However, remember this leaves you personally responsible for any damage to your own vehicle. It’s a financial gamble that depends heavily on your comfort with risk and your ability to absorb the cost of repair or replacement out-of-pocket. Regularly re-evaluate your situation, considering your vehicle’s depreciation and your financial health.

Ultimately, determining “how much is Progressive car insurance full coverage” is a dynamic process unique to each individual. By understanding the components of full coverage, the factors influencing premiums, and the specific tools and discounts Progressive offers, you can make an informed financial decision that balances comprehensive protection with affordability, ensuring your car insurance aligns perfectly with your broader financial strategy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.