Navigating the landscape of health insurance can often feel like deciphering a complex financial puzzle, and understanding the cost of Kaiser Permanente insurance is a common starting point for many. Kaiser Permanente, renowned for its integrated healthcare delivery system, offers a unique model that can significantly influence both the cost and the experience of care. Unlike traditional insurance companies that primarily pay for services from external providers, Kaiser Permanente functions as both an insurer and a healthcare provider. This distinctive structure means that when you pay for Kaiser insurance, you’re not just buying a health plan; you’re gaining access to an entire ecosystem of doctors, hospitals, pharmacies, and labs operating under one umbrella.

The question “how much is Kaiser insurance?” doesn’t have a single, straightforward answer. The cost is highly variable, depending on a multitude of factors specific to the individual, the plan chosen, and the geographic location. From monthly premiums to out-of-pocket expenses like deductibles and copayments, a comprehensive understanding requires delving into the various components that contribute to the total cost of your healthcare. This article aims to demystify these costs, providing a detailed breakdown of what to expect when considering Kaiser Permanente for your health insurance needs, and equipping you with the knowledge to make an informed financial decision.

Decoding Kaiser Permanente’s Unique Healthcare Model

To truly understand the cost of Kaiser Permanente insurance, it’s essential to first grasp the fundamentals of its operational model. This integrated system is not just a differentiator; it’s a foundational element that shapes its pricing, service delivery, and ultimately, the financial experience for its members.

Integrated Care: A Key Differentiator

Kaiser Permanente operates on an integrated managed care model. This means that the health plan, hospitals, and medical groups are all part of the same organization. When you enroll in a Kaiser Permanente plan, you primarily receive care from Kaiser-affiliated doctors, hospitals, and clinics. This vertical integration allows for a high degree of coordination among providers, often leading to streamlined communication, shared electronic medical records, and a more cohesive patient experience. For example, your primary care physician, specialist, and even the pharmacy might all be in the same building or part of the same network, using the same system.

From a cost perspective, this integrated model can offer several advantages. By controlling the entire care delivery process, Kaiser Permanente aims to reduce administrative overhead, minimize duplication of services, and focus on preventive care to manage long-term health, which can, in turn, help control overall healthcare costs. While this doesn’t always translate into the absolute lowest premiums for every individual, it often means predictable costs and a system designed to keep you healthy, potentially reducing the need for expensive interventions down the line.

HMO Focus: What It Means for You

The vast majority of Kaiser Permanente plans are structured as Health Maintenance Organizations (HMOs). An HMO plan typically requires you to choose a primary care physician (PCP) within the Kaiser Permanente network who then coordinates all your care. If you need to see a specialist, your PCP will usually provide a referral. With an HMO, care received outside the network is generally not covered, except in emergencies.

This HMO structure is a critical factor in how Kaiser Permanente manages costs. By channeling members through its own network and requiring referrals for specialists, the organization can better manage utilization of services and negotiate bulk purchasing of medical supplies and pharmaceuticals. For the member, this often means lower monthly premiums compared to PPO (Preferred Provider Organization) plans offered by other insurers that allow more flexibility in choosing providers. However, the trade-off is often less flexibility in provider choice; if you have specific doctors outside the Kaiser Permanente network you wish to see, an HMO plan may not be the right fit for you. Understanding this constraint is crucial, as sticking to the network is key to avoiding significant out-of-pocket expenses.

Factors Influencing Your Kaiser Permanente Premium

Determining the exact cost of a Kaiser Permanente insurance premium is complex, as it hinges on several dynamic factors. These elements are not unique to Kaiser but are standard considerations across the health insurance industry, shaped by regulatory frameworks and actuarial science.

Age, Location, and Household Size

These are fundamental demographic factors that significantly impact your premium.

- Age: Generally, younger individuals pay lower premiums than older individuals, as health risks tend to increase with age. The Affordable Care Act (ACA) limits how much insurers can vary premiums based on age, capping the ratio at 3:1 for older versus younger adults.

- Location: Healthcare costs, network availability, and competition among insurers vary by geographic region, state, and even specific zip code. Urban areas might have different pricing structures compared to rural ones due to varying costs of living and medical facilities.

- Household Size: If you’re enrolling yourself, your spouse, and/or dependent children, the premium will naturally increase. Each additional person on the policy adds to the overall cost, though sometimes children are priced differently than adults.

Plan Tier and Deductibles

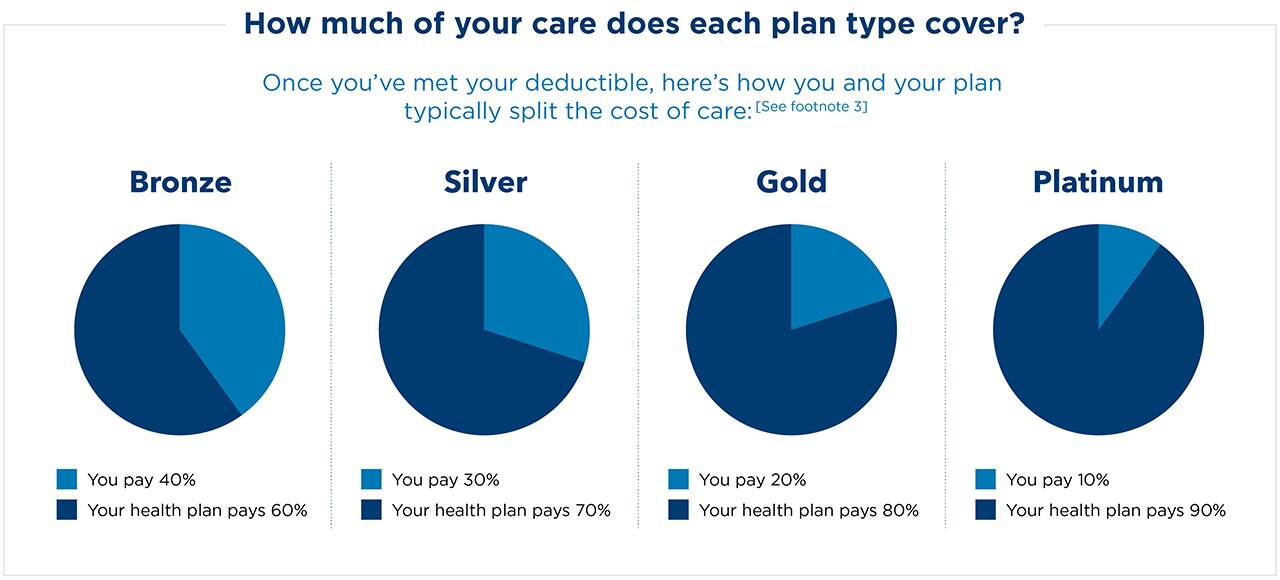

Kaiser Permanente, like other insurers, offers plans categorized into different metallic tiers under the ACA marketplace: Bronze, Silver, Gold, and Platinum. These tiers reflect the actuarial value of the plan, or the average percentage of healthcare costs the plan is expected to cover.

- Bronze plans typically have the lowest monthly premiums but the highest deductibles and out-of-pocket costs when you need care. They cover about 60% of average healthcare costs.

- Silver plans offer a balance of moderate premiums and moderate deductibles, covering around 70% of costs. They are also the only plans eligible for cost-sharing reductions (CSRs) for eligible low-income individuals.

- Gold plans have higher monthly premiums but lower deductibles and out-of-pocket costs, covering about 80% of costs.

- Platinum plans have the highest premiums but the lowest deductibles and out-of-pocket maximums, covering approximately 90% of costs.

Your choice of a deductible also directly influences your premium. A higher deductible means you pay more out of pocket before your insurance starts to cover costs, but it typically results in a lower monthly premium. Conversely, a lower deductible means higher monthly premiums.

Subsidies and Financial Assistance

Many individuals and families may not pay the sticker price for Kaiser Permanente plans purchased through state or federal health insurance marketplaces. The ACA provides financial assistance in the form of tax credits (premium subsidies) and cost-sharing reductions (CSRs).

- Premium Tax Credits: These subsidies reduce your monthly premium based on your household income relative to the federal poverty level. They are available to individuals and families earning between 100% and 400% (or even higher in some cases due to recent legislation) of the federal poverty level who do not have access to affordable employer-sponsored coverage.

- Cost-Sharing Reductions (CSRs): These subsidies reduce the amount you have to pay for deductibles, copayments, and coinsurance. They are available to individuals and families earning up to 250% of the federal poverty level and are only applicable to Silver plans.

It’s crucial to check your eligibility for these subsidies through your state’s health insurance marketplace or Healthcare.gov, as they can significantly lower your actual out-of-pocket premium costs.

Beyond the Premium: Understanding Out-of-Pocket Expenses

While the monthly premium is the most visible cost, it’s only one piece of the financial puzzle. To truly understand “how much is Kaiser insurance,” you must account for the out-of-pocket expenses you will incur when you actually use your health benefits.

Deductibles, Copayments, and Coinsurance Explained

These three terms represent the most common forms of cost-sharing that members are responsible for:

- Deductible: This is the amount you must pay out of pocket for covered healthcare services before your insurance plan starts to pay. For example, if you have a $3,000 deductible, you would pay the first $3,000 in covered medical expenses (excluding certain preventive services, which are often covered 100% before the deductible) before Kaiser Permanente begins to contribute.

- Copayment (Copay): A fixed amount you pay for a covered healthcare service after you’ve paid your deductible (though some plans may have copays that apply before the deductible for certain services, like doctor visits). For instance, you might have a $30 copay for a primary care visit or a $50 copay for a specialist visit.

- Coinsurance: This is your share of the cost of a covered healthcare service, calculated as a percentage of the allowed amount for the service, after you’ve paid your deductible. If your plan’s coinsurance is 20% and the allowed amount for a service is $100, you would pay $20, and the insurance would pay $80.

With Kaiser Permanente, these costs are clearly outlined in your plan documents. Their integrated system often makes it easier to track these expenses, as all services are typically billed through the same organization.

Out-of-Pocket Maximums: Your Financial Safety Net

The out-of-pocket maximum (or limit) is a critical financial protection feature of any health insurance plan. This is the most you will have to pay for covered services in a plan year. Once you hit this limit, your health plan pays 100% of the costs for covered benefits for the remainder of the year. This limit includes deductibles, copayments, and coinsurance, but it generally does not include your monthly premiums.

Understanding your plan’s out-of-pocket maximum is vital for budgeting and financial planning. It provides a cap on your potential financial liability in case of a serious illness or injury, offering peace of mind that medical emergencies won’t lead to unlimited debt. When comparing Kaiser plans, always look beyond just the premium and consider the worst-case out-of-pocket scenario.

Prescription Drug Costs

Prescription drug coverage is an integral part of most Kaiser Permanente plans. The cost of your medications typically depends on the drug’s tier (e.g., generic, preferred brand, non-preferred brand, specialty) and whether your deductible has been met.

- Many plans offer lower copayments for generic drugs, sometimes even before the deductible is met.

- Higher-tier or specialty drugs will usually have higher copayments or coinsurance, especially if your deductible has not been satisfied.

Kaiser Permanente’s integrated pharmacy services often mean you can fill prescriptions directly at their medical centers or clinics, which can simplify the process and sometimes offer preferred pricing within their system. Always check your plan’s formulary (list of covered drugs) and cost-sharing schedule for prescription medications.

How to Find and Compare Kaiser Permanente Plans and Costs

Finding the right Kaiser Permanente plan and understanding its true cost involves utilizing specific resources and knowing where to look for accurate information.

Official Kaiser Permanente Website

The most direct and accurate way to get quotes for Kaiser Permanente insurance is through their official website. You can typically input your demographic information (age, location, household size) to receive personalized quotes for available plans in your area. The website will detail the monthly premiums, deductibles, copayments, coinsurance, and out-of-pocket maximums for each plan, along with summaries of benefits. This is an excellent resource for comparing plan tiers (Bronze, Silver, Gold, Platinum) directly.

State and Federal Health Insurance Marketplaces

If you are not offered health insurance through an employer, or if that coverage is deemed unaffordable, you can purchase Kaiser Permanente plans (where available) through your state’s health insurance marketplace (e.g., Covered California, Connect for Health Colorado) or through Healthcare.gov (for states using the federal marketplace).

- These marketplaces are crucial for determining your eligibility for premium tax credits and cost-sharing reductions, which can significantly lower your actual monthly premiums and out-of-pocket expenses.

- The marketplace websites provide a standardized way to compare various plans, including Kaiser Permanente’s, alongside offerings from other insurers, allowing for a side-by-side financial comparison after subsidies are applied.

Employer-Sponsored Plans

For many individuals, the most common way to access Kaiser Permanente insurance is through an employer. If your employer offers Kaiser Permanente as part of their benefits package, these plans are often the most cost-effective. Employers typically contribute a significant portion of the premium, making your out-of-pocket monthly cost substantially lower than if you were to purchase the same plan individually. Consult with your HR department or benefits administrator to understand the specific Kaiser Permanente plans available through your workplace, their costs, and the enrollment process.

Tools for Cost Estimation

Beyond basic quotes, Kaiser Permanente and marketplace websites often provide tools that allow you to estimate your total annual healthcare costs based on anticipated usage. These tools might ask about your general health status, anticipated doctor visits, prescription needs, or potential surgeries. While these are estimates, they can offer a more holistic view of potential annual expenditures beyond just the premium, helping you budget more effectively.

Maximizing Value and Managing Costs with Kaiser Permanente

Choosing Kaiser Permanente is not just about the initial price tag; it’s about making the most of its unique system to manage your health and financial well-being effectively. Understanding how to utilize your benefits wisely can help you maximize value and control your long-term healthcare expenditures.

Utilizing Preventive Care

One of the cornerstones of Kaiser Permanente’s integrated model is its strong emphasis on preventive care. Regular check-ups, screenings, vaccinations, and health education programs are often covered at 100% with no deductible or copay. By actively engaging in preventive care, you can address potential health issues early, often before they become serious and costly. Proactive health management, such as managing chronic conditions through consistent engagement with your care team, can significantly reduce the likelihood of expensive emergency visits or hospitalizations in the future.

Understanding Your Plan Benefits

It might seem obvious, but thoroughly understanding your specific plan’s benefits is paramount. This includes reviewing your Evidence of Coverage (EOC) document, which details what’s covered, what’s excluded, and your cost-sharing responsibilities for various services. Familiarize yourself with the specifics of your deductible, copayments for different types of visits (PCP, specialist, urgent care, emergency room), coinsurance percentages, and your out-of-pocket maximum. Knowing these details upfront will help you avoid financial surprises and make informed decisions about when and where to seek care.

Exploring Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs)

If you enroll in a High Deductible Health Plan (HDHP) offered by Kaiser Permanente (often a Bronze or Silver tier plan), you may be eligible to open a Health Savings Account (HSA). HSAs are tax-advantaged savings accounts that allow you to save money for qualified medical expenses. Contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free. They offer a powerful way to manage out-of-pocket costs while saving for future healthcare needs.

Even if you don’t have an HDHP, many employers offer Flexible Spending Accounts (FSAs) for healthcare. FSAs allow you to set aside pre-tax money from your paycheck to pay for eligible medical, dental, and vision expenses. While FSAs typically have a “use it or lose it” rule (with some carryover exceptions), they can be an excellent way to reduce your taxable income and cover routine medical costs.

Engaging with Your Care Team

Kaiser Permanente’s integrated system thrives on collaboration. By actively engaging with your primary care physician and other members of your care team, you can leverage the system to your advantage. This means communicating openly about your health concerns, participating in shared decision-making regarding your treatment plans, and utilizing the available resources like online portals for scheduling appointments, refilling prescriptions, and communicating with your doctors. A well-coordinated care plan, facilitated by your engagement, can lead to better health outcomes and potentially more cost-effective care pathways.

Conclusion

The question “how much is Kaiser insurance?” requires a multifaceted answer that goes beyond just the monthly premium. It involves understanding Kaiser Permanente’s unique integrated healthcare model, the various factors that influence premiums such as age, location, and plan tier, and the critical role of out-of-pocket expenses like deductibles, copayments, and coinsurance. Financial assistance through subsidies can significantly alter your personal cost, making it imperative to explore all available avenues through health insurance marketplaces or employer-sponsored plans.

Ultimately, the true cost of Kaiser insurance is a balance between your upfront monthly payments and your potential out-of-pocket expenses when accessing care. By thoroughly researching available plans, understanding your benefits, and actively utilizing the preventive care and coordinated services offered, you can not only manage your healthcare finances more effectively but also ensure you’re making the most of your investment in your health. Making an informed decision about Kaiser Permanente means evaluating not just the numbers, but also how well its unique approach aligns with your personal healthcare needs and financial comfort.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.