In the modern financial lexicon, few companies command the awe and sheer scale of Alphabet Inc., the parent company of Google. The question, “how much is Google company worth?” is far more than a simple curiosity; it’s an inquiry into the financial might of one of the world’s most influential technological empires. This valuation is not static; it’s a dynamic reflection of its diverse revenue streams, market dominance, innovation pipeline, and the broader economic landscape. Delving into the financial underpinnings of Alphabet provides a profound insight into the mechanics of trillion-dollar corporations and the complex interplay of technology, market forces, and investor confidence.

Alphabet’s worth is a testament to its pervasive presence across nearly every facet of digital life. From the ubiquitous search engine and the world’s largest video platform (YouTube) to its pioneering efforts in artificial intelligence, cloud computing, and autonomous vehicles, its ventures are deeply embedded in the global economy. Calculating its value involves dissecting its financial statements, understanding its market position, and projecting its future growth potential, all while considering the inherent risks and opportunities that come with operating at such an immense scale. This article will explore the methodologies, revenue drivers, financial health indicators, and future prospects that collectively determine Alphabet Inc.’s gargantuan valuation.

The Many Facets of Valuation: Beyond Simple Market Cap

Determining the “worth” of a company as vast and diversified as Alphabet is a sophisticated process that extends well beyond a glance at its stock price. While market capitalization is often the first figure cited, a comprehensive understanding requires examining various financial metrics and methodologies, each offering a distinct perspective on the company’s financial standing and inherent value.

Market Capitalization: The Public Benchmark

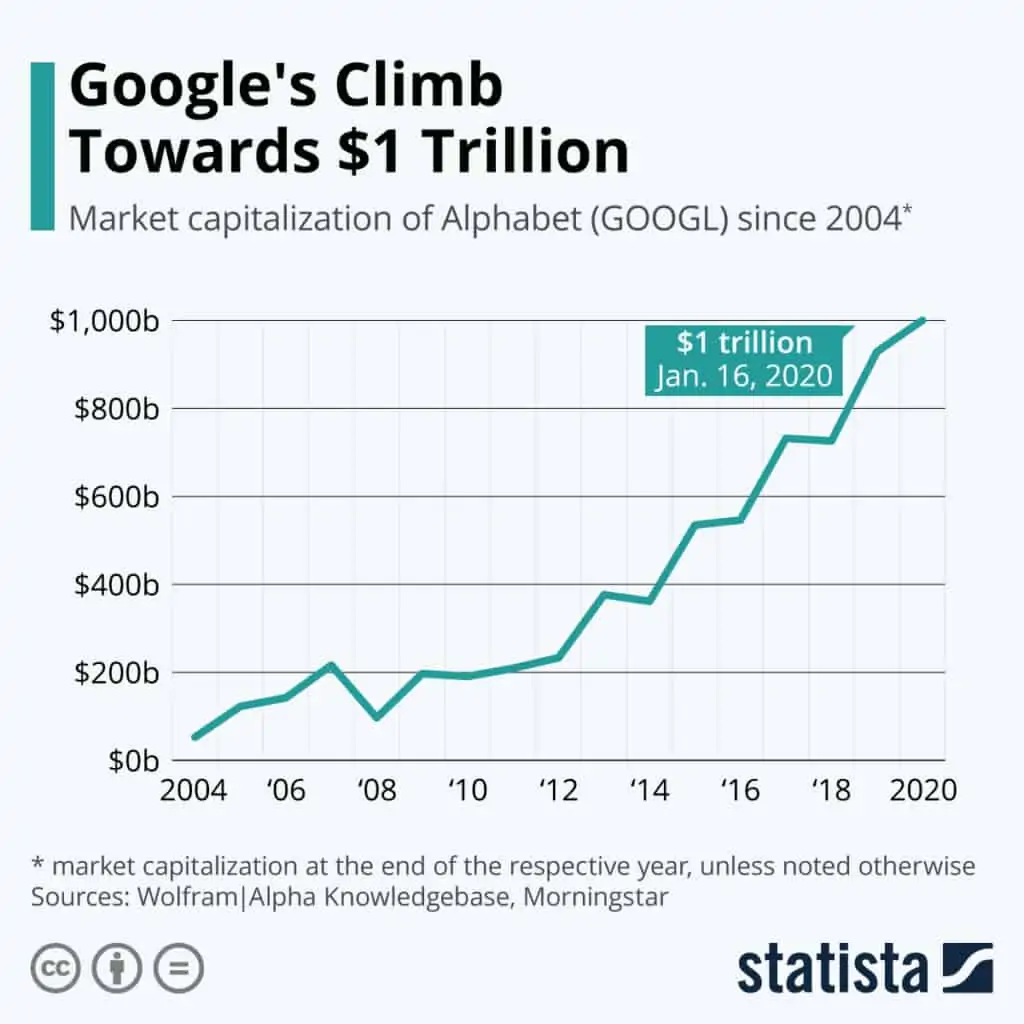

The most common and readily available measure of a company’s worth is its market capitalization. This figure is calculated by multiplying the current share price by the total number of outstanding shares. As a publicly traded entity, Alphabet Inc. (GOOGL and GOOG on NASDAQ) sees its market cap fluctuate daily, even hourly, based on investor sentiment, financial news, economic indicators, and its own operational performance. This metric reflects the collective perception of investors regarding the company’s current value and future prospects. While easy to track, market cap primarily represents equity value and doesn’t fully account for debt or cash reserves, which are crucial for a complete financial picture. Alphabet has historically been a high-growth, high-market-cap stock, often ranking among the top five most valuable companies globally, frequently jostling for position with peers like Apple, Microsoft, Amazon, and Nvidia.

Enterprise Value: A More Comprehensive View

For a more holistic assessment, financial analysts often turn to Enterprise Value (EV). EV provides a more accurate representation of a company’s total value, as if one were to acquire the entire business. It accounts for both equity and debt, while subtracting cash and cash equivalents. The formula is: EV = Market Capitalization + Total Debt – Cash & Cash Equivalents. This metric is particularly useful for comparing companies with different capital structures, as it neutralizes the impact of varying debt levels. For a company like Alphabet, which maintains significant cash reserves and minimal long-term debt relative to its size, its EV might be closer to its market cap, but it offers a more robust foundation for valuation analysis, especially when considering potential mergers and acquisitions or simply understanding the underlying economic value of the business.

Revenue Streams: Fueling the Empire

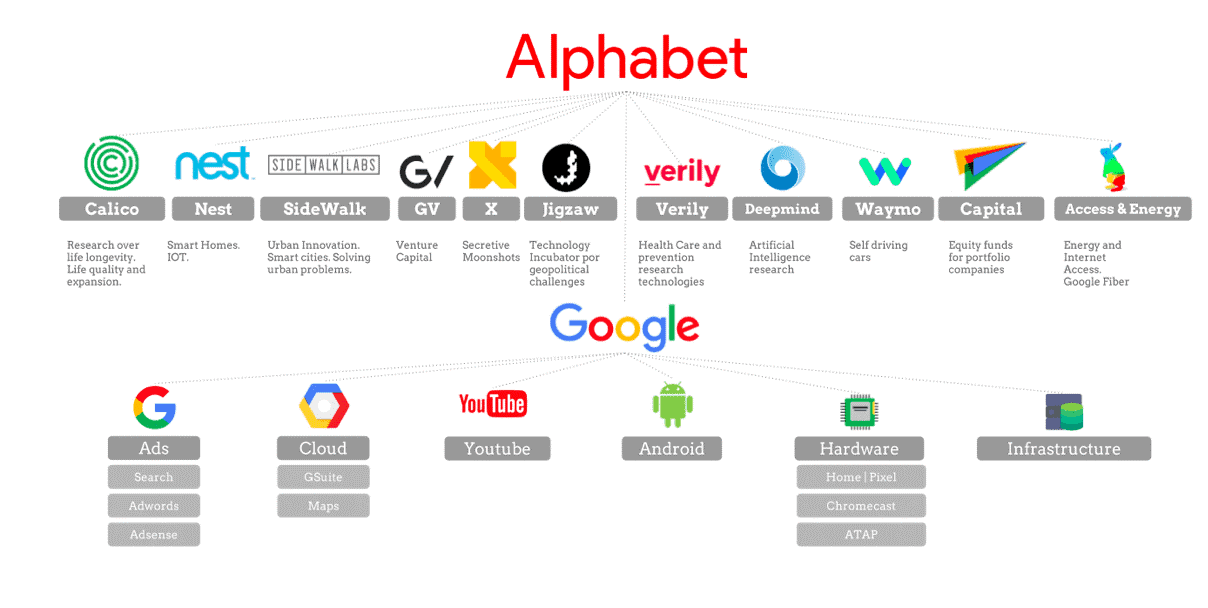

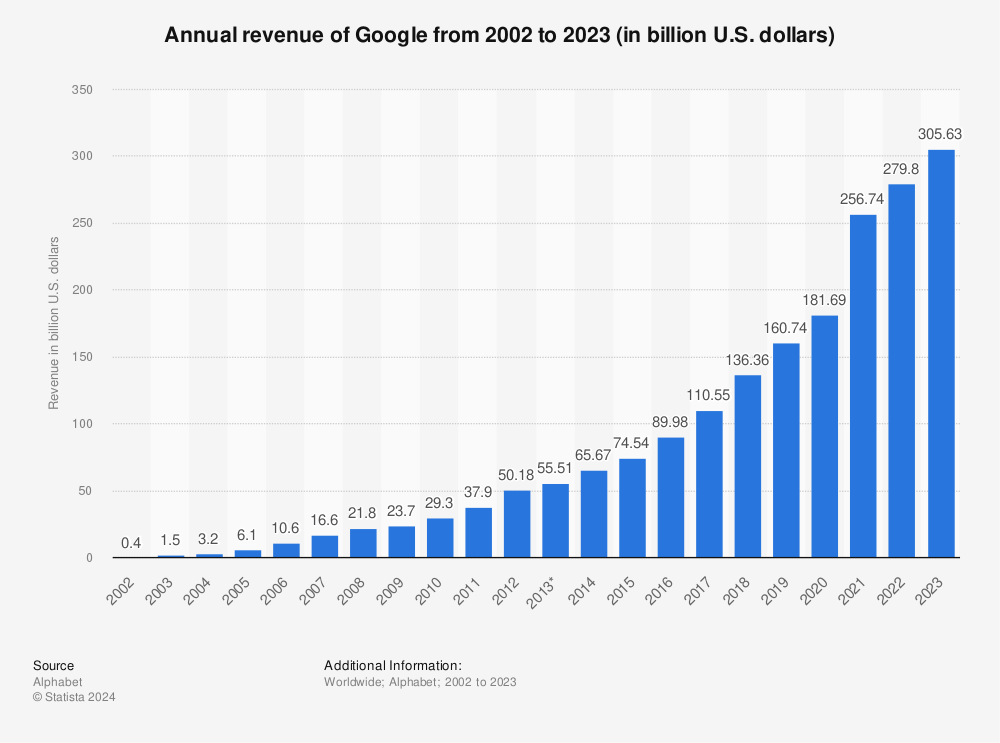

At the heart of any company’s valuation lies its ability to generate revenue. Alphabet’s financial strength stems from a remarkably diverse and robust portfolio of revenue streams, many of which enjoy monopolistic or near-monopolistic positions in their respective markets. The vast majority of its revenue still comes from advertising, primarily through Google Search and YouTube. However, the company has strategically diversified into high-growth areas like cloud computing (Google Cloud), hardware (Pixel phones, Nest devices), and its “Other Bets” segment, which includes moonshot projects in areas like autonomous driving (Waymo) and life sciences (Verily). The consistent growth and profitability across these segments are fundamental drivers of its valuation, reflecting the company’s capacity to innovate and monetize its technological leadership.

Asset Valuation: Tangible and Intangible

Beyond financial statements, a company’s assets contribute significantly to its worth. For Alphabet, these include both tangible assets like real estate, data centers, and physical infrastructure, and, perhaps more importantly, intangible assets. The latter category encompasses its vast intellectual property portfolio (patents, trademarks), brand recognition (the Google brand is one of the most valuable globally), proprietary algorithms, massive user data, and the unparalleled talent pool it employs. The value of Google’s brand alone, its immense global reach, and the network effects of its platforms are incredibly difficult to quantify but represent an enormous, underlying component of its intrinsic worth, often exceeding the sum of its physical parts.

Google’s Dominant Financial Engines: Where the Value Resides

Alphabet’s colossal valuation is primarily built upon a foundation of financially dominant and strategically critical business segments. Understanding where the bulk of its revenue and profit originate is key to appreciating its financial power and investment appeal.

Advertising Powerhouse: Google Search and YouTube

The undisputed cornerstone of Alphabet’s financial success remains its advertising business. Google Search ads, driven by its unparalleled search market share, and YouTube ads, leveraging its position as the world’s largest video platform, collectively generate the vast majority of Alphabet’s revenue and profit. This segment benefits from a powerful flywheel effect: more users lead to more data, which leads to better ad targeting, which attracts more advertisers, which generates more revenue. This cycle is incredibly difficult for competitors to replicate, granting Google a defensible moat. The precision targeting capabilities, extensive reach, and variety of ad formats ensure this segment remains a cash-generating machine, directly contributing to its high valuation.

Cloud Computing Growth: Google Cloud’s Ascent

While advertising is the breadwinner, Google Cloud is the growth engine that excites investors about Alphabet’s future. Competing with Amazon Web Services (AWS) and Microsoft Azure, Google Cloud Platform (GCP) has been rapidly expanding its market share, offering a comprehensive suite of cloud computing services to enterprises worldwide. Although currently contributing a smaller portion of overall revenue compared to advertising, its rapid growth rate, high potential for margin expansion, and strategic importance in the enterprise market make it a significant driver of future valuation. Cloud services represent a sticky, recurring revenue model with immense long-term potential, as businesses increasingly migrate their operations to the cloud.

Other Bets: Investments in Future Value

Alphabet’s “Other Bets” segment encapsulates its innovative, often audacious, ventures beyond its core businesses. This includes Waymo (autonomous driving technology), Verily and Calico (life sciences), Google Fiber (internet services), and various other experimental projects. While many of these “bets” are pre-profitability or still in the research and development phase, they represent Alphabet’s long-term vision and commitment to innovation. Investors view these ventures as potential future revenue drivers, providing upside optionality and demonstrating the company’s capacity for disruptive innovation. A breakthrough in any one of these areas could unlock tremendous new markets and significantly enhance Alphabet’s long-term worth, even if they currently operate at a loss.

Pixel and Hardware: A Niche, but Strategic Contributor

Alphabet also competes in the hardware market with its Pixel smartphones, Nest smart home devices, Fitbit wearables, and other consumer electronics. While not a dominant player in terms of market share compared to Apple or Samsung, the hardware division serves several strategic purposes. It allows Google to showcase the full potential of its Android operating system and AI capabilities, gather valuable user data to refine its software and services, and maintain a presence in the competitive consumer electronics landscape. Though contributing a smaller percentage of overall revenue, this segment is important for ecosystem control and ensuring Google’s software and services have optimal platforms, indirectly supporting the company’s broader value proposition.

Factors Influencing Alphabet’s Valuation Dynamics

The market worth of Alphabet is not static; it’s a dynamic figure constantly influenced by a confluence of internal performance and external market forces. Understanding these factors is critical for anyone looking to comprehend the nuances of its financial trajectory.

Economic Climate and Ad Spending Trends

Given that advertising is Alphabet’s primary revenue source, the broader economic climate plays a monumental role in its valuation. During periods of economic prosperity, businesses tend to increase their advertising budgets, directly boosting Google and YouTube’s revenue. Conversely, economic downturns or recessions often lead to cuts in discretionary ad spending, which can negatively impact Alphabet’s financial performance and subsequently, its stock price and market capitalization. Investor sentiment, which is heavily influenced by macroeconomic indicators like GDP growth, inflation, and consumer spending, directly translates into how the market values Alphabet’s future earnings potential.

Regulatory Scrutiny and Antitrust Concerns

As a dominant player in multiple digital markets, Alphabet consistently faces intense regulatory scrutiny and antitrust challenges from governments worldwide. Concerns over market dominance, data privacy, and competitive practices can lead to investigations, fines, and mandated changes to business operations. For instance, the European Union has historically levied significant fines against Google. These regulatory pressures introduce uncertainty, potential financial penalties, and could force the company to alter its lucrative business models, all of which can weigh on investor confidence and put downward pressure on its valuation. The ongoing legal battles are a constant, albeit manageable, risk factor.

Competitive Landscape and Innovation Pace

While Alphabet enjoys strong competitive moats, it operates in a rapidly evolving technological landscape. Competitors, both established giants and nimble startups, constantly vie for market share in search, cloud, AI, and other emerging fields. For example, the rise of TikTok impacted YouTube’s short-form video strategy, and advancements from OpenAI (backed by Microsoft) challenge Google’s long-standing leadership in AI. Alphabet’s ability to maintain its innovation pace, adapt to new trends, and effectively counter competitive threats is paramount to sustaining its growth and defending its valuation. Any perceived slowdown in innovation or loss of competitive edge can quickly dampen investor enthusiasm.

Investor Sentiment and Market Perception

Beyond objective financial metrics, investor sentiment and market perception significantly influence Alphabet’s valuation. Factors such as positive or negative news cycles, analyst ratings, technological breakthroughs (or setbacks), and even broader market trends (e.g., shifts from growth stocks to value stocks) can sway how investors view the company. A strong narrative around AI leadership, successful diversification into new markets, or effective management of regulatory challenges can bolster confidence, while missteps or negative publicity can erode it. The collective psychology of the market, though seemingly irrational at times, plays a very real role in determining a company’s day-to-day market worth.

Decoding Financial Metrics: A Deep Dive into Alphabet’s Health

To truly understand Alphabet’s financial worth, one must look beyond headline numbers and delve into the specific financial metrics that reveal the underlying health, profitability, and efficiency of the company. These metrics provide a quantitative basis for its valuation.

Revenue Growth and Profitability Margins

Consistent revenue growth is a primary indicator of a healthy, expanding business. Alphabet has historically demonstrated robust top-line growth, largely driven by its core advertising business and increasingly by Google Cloud. Equally important are profitability margins – gross margin, operating margin, and net profit margin. These figures indicate how efficiently the company converts revenue into profit after accounting for costs. Strong and stable margins suggest effective cost management and pricing power, which are crucial for sustaining high valuations. Alphabet typically maintains healthy margins, showcasing its operational efficiency and the inherent profitability of its software-driven services.

Cash Flow Generation and Balance Sheet Strength

Cash is king, and Alphabet is a prolific generator of free cash flow (FCF) – the cash left over after operating expenses and capital expenditures. High FCF indicates a company’s ability to fund its operations, invest in new projects, pay down debt, or return capital to shareholders without needing external financing. Alphabet’s strong FCF generation is a testament to its highly scalable and profitable business model. Furthermore, its balance sheet strength, characterized by substantial cash reserves and relatively low debt, provides immense financial flexibility, resilience against economic shocks, and the capacity to make strategic investments or acquisitions, all of which contribute positively to its valuation.

Shareholder Returns: Dividends and Buybacks (or lack thereof)

For many investors, a company’s commitment to returning capital to shareholders is a key valuation factor. Historically, Alphabet has not paid a regular cash dividend, preferring to reinvest its profits back into the business or execute share buybacks. Share buybacks reduce the number of outstanding shares, thereby increasing earnings per share (EPS) and often boosting the stock price. Alphabet’s substantial share repurchase programs underscore management’s confidence in the company’s intrinsic value and represent a direct way of enhancing shareholder returns. While some investors prefer dividends, Alphabet’s strategy focuses on growth and strategic capital allocation to drive long-term value appreciation.

Price-to-Earnings (P/E) Ratio and Growth Prospects

The Price-to-Earnings (P/E) ratio is a widely used valuation multiple that compares a company’s share price to its earnings per share. It helps investors determine if a stock is undervalued or overvalued relative to its earnings. For a growth company like Alphabet, investors often accept a higher P/E ratio, anticipating future earnings growth that will “catch up” to the current valuation. Analyzing Alphabet’s P/E ratio in context with its earnings growth rate (often using a PEG ratio) provides insights into how the market values its future growth prospects. A consistently strong earnings outlook, fueled by innovation and market expansion, justifies a premium valuation in the eyes of many investors.

The Future Outlook: Sustaining and Growing the Trillion-Dollar Legacy

Alphabet’s journey as a trillion-dollar company is far from over. Its future valuation will depend on its ability to navigate emerging challenges and capitalize on new opportunities, maintaining its leadership in a rapidly evolving technological and economic landscape.

AI Integration and Monetization Opportunities

Artificial intelligence represents the next frontier for Alphabet. With deep expertise and significant investments in AI research and development, the company is poised to integrate advanced AI across all its products and services, from refining search algorithms and enhancing YouTube content creation to powering Google Cloud services and advancing Waymo’s autonomous capabilities. The ability to effectively monetize these AI innovations, whether through improved ad targeting, new AI-powered services, or enhanced enterprise solutions, will be a critical determinant of future revenue growth and, consequently, its valuation. The market will closely watch how Alphabet translates its AI prowess into tangible financial gains.

Expanding Global Reach and Emerging Markets

While Google’s presence is global, significant opportunities remain in expanding its reach, particularly in emerging markets where internet penetration and digital adoption are still growing rapidly. Tailoring its products and services to these markets, respecting local nuances, and effectively competing against local players can unlock vast new user bases and revenue streams. As digital economies mature in regions like Africa, Southeast Asia, and parts of Latin America, Alphabet’s strategic investments and localized offerings will be crucial for sustained international growth, adding billions to its potential addressable market and supporting its long-term valuation trajectory.

Navigating Regulatory Headwinds

The regulatory environment will continue to be a significant factor. Alphabet must skillfully navigate increasing antitrust concerns, data privacy regulations (like GDPR and CCPA), and potential changes to its business practices mandated by governments worldwide. Proactive engagement with regulators, transparent data practices, and demonstrable commitments to fair competition will be essential to mitigate risks and maintain investor confidence. The ability to comply with regulations while preserving its competitive advantages and revenue-generating capabilities will directly impact its future financial stability and valuation.

Strategic Acquisitions and Innovation

Alphabet’s history is punctuated by strategic acquisitions (e.g., Android, YouTube, Fitbit) that have become integral to its ecosystem and financial success. The company’s future growth will likely continue to involve a mix of organic innovation and targeted acquisitions that enhance its technological capabilities, expand its market reach, or neutralize potential threats. Maintaining a culture of relentless innovation, fostering groundbreaking research, and strategically deploying its vast financial resources to acquire promising technologies or talent will be vital for sustaining its competitive edge and driving future valuation growth. The company’s “Other Bets” segment also serves as an internal incubator for future multi-billion-dollar businesses.

Conclusion

The question, “how much is Google company worth?” transcends a simple numerical answer. It leads to a profound exploration of Alphabet Inc.’s multifaceted financial strength, its unparalleled market dominance, and its intricate relationship with global economic and technological trends. Its valuation, consistently in the realm of a trillion dollars or more, is a dynamic tapestry woven from its dominant advertising empire, the explosive growth of Google Cloud, the speculative yet promising “Other Bets,” and the underlying financial health indicated by robust revenue, strong cash flow, and a formidable balance sheet.

As Alphabet continues to innovate at the forefront of AI, expand its global footprint, and navigate an increasingly complex regulatory landscape, its worth will remain a barometer of its adaptability, its strategic foresight, and its enduring capacity to shape the digital future. For investors and financial observers alike, understanding the intricate layers of its valuation provides a critical lens through which to view not just the company itself, but also the broader forces driving the world’s most valuable enterprises.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.