For the modern consumer, the question “How much is a Tesla Model 3?” is rarely answered by a single figure on a window sticker. In the realm of personal finance and strategic investing, the Model 3 represents more than just a vehicle; it is a complex financial asset with a fluctuating price point, significant tax implications, and a unique total cost of ownership (TCO) profile. Since its inception, the Model 3 has been positioned as the “affordable” entry point into the Tesla ecosystem, but understanding its true cost requires a deep dive into federal incentives, operational savings, and the long-term math of electric vehicle (EV) ownership.

This guide analyzes the Tesla Model 3 through a financial lens, breaking down the acquisition costs, financing variables, and the long-term fiscal impact of transitioning from internal combustion to electric propulsion.

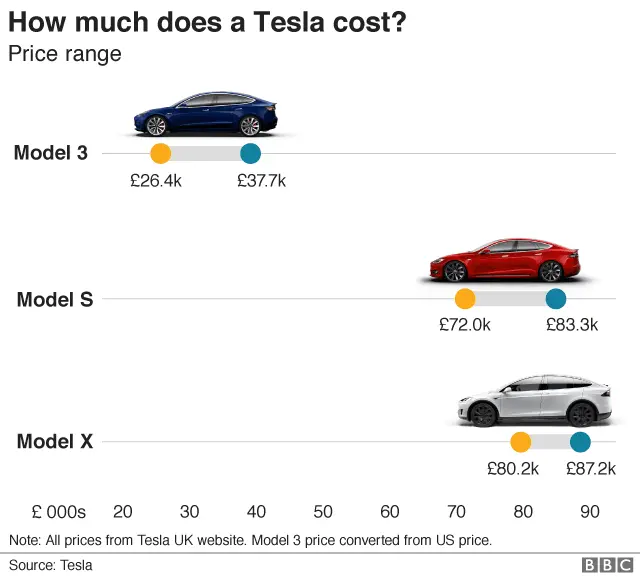

Initial Acquisition Cost: Breaking Down the Sticker Price

The first layer of the financial puzzle is the “out-the-door” price. Tesla utilizes a direct-to-consumer sales model, which eliminates dealership markups but introduces a dynamic pricing strategy where MSRP can change overnight based on market demand and supply chain efficiencies.

Base MSRP and Trim Level Performance

The Tesla Model 3 is currently offered in three primary configurations, each catering to a different budgetary and performance bracket.

- Rear-Wheel Drive (RWD): Often referred to as the “Standard Range,” this is the entry-level tier. It is designed for the budget-conscious buyer who prioritizes the lowest possible entry price.

- Long Range All-Wheel Drive: This mid-tier option represents the “sweet spot” for many investors. While the upfront cost is higher, the increased utility and battery capacity often lead to better value retention.

- Performance: The top-tier trim carries a premium price tag. From a financial perspective, this is a luxury purchase rather than a utility one, as the additional cost goes toward acceleration and aesthetics rather than efficiency.

The Impact of Federal and State Tax Credits

In the United States, the Inflation Reduction Act (IRA) has fundamentally altered the math of buying a Model 3. Under current regulations, eligible buyers can receive a federal tax credit of up to $7,500. For many, this is now available as a “point-of-sale” discount, effectively lowering the loan amount or cash required at the time of purchase. However, this credit is subject to strict income caps and vehicle MSRP limits. For a savvy buyer, navigating these eligibility requirements is the most effective way to reduce the “real” price of the car. Furthermore, various states offer additional rebates, ranging from $500 to $5,000, which can bring the effective cost of a Model 3 RWD down to the level of a mid-market gasoline sedan.

Destination Fees and Hidden Delivery Costs

It is a common financial oversight to ignore the non-negotiable fees. Every new Tesla carries a destination and documentation fee (typically around $1,390). Unlike traditional dealerships where these might be negotiated or waived through various “packages,” Tesla’s fees are fixed. Additionally, buyers must account for registration fees and sales tax, which are calculated based on the pre-incentive price in most jurisdictions, adding thousands to the initial capital outlay.

Financing and Leasing Strategies for the Modern EV

Once the purchase price is established, the next financial hurdle is the method of acquisition. The choice between cash, traditional financing, or leasing can change the long-term wealth impact of the vehicle significantly.

Traditional Loans vs. Tesla Financing

In a high-interest-rate environment, the cost of capital is a major factor. Tesla often partners with various banking institutions to offer competitive rates, but buyers with high credit scores may find better terms at local credit unions. A 1% difference in an interest rate over a 72-month term can result in thousands of dollars in “lost” money. When calculating “how much” a Tesla costs, one must include the total interest paid over the life of the loan.

The Pros and Cons of Leasing a Model 3

Leasing a Tesla Model 3 is an attractive option for those who fear technological obsolescence. Because EV technology (battery density, charging speeds) evolves rapidly, a lease allows a driver to “rent” the technology for three years and hand it back before a major hardware shift occurs. However, from a pure wealth-building perspective, Tesla leases have historically been restrictive—most notably by not allowing lessees to buy out the car at the end of the term. This prevents the driver from capturing any “equity” if the used car market remains strong.

Calculating the Monthly Cash Flow Impact

A professional approach to vehicle budgeting looks at monthly cash flow rather than just the total price. A Model 3 might have a higher monthly payment than a Honda Civic, but when the “fuel” (electricity) and maintenance costs are factored in, the “net” monthly outflow may actually be lower. This “effective monthly cost” is the metric most relevant to personal finance enthusiasts.

Total Cost of Ownership (TCO): Beyond the Purchase Price

The true financial brilliance of the Model 3 lies in its operational efficiency. To understand “how much” the car costs, one must calculate the Total Cost of Ownership over a five-to-ten-year horizon.

Fuel Savings: Electricity vs. Gasoline

The most immediate financial benefit of the Model 3 is the displacement of gasoline costs. On average, charging a Tesla at home costs about one-third as much per mile as fueling a comparable internal combustion engine (ICE) vehicle. For a driver covering 15,000 miles per year, this can result in annual savings of $1,000 to $2,000. Over a five-year ownership period, that is nearly $10,000 returned to the owner’s pocket, effectively acting as a retrospective discount on the purchase price.

Maintenance and Repair Long-Term Projections

Traditional vehicles require oil changes, transmission flushes, spark plug replacements, and brake pad changes (frequently). The Model 3 eliminates most of these. Because of regenerative braking, the physical brakes on a Tesla can last significantly longer than those on a gas car. There are no mufflers, valves, or timing belts to fail. While tires tend to wear out faster on EVs due to the vehicle’s weight and torque, the overall maintenance schedule is remarkably lean, reducing the “surprise” costs that often plague personal budgets.

Insurance Premiums for High-Tech Vehicles

One area where the Model 3 can be more expensive than its peers is insurance. Because of the high cost of the sensors (cameras and ultrasonic sensors) and the specialized labor required for aluminum body repairs, insurance premiums for Teslas are often higher than for traditional sedans. Prospective owners should get an insurance quote before purchasing to ensure these monthly premiums don’t eat into the fuel savings.

Residual Value and Investment Potential

Vehicles are generally depreciating assets, but the rate of depreciation determines the “cost” of the time you spent owning the car.

Depreciation Curves in the EV Market

Historically, Teslas held their value better than almost any other vehicle on the market. However, as production has scaled and Tesla has aggressively cut new car prices, used Model 3 values have normalized. From a financial planning perspective, one should expect a standard depreciation curve of 15-20% in the first year and 10% annually thereafter. Comparing this to the steeper depreciation of luxury German sedans, the Model 3 remains a relatively “safe” place to park capital in the automotive world.

The Software-Defined Value and FSD

A unique variable in the Model 3’s value is Full Self-Driving (FSD) capability. Tesla sells this as a software add-on that can cost upwards of $12,000 (or a monthly subscription). From a money management standpoint, the upfront purchase of FSD is a high-risk investment. While Tesla claims the software will make the car an appreciating asset (via a future “Robotaxi” network), currently, the resale market does not return 100% of the FSD cost to the seller. Most financial advisors suggest the monthly subscription as a way to preserve capital unless the buyer intends to keep the car for its entire operational life.

The 300,000-Mile Horizon

The final financial consideration is the lifespan of the asset. Most modern engines are built to last 150,000 to 200,000 miles. Tesla’s drivetrains are engineered for significantly higher mileage, with battery packs designed to retain the majority of their capacity well beyond the 200,000-mile mark. If a buyer views the Model 3 as a 10-to-15-year investment, the “cost per mile” becomes incredibly low, making it one of the most fiscally responsible choices in the premium automotive segment.

Conclusion: Is the Model 3 a Sound Financial Decision?

When asking “how much is a Tesla Model 3,” the answer is a moving target that depends on your tax bracket, your annual mileage, and your local utility rates. At a base level, the sticker price may hover between $35,000 and $55,000, but the economic price is often much lower.

For the individual focused on personal finance, the Model 3 represents a shift from “Opex” (Operating Expenditure) to “Capex” (Capital Expenditure). You are paying more upfront to drastically reduce your ongoing monthly costs. When the federal incentives are applied and the fuel savings are realized over a five-year period, the Model 3 often competes financially with vehicles that have a sticker price $10,000 to $15,000 lower. In the world of money and investing, the Model 3 isn’t just a car; it’s a calculated hedge against rising energy costs and a lesson in the long-term value of technological efficiency.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.