The allure of a Tesla is undeniable, blending cutting-edge technology, striking design, and the promise of a sustainable future. Yet, for many prospective buyers, the ultimate question isn’t about acceleration or infotainment, but rather: “How much is a Tesla?” This seemingly simple query unravels into a complex web of financial considerations, stretching far beyond the initial sticker price. Understanding the full monetary commitment involves delving into base costs, customization options, financing avenues, and the long-term financial implications of ownership. For anyone contemplating the leap into electric vehicle (EV) ownership, particularly with a brand as prominent as Tesla, a thorough financial analysis is paramount. This guide will navigate the multi-faceted financial landscape of purchasing and owning a Tesla, firmly rooted within the realm of personal finance and investment.

Understanding the Base Price of a Tesla

The journey to determine the cost of a Tesla begins with its base models. Unlike traditional automotive manufacturers with vast lineups, Tesla’s offering is relatively streamlined, though prices fluctuate based on configuration and ongoing market dynamics. It’s crucial to recognize that “a Tesla” isn’t a single price point; it’s a spectrum defined by model, performance, and range.

Model 3: The Entry Point to Tesla Ownership

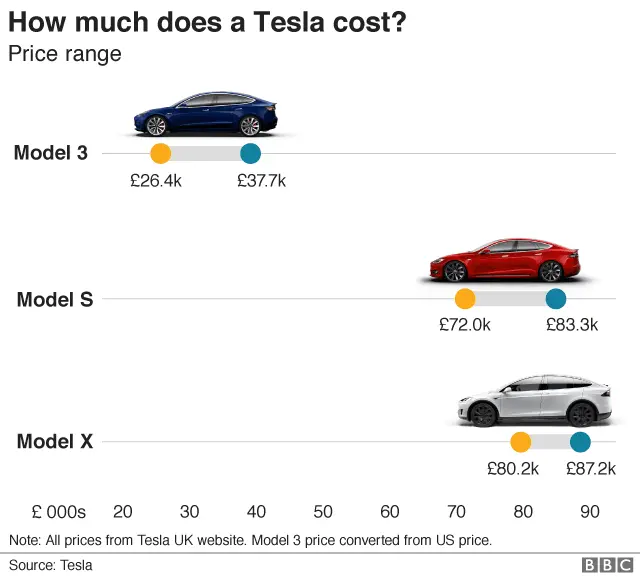

Historically, the Model 3 has served as Tesla’s most accessible vehicle, designed to bring EV technology to a broader market. Its pricing typically starts at a point that makes it competitive with mid-range luxury sedans, yet offers superior technology and electric performance. The base Rear-Wheel Drive (RWD) variant often represents the most affordable option, prioritizing range and efficiency. As one moves up to the Long Range All-Wheel Drive (AWD) or Performance AWD versions, the price naturally increases due to enhanced battery capacity, more powerful motors, and quicker acceleration. For many, the Model 3 strikes an optimal balance between cost, performance, and practicality, making it a popular choice for those transitioning to an EV.

Model Y: The Versatile Crossover SUV

Following the Model 3’s success, the Model Y emerged as a compact crossover SUV, sharing much of its platform and technology with its sedan counterpart. Its appeal lies in its increased cargo space, higher seating position, and optional third-row seating, catering to families or individuals requiring more utility. The Model Y’s entry price is typically higher than the Model 3, reflecting its larger size and versatility. Similar to the Model 3, it’s offered in Long Range AWD and Performance AWD configurations, each carrying a progressively higher price tag. The Model Y often competes with premium compact SUVs, making its financial evaluation critical for buyers weighing practicality against investment.

Model S & Model X: Premium Luxury and Performance

At the apex of Tesla’s consumer lineup sit the Model S sedan and the Model X SUV. These vehicles represent Tesla’s original vision for high-performance, long-range luxury EVs. Their base prices are significantly higher than the Model 3 and Model Y, placing them squarely in the luxury automotive segment. Both models boast exceptional acceleration, extended range, and advanced features, with the Model X uniquely offering “falcon-wing” doors. The Model S and X are often chosen by buyers prioritizing ultimate performance, cutting-edge luxury, and the latest in automotive technology, with their price reflecting their premium positioning and extensive capabilities. The “Plaid” versions of these models push the boundaries of performance and, consequently, price.

Cybertruck and Future Models

Tesla’s innovative spirit extends to future vehicles like the Cybertruck, which, upon its full market release, will introduce new price points and configurations. The Cybertruck’s unique design and utility-focused approach aim to disrupt the truck market, and its pricing is expected to reflect its advanced materials and capabilities. As Tesla continues to innovate and expand its product portfolio, new models will inevitably introduce new base prices, requiring prospective buyers to stay informed about the latest offerings and their financial implications.

Beyond the Sticker Price: Additional Costs and Customizations

The base price is merely the starting point. A true understanding of “how much is a Tesla” necessitates a deep dive into the myriad of options, upgrades, and mandatory fees that can significantly inflate the final purchase price. These elements are crucial for a comprehensive financial assessment.

Autopilot and Full Self-Driving (FSD) Capability

Perhaps the most significant optional upgrade, both financially and technologically, is Tesla’s Autopilot and Full Self-Driving (FSD) capability. While basic Autopilot features (traffic-aware cruise control, autosteer) are typically standard, the enhanced Autopilot and particularly the FSD package are substantial additions. FSD, a sophisticated suite of driver-assistance features aimed at eventual full autonomy, commands a premium price tag, often costing tens of thousands of dollars. Buyers must weigh the financial investment against the current capabilities and future promises of this evolving technology, considering whether the added cost aligns with their personal finance priorities and perceived value.

Paint, Wheels, and Interior Upgrades

Personalization plays a significant role in the final cost. While a standard paint color is included, premium metallic or multi-coat options often incur additional charges. Similarly, upgrading from standard wheels to larger, more aesthetically pleasing designs will add to the price. Interior upgrades, such as premium material choices or specific seat configurations (like the Model Y’s optional third row), also contribute to the final cost. These aesthetic and comfort enhancements, while appealing, are non-essential from a functional standpoint and represent discretionary spending that can quickly accumulate.

Destination, Documentation, and Order Fees

Every new vehicle purchase includes mandatory fees that are separate from the vehicle’s MSRP. A destination fee, also known as a delivery fee, covers the cost of shipping the vehicle from the factory to the delivery center. This fee is standard across all models and is non-negotiable. Documentation fees, often charged by dealerships or directly by manufacturers in states where they operate directly, cover the administrative costs of processing paperwork. Finally, an order fee is often required when placing a reservation for a Tesla, which may or may not be applied toward the final purchase price depending on the market and specific terms. These fees, though seemingly small individually, add to the total financial outlay.

Sales Tax, Registration, and Other Government Fees

The final and often largest add-on to the purchase price comes in the form of sales tax. This percentage-based tax, which varies significantly by state and locality, is applied to the total purchase price of the vehicle, including any options and fees. Given Tesla’s price points, the sales tax alone can amount to thousands of dollars. Beyond sales tax, buyers are responsible for annual vehicle registration fees, license plate fees, and potentially other local government charges. These recurring and upfront governmental fees are critical components of the total cost and must be factored into any financial planning for a Tesla purchase.

Financing Your Tesla: Options and Considerations

Once the total “out-the-door” price is established, the next financial hurdle is determining how to pay for it. Tesla offers several avenues for acquisition, each with its own financial implications for personal finance and cash flow.

Cash Purchase vs. Loan vs. Lease

- Cash Purchase: For those with sufficient liquid assets, paying cash for a Tesla eliminates interest payments and the burden of monthly debt. This provides complete ownership from day one and simplifies financial planning. However, it ties up a significant amount of capital that could potentially be invested elsewhere, making the opportunity cost a key financial consideration.

- Traditional Auto Loan: The most common financing method, an auto loan allows buyers to spread the cost over several years (e.g., 36 to 72 months). This preserves capital and makes the vehicle accessible to a wider range of budgets. Key financial considerations include the interest rate (APR), loan term, down payment amount, and the impact on one’s credit score. Securing a favorable interest rate is crucial for minimizing the total cost of borrowing.

- Leasing: Leasing a Tesla involves paying for the depreciation of the vehicle over a set period (typically 2-4 years) rather than purchasing it outright. Monthly lease payments are generally lower than loan payments, and maintenance is often covered under warranty for the lease term. This option is appealing for those who prefer to drive a new car every few years and aren’t concerned with long-term ownership. However, lessees do not build equity, face mileage restrictions, and may incur fees for excessive wear and tear. Financially, leasing is a consumption model, not an asset acquisition strategy.

Interest Rates and Loan Terms

For those choosing a loan, interest rates are paramount. Rates are influenced by general economic conditions, the lender’s policies, and the borrower’s creditworthiness. A difference of even a percentage point can amount to thousands of dollars over the life of a loan. Shorter loan terms (e.g., 36 or 48 months) typically come with higher monthly payments but lower total interest paid, while longer terms (e.g., 60 or 72 months) reduce monthly payments but increase total interest. Careful consideration of one’s budget and long-term financial goals is essential when selecting a loan term.

Eligibility and Credit Score Impact

Lenders assess a borrower’s credit score, debt-to-income ratio, and income stability to determine loan eligibility and interest rates. A strong credit score (generally 700+) is vital for securing the most favorable terms. Taking on a significant auto loan will also impact one’s credit utilization and overall debt burden, which can affect future borrowing capacity for things like mortgages or personal loans. Prospective buyers should review their credit report and understand their financial standing before applying for a Tesla loan.

Leasing: Pros and Cons for Financial Planning

Leasing offers predictable monthly payments and the ability to drive a new Tesla every few years. It avoids the complexities of resale value and major repair costs post-warranty. However, from a financial perspective, leasing means you never own an asset. Your payments build no equity, and at the end of the term, you either return the car or buy it out at a pre-determined residual value. This can be less financially efficient for those who plan to keep a vehicle for many years. It’s a trade-off between flexibility and long-term asset building, critical for sound personal finance decisions.

The Long-Term Financial Picture: Ownership Costs and Value

The purchase price and financing are only one part of the financial equation. True cost of ownership extends years into the future, encompassing recurring expenses and considering the vehicle’s long-term value.

Charging Costs vs. Fuel Costs

One of the most compelling financial arguments for an EV is the reduced “fuel” cost. While electricity prices vary, charging a Tesla at home or at public Superchargers is generally cheaper per mile than gasoline, especially for premium fuel. Owners can often optimize costs by charging during off-peak hours at home or utilizing free charging options where available. However, relying solely on Superchargers can sometimes approach or even exceed gasoline costs, depending on local electricity rates. A detailed comparison of typical driving habits and local energy costs is crucial for accurate financial forecasting.

Insurance Premiums for a Tesla

Tesla vehicles, being high-tech, performance-oriented, and often targets for theft, generally command higher insurance premiums than comparable internal combustion engine (ICE) vehicles. The cost of replacing specialized components, extensive software, and the higher purchase price all contribute to this. Factors like the driver’s record, location, chosen coverage, and model variant will influence the exact premium. It’s imperative to obtain insurance quotes before purchasing a Tesla to avoid any unpleasant financial surprises.

Maintenance and Repairs

EVs are known for having fewer moving parts than ICE vehicles, leading to potentially lower routine maintenance costs. There’s no oil to change, spark plugs to replace, or complex transmissions to service. However, Teslas still require tire rotations, brake fluid checks, cabin filter replacements, and occasional wear-and-tear repairs. Battery degradation, while often covered by long warranties, is a long-term factor. Software updates often address issues, but unexpected repairs to high-tech components can be expensive outside of warranty. Owners should budget for these items and consider extended warranty options, if available, as a risk management strategy.

Depreciation and Resale Value

Like all vehicles, Teslas depreciate, though historically they have held their value better than many luxury ICE cars, partly due to demand, brand appeal, and continuous software updates that keep older models feeling fresh. However, rapid technological advancements and new model releases can impact future depreciation curves. The resale value will depend on factors like mileage, condition, optional features (like FSD, which may or may not retain its full value), and market demand at the time of sale. Considering the potential depreciation is vital for calculating the true total cost of ownership over time and making a sound financial decision.

Government Incentives and Tax Credits

Both federal and state governments have historically offered incentives to encourage EV adoption. These can include federal tax credits, state rebates, sales tax exemptions, or even preferential parking/HOV lane access. These incentives can significantly reduce the effective purchase price of a Tesla, sometimes by thousands of dollars. However, eligibility rules frequently change, often based on the vehicle’s manufacturing location, battery components, and the buyer’s income level. Prospective buyers must thoroughly research current incentives applicable to their specific situation and location, as these can materially impact the financial viability of a Tesla purchase.

Is a Tesla a Worthwhile Financial Investment?

Ultimately, the decision of whether a Tesla is “worth it” financially is deeply personal, rooted in individual financial goals, priorities, and lifestyle. It’s rarely a pure financial “investment” in the traditional sense, as cars are depreciating assets. However, it can be a financially wise purchase under the right circumstances.

Evaluating Total Cost of Ownership (TCO)

To truly answer “how much is a Tesla,” one must calculate the Total Cost of Ownership (TCO) over a planned period, typically 3-5 years. This involves summing up the initial purchase price (adjusted for incentives), financing costs, insurance, charging, maintenance, and then subtracting the estimated resale value. Comparing the TCO of a Tesla against a comparable ICE vehicle, or even other EVs, provides the clearest financial picture. Often, the lower operating costs of an EV can offset a higher upfront price over the long term, though this requires careful calculation.

Environmental Impact and Savings

Beyond pure financial metrics, many Tesla buyers consider the environmental benefits. Reduced carbon footprint and reliance on fossil fuels are significant motivations. While not directly financial, the societal value and personal satisfaction derived from contributing to sustainability can be considered a form of “return” on investment for some. There’s also the potential for long-term savings on fuel if gasoline prices remain volatile or trend upwards.

Future Value Proposition

Tesla’s continuous innovation, over-the-air software updates, and strong brand identity suggest that their vehicles may continue to hold value relatively well compared to the broader market. The ongoing development of features like FSD could, theoretically, enhance the long-term utility and desirability of older models. However, this future value is not guaranteed and depends on market trends, technological obsolescence, and brand perception.

Making an Informed Financial Decision

Purchasing a Tesla is a significant financial commitment. It requires meticulous budgeting, an understanding of all associated costs, and a clear view of one’s long-term financial health. Prospective buyers should explore all financing options, research current incentives, and carefully consider their driving habits and personal circumstances. While the initial “how much is a Tesla” might seem daunting, a comprehensive financial guide empowers individuals to make an informed, confident, and financially sound decision that aligns with their personal finance objectives.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.