In the modern digital economy, the speed of capital movement has become as critical as the capital itself. Venmo, a subsidiary of PayPal, has revolutionized the way we handle peer-to-peer (P2P) transactions, turning the act of paying someone back into a social experience. However, for many users, the most pressing question isn’t how to send money, but how to get that money out of the app and into a traditional bank account. While Venmo offers a free “Standard” transfer, the “Instant Transfer” feature is the go-to for those in need of immediate liquidity. Understanding the costs associated with this speed is essential for effective personal finance management.

Understanding the Cost of Convenience: Venmo’s Fee Structure

The primary draw of Venmo is its seamless interface, but that seamlessness comes with a specific price tag when you bypass the traditional banking wait times. To manage your money effectively, you must understand exactly how Venmo calculates its take on your hard-earned cash.

The Standard Transfer vs. Instant Transfer

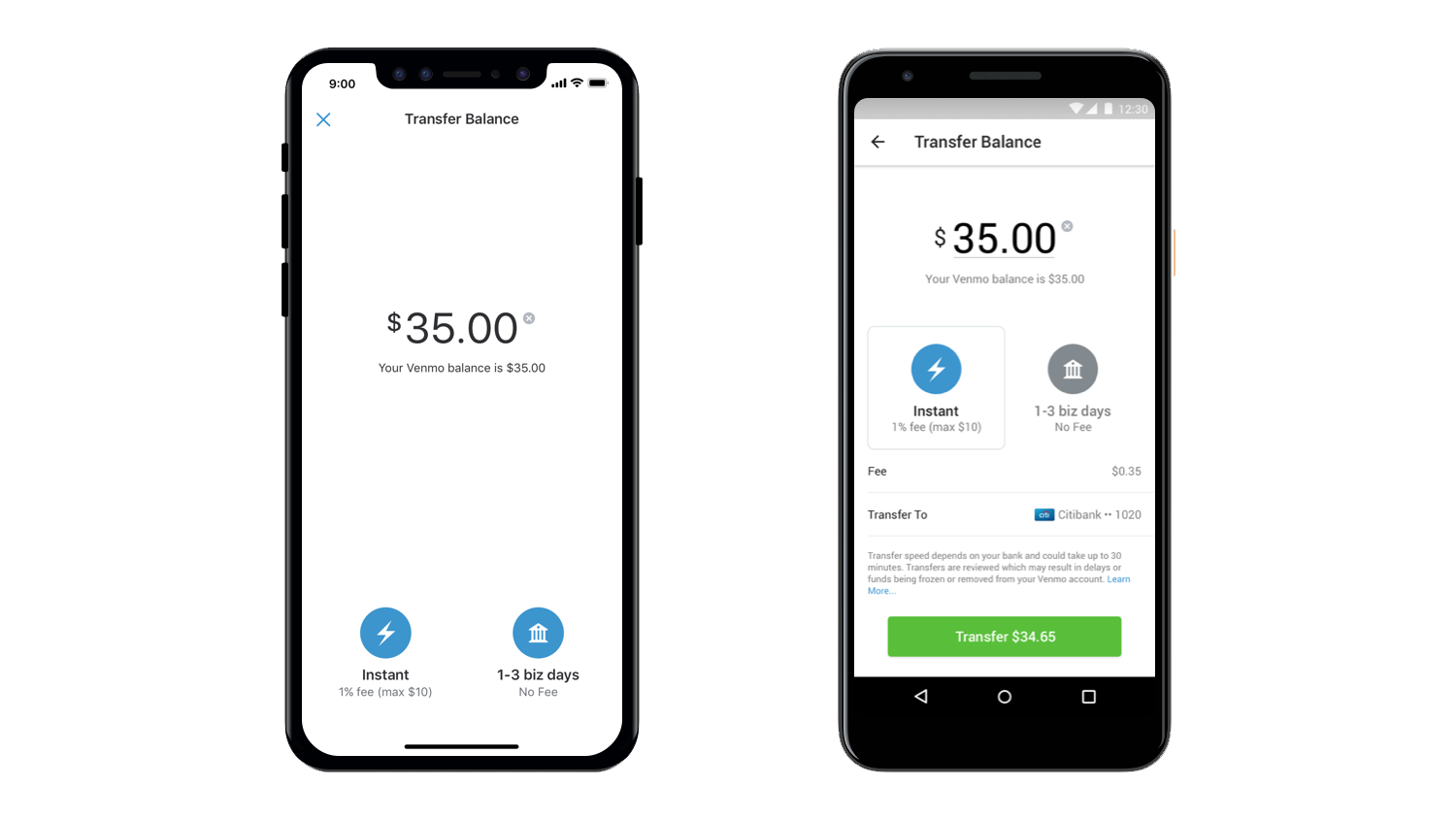

When you receive money on Venmo, it sits in your “Venmo Balance.” You have two primary ways to move that money to your personal bank account. The Standard Transfer is free of charge but typically takes one to three business days to settle. This delay is due to the Automated Clearing House (ACH) network, which processes transactions in batches.

The Instant Transfer, conversely, utilizes the Real-Time Payments (RTP) network or push-to-card technology. This allows funds to arrive in your bank account or on your debit card within minutes—usually less than 30. This speed is a premium service, and Venmo charges accordingly to facilitate this rapid movement of data and value.

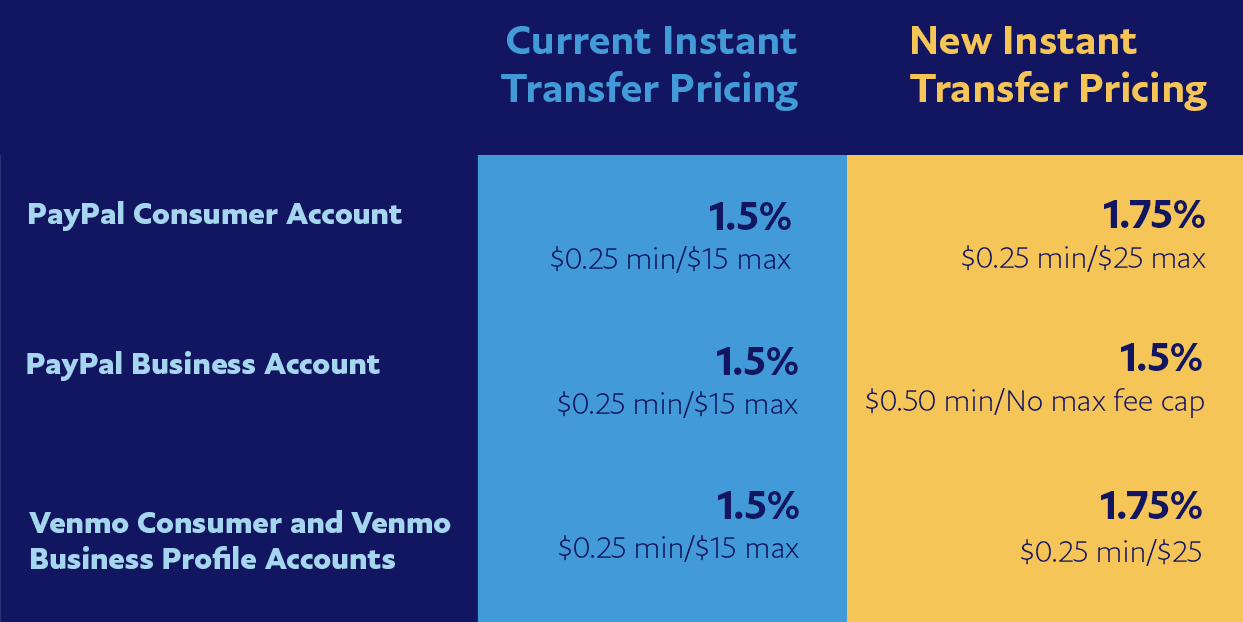

Current Percentage-Based Fees and Limits

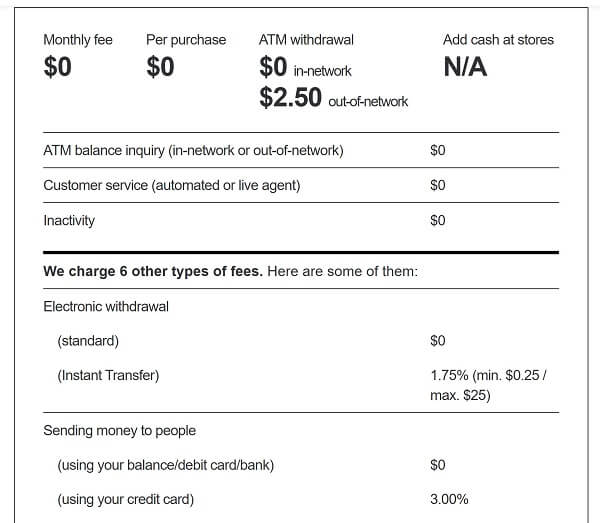

As of the latest updates to Venmo’s terms of service, the fee for an Instant Transfer is 1.75% of the total transfer amount. While 1.75% might sound negligible on a $20 lunch repayment, it scales significantly with larger sums.

To protect users and the platform, Venmo imposes a “floor” and a “ceiling” on these fees:

- Minimum Fee: $0.25. If you are transferring a small amount where 1.75% would be less than a quarter, Venmo will still charge you $0.25.

- Maximum Fee: $25.00. This is the cap. If you are transferring several thousand dollars, your fee will never exceed $25, making larger transfers slightly more “cost-effective” in terms of percentage.

For example, if you transfer $100, the fee is $1.75. If you transfer $10, the fee is $0.25 (since 1.75% of $10 is only $0.17). If you transfer $2,000, the fee is $25 (since 1.75% of $2,000 would be $35, but the cap kicks in).

The Mechanics of Liquidity: Why Instant Transfers Matter

In the world of personal finance, liquidity is king. The ability to access your cash immediately can be the difference between paying a bill on time or incurring a late fee that far exceeds Venmo’s 1.75% charge.

Emergency Funds and Cash Flow Management

For freelancers, gig workers, and those living paycheck to paycheck, Venmo often acts as a primary receiving account for income. When an unexpected expense arises—such as a car repair or a medical co-pay—the one-to-three-day wait of a standard transfer is often not an option.

In these scenarios, the Instant Transfer fee is viewed not just as a cost, but as a “convenience tax” that provides financial agility. From a strategic standpoint, paying $1.75 to access $100 instantly is a rational financial decision if it prevents a $35 overdraft fee or a $50 late payment penalty on a utility bill. However, relying on this feature habitually can erode your savings over time, making it a tool that should be used with intention rather than by default.

Comparing Venmo to Other Peer-to-Peer (P2P) Payment Tools

To truly understand Venmo’s value proposition, one must look at the broader financial tool landscape. Venmo’s 1.75% fee is competitive but not the only option:

- Cash App: Typically charges a similar fee (ranging from 0.5% to 1.75%) for instant deposits.

- Zelle: Often integrated directly into banking apps, Zelle usually offers instant transfers for free, as it moves money directly between linked bank accounts without an intermediary “balance” phase.

- PayPal: As Venmo’s parent company, PayPal utilizes a near-identical fee structure for its instant transfer service to debit cards and bank accounts.

By comparing these tools, users can decide which “wallet” to use for specific transactions. If a friend offers to pay you via Zelle or Venmo, choosing Zelle might save you the 1.75% fee if you know you’ll need that money in your bank account immediately.

Security and Eligibility for Instant Transfers

Not every transaction or bank account is eligible for the instant transfer feature. There are technical and security hurdles that Venmo implements to ensure the integrity of the financial system.

Verifying Your Bank and Card Compatibility

To use Instant Transfer, you must have a valid U.S. debit card or a bank account that supports the “Instant Transfer” network. Most major banks (like Chase, Wells Fargo, and Bank of America) participate in these networks. However, some smaller credit unions or prepaid cards may not support the necessary technology.

Users should also be aware that Venmo requires account verification to move larger sums of money. This involves confirming your identity through your Social Security Number (SSN) or other legal documentation. Without this verification, your transfer limits—both for sending and for withdrawing—will be significantly lower, which can hamper your ability to move money during a financial crunch.

Protecting Your Transactions in a High-Speed Environment

Speed is a double-edged sword. While it’s great to get your money quickly, the “instant” nature of these transfers means they are generally irreversible. Venmo uses encryption and monitoring to flag suspicious activity, but the onus of security often falls on the user.

Before hitting the “Transfer” button, always double-check the destination. If you have multiple bank accounts or debit cards linked, ensuring the money is going to the correct institution is vital. Once the “Instant Transfer” is initiated and the fee is deducted, there is no “undo” button. From a financial security perspective, it is also wise to enable two-factor authentication (2FA) on your Venmo account to ensure that a bad actor cannot instantly drain your Venmo balance into an external account.

Strategic Alternatives to Paying the Instant Transfer Fee

For the budget-conscious user, avoiding unnecessary fees is a cornerstone of building wealth. While 1.75% seems small, frequent users can end up paying hundreds of dollars a year in transfer fees.

Leveraging the Venmo Debit Card

One of the most effective ways to bypass the instant transfer fee while still maintaining immediate access to your funds is the Venmo Debit Card. This is a physical Mastercard that is linked directly to your Venmo balance.

By using the card, you can spend your Venmo balance at any retailer that accepts Mastercard, or withdraw cash at an ATM, without ever having to “transfer” the money to a traditional bank. This allows you to treat your Venmo balance as a checking account. If you need the money for groceries or gas, using the Venmo card costs you $0 in fees, whereas transferring that money to your bank account to use your bank’s debit card would cost you the 1.75% fee.

Planning Ahead with Standard Bank Transfers

The most straightforward way to save money is through behavioral change: planning. If you know you have a rent payment due on the 1st of the month, initiating a free Standard Transfer on the 25th of the previous month ensures the funds are there without the need for an Instant Transfer.

In professional personal finance management, “the cost of waiting” is a variable you can control. By maintaining a small buffer in your traditional bank account, you can afford the three-day lead time required for free transfers. This strategy effectively turns Venmo into a secondary “holding pen” for capital rather than an emergency pipeline, ensuring that every cent you earn or receive stays in your pocket rather than going toward platform service fees.

Summary of Best Practices

To maximize the utility of Venmo while minimizing the financial impact, consider the following rules of thumb:

- Use Instant Transfer for true emergencies only, where the cost of the fee is lower than the cost of a potential late penalty.

- Verify your identity to unlock higher transfer limits and ensure your account remains in good standing.

- Get the Venmo Debit Card to spend your balance directly, effectively circumventing the need for transfers altogether.

- Compare P2P apps before requesting money; if you have the option, Zelle is often the most cost-effective for instant liquidity.

By treating Venmo as a strategic financial tool rather than just a social app, you can enjoy the convenience of modern fintech without sacrificing your long-term financial health to avoidable fees.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.