The allure of a Tesla – cutting-edge technology, exhilarating performance, and a commitment to sustainable transport – often captivates prospective buyers. However, behind the sleek design and impressive specifications lies a critical question for anyone considering the switch: “How much does a Tesla car cost?” This seemingly straightforward inquiry quickly unravels into a complex financial exploration, far exceeding a simple sticker price. For the financially savvy individual, understanding the true cost of Tesla ownership involves a deep dive into initial outlay, ongoing operational expenses, long-term value retention, and strategic financial planning. This article will meticulously dissect these monetary facets, providing a comprehensive financial guide to owning a Tesla, firmly rooted within the domain of personal and business finance.

Beyond the Sticker Price: Understanding Tesla’s Initial Investment

The journey to Tesla ownership begins with the initial purchase price, but this figure is merely the tip of the iceberg. Savvy financial planning necessitates a detailed breakdown of what contributes to this foundational cost and how various factors can either escalate or mitigate it.

Model-Specific Pricing: A Snapshot of Current Tesla Offerings

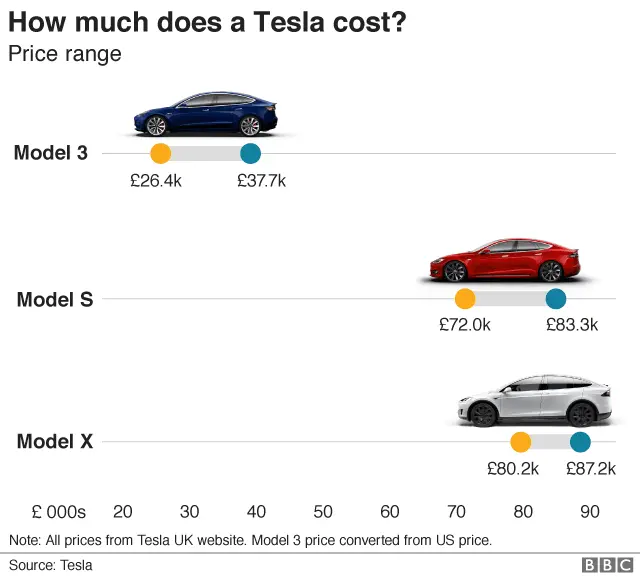

Tesla offers a range of models, each catering to different needs and budgets, and their starting prices form the bedrock of the initial investment. As of current market conditions (and acknowledging that prices can fluctuate), Tesla’s lineup generally includes the more accessible Model 3 sedan and Model Y SUV, which typically serve as entry points into the brand. The Model 3, for instance, might start in the mid-$30,000s to low-$40,000s for its base Rear-Wheel Drive variant, with Long Range and Performance versions commanding higher prices. Similarly, the Model Y, being an SUV, usually begins in the high-$40,000s to low-$50,000s, escalating significantly for its Long Range and Performance trims.

At the upper echelon, the Model S sedan and Model X SUV represent Tesla’s premium offerings. These vehicles boast longer ranges, more luxurious interiors, and advanced features, with starting prices often well into the $70,000s, and top-tier Plaid versions easily exceeding $100,000. For business owners or those seeking to electrify a fleet, understanding this diverse pricing structure is crucial for initial budget allocation and determining the financial viability of integrating Teslas into operations. These base prices are critical for calculating down payments, loan amounts, and ultimately, the total principal investment.

Customizable Add-Ons and Their Financial Impact

One of the most significant factors influencing a Tesla’s final purchase price is the array of customizable add-ons. While some are aesthetic, many enhance functionality and performance, each carrying a substantial financial implication. The most prominent example is the “Full Self-Driving” (FSD) capability. This advanced driver-assistance system, while continuously evolving, represents a considerable upfront investment, often costing upward of $10,000 to $15,000 or more if purchased outright. Alternatively, Tesla offers an FSD subscription, converting a large capital outlay into a recurring monthly operating expense, which impacts cash flow differently.

Beyond FSD, choices like premium paint colors (e.g., Red Multi-Coat), larger wheel upgrades, and interior material selections (e.g., white interior) add several hundreds or thousands of dollars to the final cost. These customizations, while enhancing the ownership experience, directly inflate the initial capital expenditure. For individuals or businesses meticulously managing their budgets, each add-on needs to be weighed against its perceived value and its financial impact on the overall investment, potentially pushing a “budget-friendly” Model 3 into the price territory of a base Model Y.

Navigating Government Incentives and Tax Credits

A pivotal aspect of reducing the effective purchase price of a Tesla, and indeed any electric vehicle, is leveraging available government incentives and tax credits. These financial mechanisms are designed to accelerate EV adoption and can significantly lower the overall cost of ownership. The most widely known is the federal EV tax credit in the United States, which, depending on battery capacity, manufacturing location, and critical mineral sourcing, can offer up to $7,500. However, eligibility criteria are strict, often tied to the manufacturer’s suggested retail price (MSRP) of the vehicle and the buyer’s adjusted gross income. Therefore, not all Tesla models or buyers will qualify for the full amount, or any amount, at a given time.

Beyond federal incentives, many states and even some local municipalities offer additional rebates, grants, or tax credits. These can range from a few hundred dollars for home charging equipment installation to several thousand dollars off the purchase price of the EV itself. For instance, some states might offer an additional $2,000-$5,000 rebate. Business finance departments should also explore specific commercial incentives for fleet electrification. Thorough research into these programs – understanding their caps, eligibility requirements, and application processes – is absolutely essential for maximizing financial savings and accurately calculating the net initial investment in a Tesla. Failing to account for these can lead to an overestimation of the car’s true cost, or conversely, missing out on valuable savings.

The Long-Term Financial Picture: Operating Costs and Savings

While the initial purchase price is a significant hurdle, the ongoing operational costs and potential savings over the vehicle’s lifespan paint a more complete financial picture. This “total cost of ownership” (TCO) perspective is critical for any long-term financial planning.

Fueling Your Tesla: Electricity Costs vs. Gasoline Savings

One of the most compelling financial advantages of a Tesla is the dramatic reduction in “fuel” costs. Replacing gasoline with electricity fundamentally alters the monthly budget. While gasoline prices fluctuate wildly, electricity costs are generally more stable and, crucially, significantly lower per mile traveled.

The cost of charging a Tesla varies based on several factors:

- Home Charging: This is typically the most cost-effective method. Charging overnight during off-peak hours, when electricity rates are lowest, can result in per-mile costs equivalent to paying under $1.00 per gallon of gasoline in many regions. Installing a Level 2 charger at home (a one-time investment often offset by rebates) optimizes this saving.

- Tesla Supercharger Network: For long-distance travel or when home charging isn’t feasible, the Supercharger network offers rapid charging. While more expensive than home charging, Supercharger rates are still generally competitive with, or cheaper than, gasoline for an equivalent range. Rates can vary by location and time of day, often ranging from $0.25 to $0.50 per kWh.

- Third-Party Charging Networks: Other public charging options exist, with varying pricing models (per kWh, per minute, or session fees).

From a financial planning standpoint, the consistent savings on fuel can be substantial, often amounting to hundreds or even over a thousand dollars annually, depending on mileage and local energy costs. For businesses with fleets, these savings accumulate rapidly, directly impacting the bottom line. Calculating the potential savings requires comparing average gasoline consumption and price for a conventional vehicle against the Tesla’s electricity consumption (measured in Wh/mile or kWh/100 miles) and local electricity rates.

Maintenance and Service: A Different Paradigm

Tesla ownership introduces a paradigm shift in automotive maintenance, largely due to the simplicity of electric powertrains. Internal combustion engine (ICE) vehicles require regular oil changes, spark plug replacements, air filter changes, and more frequent brake service. Teslas, by contrast, have far fewer moving parts. There’s no engine oil to change, no timing belt to replace, and regenerative braking significantly reduces wear on brake pads and rotors, extending their lifespan considerably.

However, “lower maintenance” doesn’t mean “no maintenance.” Tesla owners still incur costs for:

- Tires: Due to the instant torque and heavier weight of EVs, tire wear can sometimes be higher than in equivalent ICE vehicles, necessitating more frequent replacements.

- Wiper Blades and Cabin Air Filters: These are routine consumables.

- Annual Inspections: While less critical than ICE vehicle services, Tesla recommends specific checks and services at certain mileage or time intervals (e.g., brake fluid checks, tire rotations, battery system diagnostics).

- Body Repairs: As with any car, accident repairs can be costly, and specialized EV components might require specific repair expertise, potentially affecting insurance premiums.

From a financial perspective, Tesla owners often report significant savings on routine maintenance compared to their previous gasoline cars. These savings contribute directly to a lower total cost of ownership over the vehicle’s lifespan, freeing up budget for other personal finance goals or business investments.

Insurance Premiums: An Often Overlooked Expense

While often overlooked during the initial purchase excitement, insurance premiums represent a significant ongoing financial commitment for any vehicle, and Teslas are no exception. In fact, many Tesla owners find their insurance costs to be higher than those for comparable gasoline-powered cars. Several factors contribute to this:

- High Replacement Cost: Teslas, especially the performance models, have higher MSRPs, meaning the cost to replace the vehicle in case of a total loss is higher for insurers.

- Specialized Parts and Repair: The advanced technology, specialized components, and aluminum body construction of Teslas can lead to higher repair costs following an accident. Not all body shops are certified to repair Teslas, limiting competition and potentially increasing prices.

- Performance: Many Teslas offer instant torque and rapid acceleration, which insurers may perceive as a higher risk factor for accidents, particularly for younger drivers.

- Technology Features: While features like FSD or advanced collision avoidance systems aim to reduce accidents, their complexity means repairs to these systems can be expensive if damaged.

Prospective buyers should always obtain insurance quotes for their desired Tesla model before committing to a purchase. The difference in premiums can be substantial based on the model, driver’s history, location, and chosen coverage limits. For robust financial planning, factoring in these potentially higher insurance costs is crucial for an accurate monthly and annual budget. Some owners explore Tesla’s own insurance offerings, which use real-time driving data to adjust premiums, potentially rewarding safer drivers with lower costs, though this approach has its own privacy considerations.

Depreciation, Resale Value, and Future Financial Outlook

Beyond the immediate and ongoing costs, the long-term financial health of owning a Tesla hinges significantly on how it retains value over time, its status as an asset, and the various financing mechanisms available.

Understanding Tesla’s Depreciation Trends

Depreciation is a critical, albeit often silent, financial cost of vehicle ownership. It represents the loss in value of an asset over time due to wear and tear, age, and obsolescence. For electric vehicles, including Teslas, depreciation patterns can differ from traditional ICE vehicles.

Historically, Teslas have demonstrated relatively strong resale values compared to many conventional luxury cars. Factors contributing to this include:

- High Demand: The strong market demand for Teslas, driven by brand appeal and EV adoption, helps to prop up used prices.

- Over-the-Air (OTA) Updates: Unlike ICE vehicles that become technologically static after purchase, Teslas receive software updates that can add new features, improve performance, and enhance battery management, effectively “upgrading” the car over its lifespan and mitigating technological obsolescence to some degree.

- Battery Longevity: Modern EV batteries are proving to be very durable, alleviating earlier concerns about rapid battery degradation impacting resale value.

However, factors that can influence Tesla depreciation include:

- Rapid Model Evolution: Tesla frequently updates its models (e.g., new battery chemistries, sensor upgrades), which can make older versions seem less desirable.

- Price Adjustments: Tesla’s dynamic pricing strategy, where new car prices can fluctuate, can impact the resale market for existing vehicles.

- FSD Transferability: The ability (or inability) to transfer the FSD package to a new owner can significantly affect the used car’s value. If FSD is tied to the original owner or subscription, it doesn’t add as much value to the used car.

For sound financial analysis, understanding these trends allows an owner to project the future residual value of their Tesla, which is crucial for calculating the true total cost of ownership over their intended ownership period.

The Investment Perspective: Is a Tesla a Sound Financial Decision?

From a pure investment standpoint, a car, regardless of its make or model, is generally a depreciating asset. However, evaluating a Tesla as a “sound financial decision” requires looking beyond simple depreciation to a holistic total cost of ownership (TCO) analysis over a 5-10 year horizon.

While the initial outlay for a Tesla can be high, the financial benefits often accumulate over time:

- Lower Operating Costs: Significant savings on fuel and reduced maintenance translate into substantial financial benefits annually.

- Environmental Benefits (Indirect Financial Value): While not a direct financial return, contributing to environmental sustainability aligns with certain investment philosophies and can have intangible benefits.

- Potential for Energy Independence: For owners with solar panels and battery storage, a Tesla can further reduce reliance on traditional energy grids, offering a degree of financial resilience.

Calculating the TCO involves summing the initial purchase price (net of incentives), finance charges, insurance, charging costs, and maintenance, then subtracting the projected resale value. Many studies and owner experiences suggest that over a 5-7 year period, the TCO of a Tesla can be competitive with, or even lower than, that of a premium gasoline-powered vehicle, especially when factoring in tax credits and fuel savings. For businesses, this analysis is critical for fleet budgeting, assessing ROI, and demonstrating commitment to ESG (Environmental, Social, and Governance) goals.

Financing Options and Their Financial Implications

The method chosen to finance a Tesla significantly impacts its overall financial footprint. The primary options are outright purchase, traditional auto loan, or leasing.

- Outright Purchase: While requiring substantial upfront capital, this eliminates interest payments and offers full ownership from day one. It’s ideal for those with strong cash reserves or a preference for avoiding debt.

- Auto Loan: The most common financing method, an auto loan spreads the cost over several years (e.g., 60, 72, or 84 months). Key financial considerations include:

- Down Payment: A larger down payment reduces the loan principal, leading to lower monthly payments and less interest paid over the loan term.

- Interest Rate (APR): Even a seemingly small difference in APR can translate to thousands of dollars in interest over the life of the loan. Securing the lowest possible rate is crucial.

- Loan Term: Shorter terms mean higher monthly payments but less interest paid overall, while longer terms reduce monthly payments but increase total interest.

- Leasing: Leasing involves paying for the depreciation of the vehicle over a set period (typically 24-36 months) plus interest, taxes, and fees, rather than purchasing the car outright.

- Lower Monthly Payments: Leases generally have lower monthly payments than loan financing for the same vehicle.

- No Ownership: At the end of the lease, the car is returned, avoiding depreciation risk and the hassle of selling.

- Mileage Restrictions: Leases come with mileage limits, incurring fees if exceeded.

- No Equity Build-Up: Unlike a loan, you don’t build equity in the vehicle.

The choice between buying and leasing depends on individual financial goals, planned ownership duration, annual mileage, and cash flow preferences. A thorough financial assessment of each option, including calculating total costs over the expected ownership period, is vital for making an informed decision that aligns with one’s personal or business financial strategy.

Strategic Financial Planning for Tesla Ownership

Owning a Tesla is more than just buying a car; it’s an integration into a new financial ecosystem. Strategic financial planning can optimize the experience and mitigate potential risks.

Budgeting for the Unexpected: Contingency Funds

Even with lower routine maintenance, financial prudence dictates budgeting for the unexpected. While Teslas are generally reliable, unforeseen circumstances can arise.

- Non-Warranty Repairs: Beyond the standard warranty, components like the 12V battery might need replacement, or complex sensor issues could arise. While the main battery and drive unit have extended warranties, other sophisticated components are not always covered for the vehicle’s entire lifespan.

- Increased Insurance Rates: Premiums can increase unexpectedly due to general market trends, driving history changes, or even new model updates.

- Tire Replacement: As noted, tire wear can be a significant recurring cost.

- Charging Infrastructure Malfunctions: While home chargers are generally robust, issues could require professional repair or replacement.

Maintaining a dedicated contingency fund for automotive expenses, specifically tailored for EV peculiarities, is a wise financial strategy. This ensures that any unexpected costs do not derail personal budgets or negatively impact business cash flow.

Maximizing Financial Benefits: Utilizing Charging Infrastructure and Off-Peak Rates

Optimizing charging habits is paramount to maximizing financial savings from a Tesla.

- Home Charging During Off-Peak Hours: Many utility companies offer time-of-use (TOU) rates, where electricity is significantly cheaper during off-peak hours (typically overnight). Scheduling charging to occur exclusively during these periods can dramatically reduce electricity costs.

- Leveraging Solar Power: For homeowners with solar panel installations, charging a Tesla directly from self-generated solar power can virtually eliminate “fuel” costs, making the vehicle nearly free to power on a day-to-day basis. This also enhances energy independence, a significant financial hedge against rising energy costs.

- Public Charging Strategies: Understanding the pricing structures of various public charging networks (e.g., Superchargers, Electrify America) and choosing the most cost-effective options for different situations can further optimize expenses. Some workplaces offer free charging, which can represent a substantial annual saving.

Effective management of charging habits is not just about convenience; it’s a direct financial lever that can significantly influence the long-term cost of Tesla ownership.

The Total Cost of Ownership (TCO) Calculation

Ultimately, the most accurate answer to “how much does a Tesla car cost?” comes from a comprehensive Total Cost of Ownership (TCO) calculation. This metric provides a holistic financial view by summing all costs associated with the vehicle over its entire lifespan or a predetermined ownership period, while also factoring in financial benefits.

A robust TCO calculation for a Tesla should include:

- Initial Purchase Price: Net of any federal, state, or local incentives.

- Financing Costs: Total interest paid on a loan or total lease payments.

- Insurance: Total estimated premiums over the ownership period.

- Fueling Costs: Estimated electricity costs (home, Supercharger, public) based on projected mileage and local rates.

- Maintenance & Repairs: Estimated routine service, tires, and potential unexpected repairs.

- Depreciation: The difference between the net purchase price and the projected resale value at the end of the ownership period.

- Other Costs: Registration fees, taxes, home charging installation costs.

By diligently calculating these elements, individuals and businesses can gain a clear financial understanding of what a Tesla truly costs over its lifetime. This granular financial analysis moves beyond the initial excitement to provide an objective, data-driven foundation for a decision that aligns with sound financial principles and long-term monetary well-being. Owning a Tesla represents a significant investment, but when approached with careful financial planning and an understanding of its unique cost structure, it can prove to be a financially astute decision for many.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.