For millions of Americans, Social Security represents the foundation of a stable retirement strategy. It is the one inflation-adjusted income stream that most workers can count on for the duration of their lives. However, the question of “how much” Social Security pays is rarely met with a simple dollar amount. Because the system is designed to replace a portion of your pre-retirement income based on your specific work history, the payout varies significantly from one individual to the next.

Understanding the mechanics of Social Security is not just a matter of curiosity; it is a vital component of personal finance and long-term wealth management. To accurately plan for your “golden years,” you must understand how the Social Security Administration (SSA) calculates benefits, how your choices regarding timing can permanently alter your checks, and what the current landscape looks like for maximum and average payouts.

The Architecture of the Payout: How Benefits Are Calculated

The Social Security benefit formula is progressive, meaning it is designed to provide a higher “replacement rate” for lower-earning workers than for higher-earning ones. To understand what you will receive, you must first look at the variables the SSA uses to build your specific profile.

The 35-Year Earnings Average

The SSA looks at your entire work history, but it only calculates your benefit based on your 35 highest-earning years. These earnings are “indexed” to account for changes in average wages over time, ensuring that your 1990 earnings are viewed through a modern lens. If you have fewer than 35 years of work in the Social Security system, the SSA fills in the remaining years with zeros. This can significantly drag down your average, making it a priority for many workers to reach that 35-year milestone before retiring.

Average Indexed Monthly Earnings (AIME) and the PIA

Once your 35 highest years are indexed and averaged, the SSA divides that total by 420 (the number of months in 35 years) to find your Average Indexed Monthly Earnings (AIME). This figure is then plugged into a formula to determine your Primary Insurance Amount (PIA). The PIA is the base amount you would receive if you retired exactly at your Full Retirement Age (FRA).

The Role of “Bend Points”

The formula used to turn your AIME into your PIA uses “bend points.” For 2024, for example, the formula takes 90% of the first portion of your AIME, 32% of the middle portion, and 15% of any earnings above the final threshold. This tiered approach is why a worker who earned twice as much as their neighbor throughout their career will not receive a Social Security check that is twice as large; the “bend points” ensure a safety net for lower earners while capping the benefits of high earners.

The Impact of Timing: When You Claim Matters

While your earnings history sets the baseline for your benefit, the age at which you choose to start receiving checks is the single most important factor in determining the final amount. The “Full Retirement Age” is no longer 65 for most current workers; it has shifted based on your birth year.

Understanding Your Full Retirement Age (FRA)

For anyone born in 1960 or later, the Full Retirement Age is 67. If you were born between 1943 and 1954, it is 66. For those born in the years in between, it increases by two months for every year. Claiming at your FRA ensures you receive 100% of your calculated PIA. If you claim even one month early or late, that 100% figure is permanently adjusted.

The Cost of Claiming Early (Age 62)

You can choose to claim Social Security as early as age 62, but there is a steep price for doing so. Claiming at 62 results in a permanent reduction of your benefits. If your FRA is 67 and you claim at 62, your monthly check will be reduced by 30%. This reduction is calculated month-by-month: for the first 36 months before FRA, the benefit is reduced by 5/9 of 1% per month. Beyond 36 months, it is reduced by an additional 5/12 of 1% per month. While you get more checks over your lifetime by starting early, each check is significantly smaller.

The Reward for Delayed Retirement (Age 70)

On the opposite end of the spectrum, you can choose to delay claiming benefits past your FRA. For every year you wait—up until age 70—your benefit increases by 8% annually. This is known as “Delayed Retirement Credits.” If your FRA is 67 and you wait until age 70, you will receive 124% of your PIA for the rest of your life. In the world of personal finance, a guaranteed 8% annual increase is an incredibly high “return on investment,” which is why many financial advisors recommend waiting as long as possible if you have the health and savings to do so.

Maximum Payouts and Current Financial Realities

To put “how much” into perspective, we must look at the actual numbers provided by the SSA for the current year. These figures represent the ceiling and the average of what Americans are currently receiving.

The 2024 Maximum Benefit

There is a limit to how much you can receive from Social Security, regardless of how much you earned. This is because there is a “taxable maximum”—a cap on the amount of earnings subject to Social Security taxes each year. For 2024, the maximum monthly Social Security benefit for someone retiring at age 70 is $4,873. If you retire at your FRA (67), the maximum is $3,822. If you retire at 62, the maximum is just $2,710. To hit these maximums, you must have earned at or above the taxable wage base for at least 35 years.

National Averages and Reality Checks

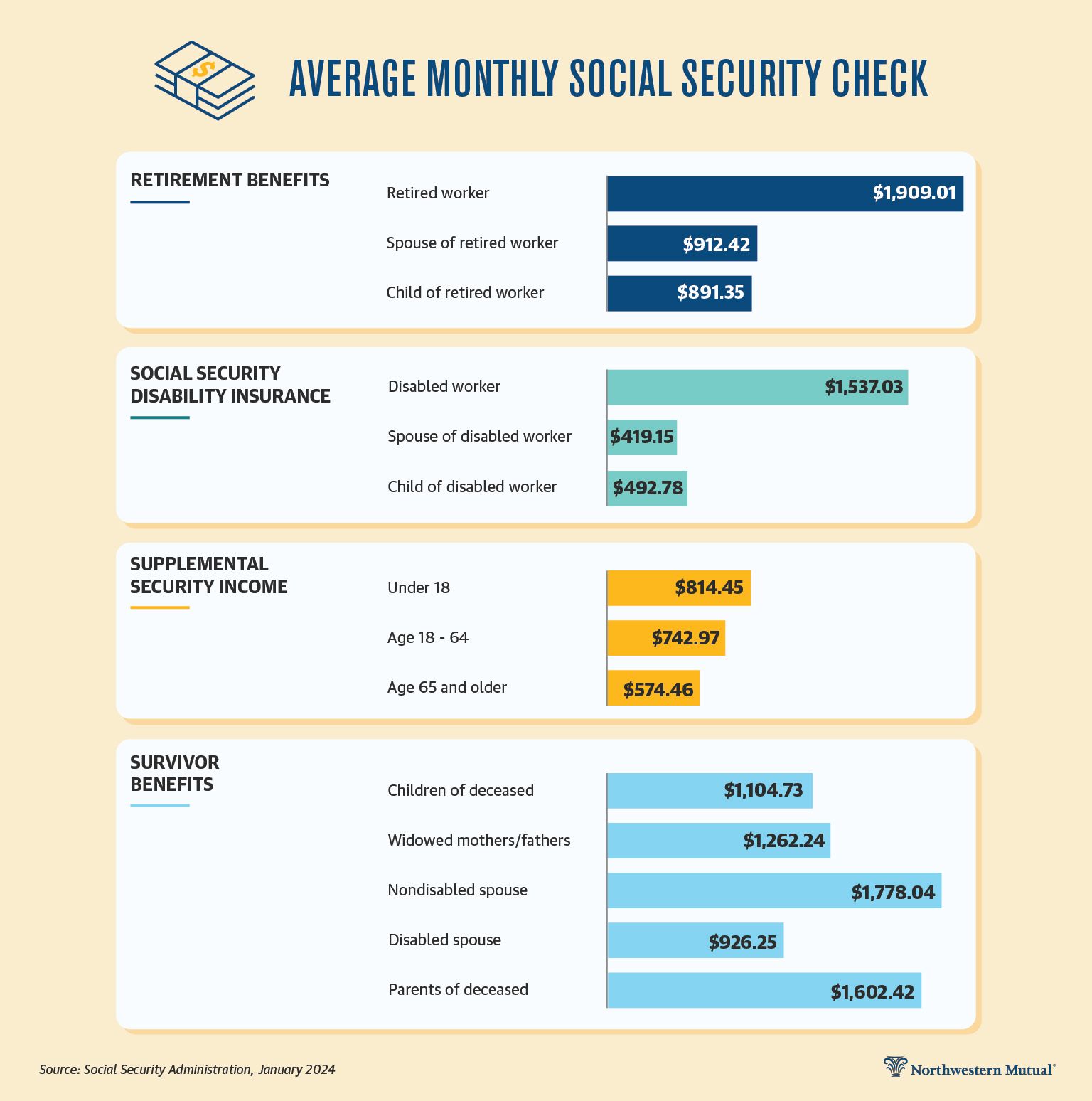

While the maximums sound substantial, the reality for the average American is different. As of early 2024, the average monthly Social Security benefit for a retired worker is approximately $1,900. While this provides a critical floor for expenses, it highlights that Social Security is intended to replace only about 40% of the average worker’s pre-retirement income. For those in higher income brackets, that replacement rate is often closer to 20% or 25%.

COLA: Protecting Purchasing Power

One of the most valuable features of Social Security is the Cost-of-Living Adjustment (COLA). Every year, the SSA evaluates the Consumer Price Index to determine if benefits should increase to keep up with inflation. In years of high inflation, such as 2023, the COLA can be as high as 8.7%. In 2024, it was 3.2%. This ensures that the “how much” of today maintains its value in the “how much” of tomorrow, a feature that few private pensions or annuities offer.

Strategic Considerations for Maximizing Your Benefit

Determining how much Social Security will pay you isn’t just about reading a statement; it’s about active financial management. There are several strategies you can employ to ensure you are capturing the maximum amount possible for your household.

Optimizing High-Earning Years

Because the formula uses your top 35 years, your earnings in your late 50s and early 60s are often your most impactful. If you had several low-earning years early in your career, working just a few more years at a higher peak salary can “flush out” those low-earning years from your average, boosting your PIA significantly.

Spousal and Survivor Benefits

Social Security isn’t just about your own work record. If you are married, you may be eligible for a spousal benefit that is worth up to 50% of your spouse’s PIA. This is particularly beneficial if one spouse was a much higher earner than the other. Additionally, survivor benefits allow a widowed spouse to “step into the shoes” of the deceased spouse, taking over their higher benefit amount. Financial planning for couples often involves the higher earner delaying benefits until 70 to ensure the highest possible survivor benefit for the remaining spouse.

The Impact of Taxes on Your Benefits

A common surprise in personal finance is that Social Security benefits can be taxable. If your “combined income” (adjusted gross income + nontaxable interest + half of your Social Security benefits) exceeds $25,000 for individuals or $32,000 for couples, you may owe federal income tax on up to 50% to 85% of your benefits. Understanding these thresholds is essential for tax-efficient withdrawal strategies from your 401(k) or IRA, as those distributions can push your Social Security into a taxable bracket.

Conclusion: Integrating Social Security into Your Wealth Plan

The answer to “how much does Social Security pay” is ultimately a reflection of your career’s longevity, your peak earnings, and your patience in waiting to claim. While the average check sits around $1,900, the range from $2,710 to $4,873 for high earners demonstrates the power of timing and income.

Social Security should never be viewed in a vacuum. It is one leg of a “three-legged stool” that includes personal savings (like IRAs and 401(k)s) and private pensions or home equity. By understanding the formulas, avoiding the “early retirement trap” unless necessary, and accounting for the tax implications, you can maximize this government-guaranteed income stream and build a more resilient financial future. Regardless of where you are in your career, checking your Social Security statement annually at ssa.gov is the first step in taking control of your retirement’s most important number.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.