Refinancing a car loan can be a strategic financial move for many vehicle owners, potentially leading to significant savings over the life of the loan. However, like any financial transaction, it’s natural to wonder about the associated costs. While the primary goal of refinancing is often to reduce monthly payments or secure a lower interest rate, there can be various fees and charges involved that impact the overall financial benefit. Understanding these costs upfront is crucial for making an informed decision and ensuring that refinancing truly aligns with your financial objectives. This comprehensive guide will break down the typical expenses, hidden fees, and critical factors that influence the cost of refinancing your car, helping you navigate the process with confidence.

Understanding Car Refinancing and Its Potential Benefits

Before diving into the costs, it’s essential to grasp what car refinancing entails and why it might be a beneficial option for you. Refinancing essentially means replacing your existing car loan with a new one, typically from a different lender, though sometimes from the same one under new terms.

What is Car Refinancing?

At its core, refinancing a car loan involves taking out a new loan to pay off your current auto loan. The new loan will come with a new interest rate, new monthly payments, and a potentially new loan term (the period over which you pay back the loan). The goal is almost always to improve upon the terms of your original loan, making your car ownership more affordable or manageable.

Why Consider Refinancing Your Car?

There are several compelling reasons why car owners choose to refinance:

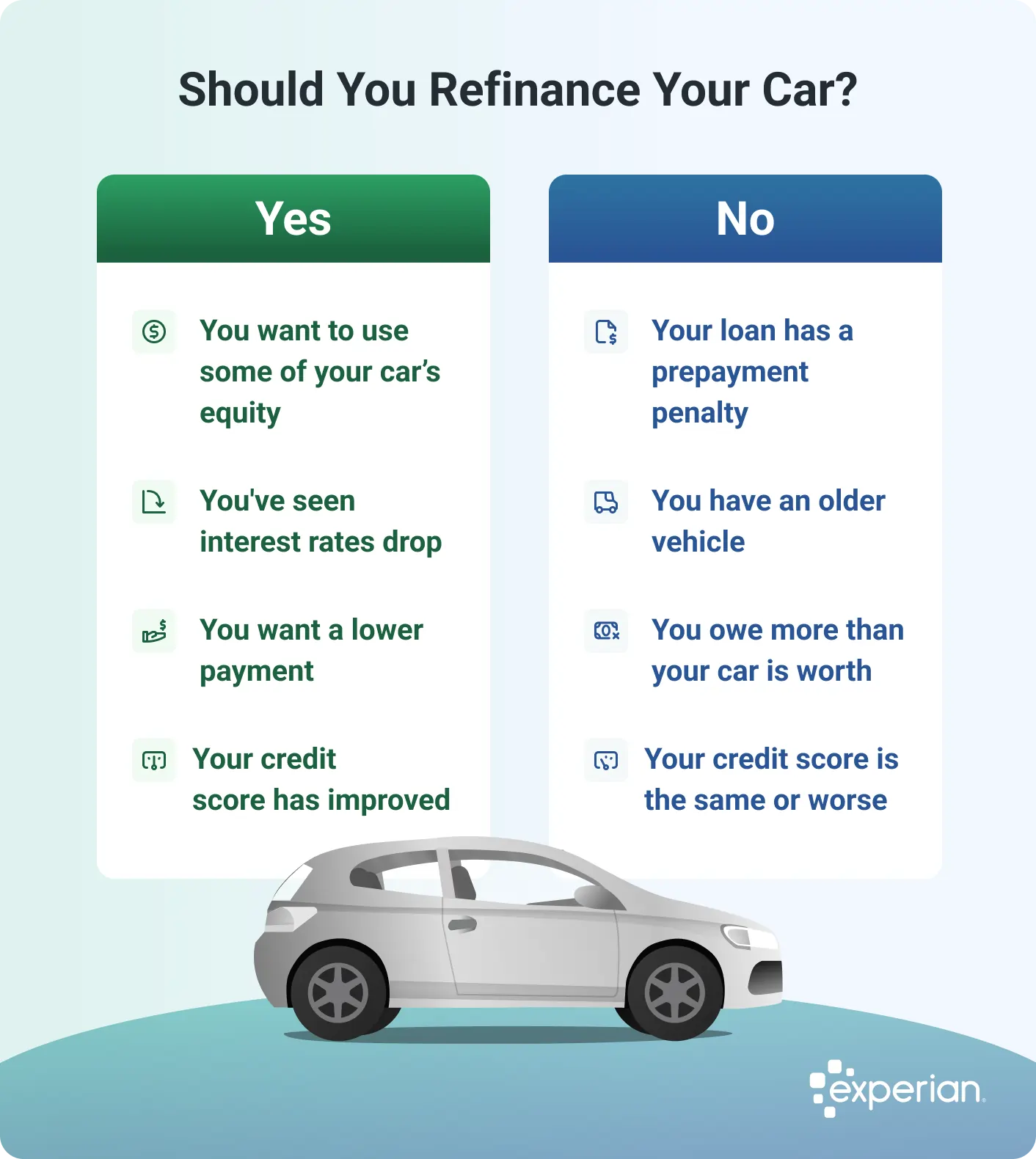

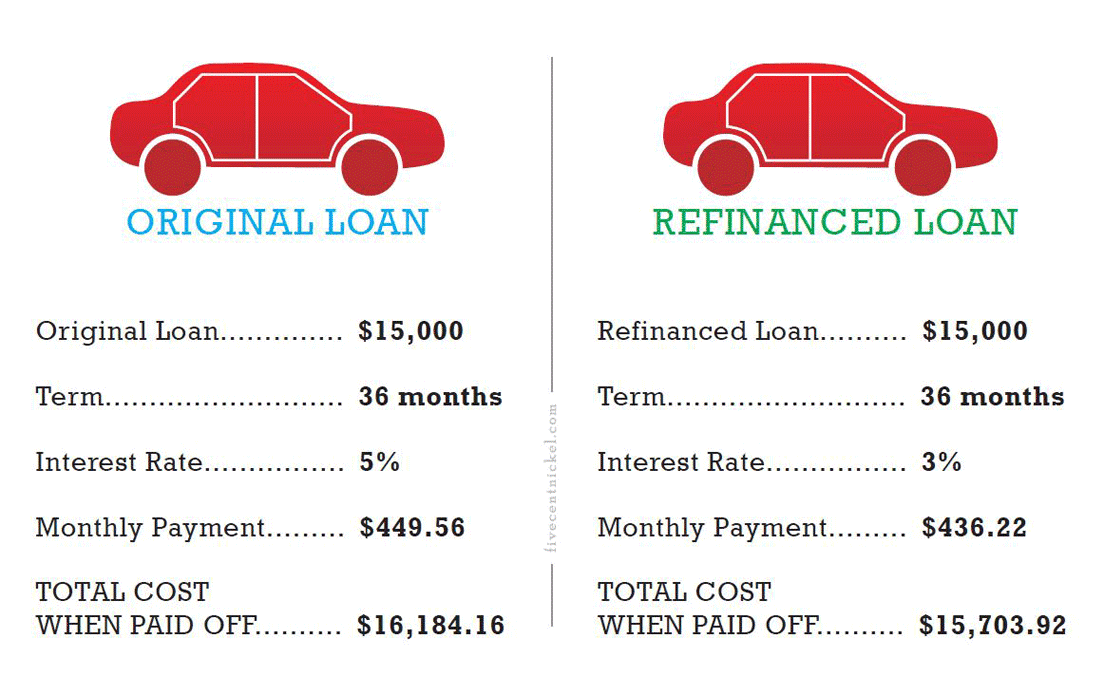

- Lower Interest Rate: This is the most common reason. If your credit score has improved since you first bought the car, or if market interest rates have dropped, you might qualify for a significantly lower Annual Percentage Rate (APR). A lower APR translates directly into less interest paid over the life of the loan and lower monthly payments.

- Lower Monthly Payments: Even without a drastically lower interest rate, extending the loan term can reduce your monthly payment, freeing up cash flow. Be cautious, though, as a longer term can mean paying more interest overall, even if the monthly payment is lower.

- Change Loan Term: You might want to shorten your loan term to pay off the car faster and save on interest, or extend it to reduce your monthly burden.

- Remove a Co-signer: If a co-signer helped you qualify for your original loan, refinancing can allow you to take sole responsibility for the loan, releasing them from their obligation.

- Access Cash (Cash-out Refinance): Some lenders offer “cash-out” refinancing, where you borrow more than you owe on the car and receive the difference in cash. This is less common for auto loans than for mortgages and should be approached with extreme caution due to the risk of going upside down on the loan.

When is the Right Time to Refinance?

The optimal time to refinance often depends on a few key factors: your credit score has improved, market interest rates have fallen, you’ve made a significant number of payments on your original loan and built equity, or your financial situation has stabilized. It’s generally not advisable to refinance very early in your loan term if you have substantial prepayment penalties, or if your car’s value has depreciated significantly, putting you in an upside-down position (owing more than the car is worth).

Deconstructing the Costs of Car Refinancing

While the potential benefits of refinancing can be substantial, it’s crucial to be aware of the fees that might diminish those savings. Fortunately, car loan refinancing typically involves fewer fees than mortgage refinancing, but they do exist.

Origination Fees: Rare but Possible

An origination fee is a charge from the lender for processing a new loan. While common in mortgages, origination fees are relatively rare for auto loan refinancing. Some lenders, particularly those dealing with borrowers with lower credit scores or specific loan products, might charge one. These fees can range from a small flat amount to a percentage of the loan principal. Always ask your prospective lender if an origination fee applies.

Title and Registration Fees

When you refinance your car loan, the lienholder changes from your original lender to the new one. This change needs to be updated on your vehicle’s title with your state’s Department of Motor Vehicles (DMV) or equivalent agency. You will likely incur a state-mandated fee for updating the title and potentially for new registration, especially if your new lender is in a different state or has specific requirements. These fees are usually relatively minor, often in the range of $15 to $100, varying by state.

Lien Holder Fees

Some states or lenders might have specific fees associated with changing the lienholder on a vehicle. This is often tied into the title transfer process but can sometimes be a separate administrative charge. It’s important to clarify with your new lender and your state’s DMV about all fees related to the change of lien.

Prepayment Penalties (from the original loan)

While not a direct cost of the new refinance loan, a prepayment penalty can be a significant cost associated with ending your original loan early. Some auto loan contracts include clauses that charge a fee if you pay off the loan before its scheduled term. These penalties are designed to compensate the original lender for the interest they lose when you pay off the loan early. Before refinancing, meticulously review your current loan agreement for any prepayment penalty clauses. If such a penalty exists, factor it into your cost-benefit analysis. Fortunately, many auto loans, especially those from credit unions or major banks, do not include prepayment penalties.

Credit Report Fees

When you apply for a new loan, lenders will pull your credit report to assess your creditworthiness. Some lenders might pass on the cost of this credit check to the applicant. These fees are typically small, often under $30, and are usually rolled into the overall loan cost or simply absorbed by the lender.

Potential Savings vs. Upfront Costs

The key to a successful refinance is ensuring that the savings you achieve through a lower interest rate or better terms outweigh any upfront costs. Calculate the total cost of fees, add any prepayment penalties from your old loan, and then compare that against the total interest saved over the new loan term. If the fees are minimal and the interest savings substantial, refinancing is likely a wise move.

Factors Influencing Your Refinancing Costs and Eligibility

The actual interest rate and the number of fees you encounter will largely depend on several personal and market factors. Understanding these can help you position yourself for the best possible refinancing offer.

Your Credit Score

Your credit score is arguably the most critical factor influencing your interest rate. A higher credit score (typically FICO scores above 700-740) signals less risk to lenders, making you eligible for their most competitive rates. If your credit score has improved significantly since you took out your original loan, you’re in a prime position to secure a lower rate. Conversely, a lower credit score might lead to higher interest rates, potentially diminishing the benefits of refinancing.

Your Debt-to-Income (DTI) Ratio

Lenders also look at your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income to cover your loan payments, making you a more attractive borrower. Lenders prefer DTI ratios typically below 43%, though this can vary. A high DTI might lead to higher interest rates or even loan denial.

Vehicle Age and Mileage

The age and mileage of your vehicle play a role because they affect the car’s collateral value. Lenders are more reluctant to finance older, high-mileage vehicles at very favorable rates because their resale value is lower, increasing the risk for the lender. Most lenders have limits on the age and mileage of vehicles they will refinance, often capping it around 7-10 years old and 100,000-150,000 miles.

Current Market Interest Rates

Economic conditions significantly influence auto loan interest rates. If the Federal Reserve has lowered interest rates, or if there’s increased competition among lenders, you might find lower rates available than when you originally financed your car. Keeping an eye on prevailing market rates can help you identify opportune times to refinance.

Lender Specifics and Policies

Different lenders have different risk appetites, fee structures, and loan offerings. A credit union, for instance, might offer more competitive rates and fewer fees than a traditional bank or an online lender, depending on their operational model and membership requirements. It’s crucial to shop around and compare offers from various types of lenders.

The Refinancing Process: Step-by-Step and What to Expect

Knowing the typical steps involved in refinancing can help demystify the process and allow you to anticipate what’s coming next.

Gathering Your Documents

Before applying, prepare essential documents. This typically includes your driver’s license, proof of income (pay stubs, tax returns), proof of residence, your current loan statements (including payoff amount), vehicle information (VIN, make, model, mileage), and insurance details. Having these ready will streamline your application process.

Shopping Around for Lenders

This is perhaps the most crucial step. Don’t settle for the first offer. Apply to several lenders, including banks, credit unions, and online auto lenders. Each will have different rates, terms, and fees. Use pre-qualification processes (which usually involve a “soft” credit pull that doesn’t harm your score) to get initial rate estimates without commitment.

Submitting Your Application

Once you’ve chosen a few promising lenders, you’ll submit formal applications. This will involve a “hard” credit inquiry, which might temporarily ding your credit score by a few points. However, credit scoring models typically group multiple auto loan inquiries within a short period (e.g., 14-45 days) as a single inquiry, so shopping around within a concentrated timeframe is advisable.

Reviewing the Loan Offer

Carefully review each loan offer. Pay close attention to the APR (which includes the interest rate plus certain fees), the loan term, the total amount of interest you’ll pay, and any specific fees. Ensure you understand all the terms and conditions before proceeding.

Finalizing the Refinance

Once you accept an offer, the new lender will typically pay off your old loan. You’ll then begin making payments to your new lender under the new terms. The new lienholder information will be updated on your vehicle’s title, a process often handled directly by the lender or a third-party service they employ.

Maximizing Your Savings and Avoiding Hidden Fees

To ensure you get the most out of your car refinance, proactive steps can make a significant difference in both the rate you secure and the fees you encounter.

Improving Your Credit Score Before Applying

If you know you want to refinance in the near future, take steps to boost your credit score. Pay down other debts, make all payments on time, and avoid opening new lines of credit. Even a small improvement can lead to a better interest rate offer.

Negotiating with Lenders

Don’t be afraid to negotiate. If you receive competing offers, you can sometimes leverage one offer to get a better rate or lower fees from another lender. Some lenders may be willing to waive small fees to secure your business.

Reading the Fine Print Thoroughly

Always, always read the entire loan agreement before signing. Look for any hidden fees, prepayment penalties on the new loan, or unusual clauses. If anything is unclear, ask for clarification. An informed borrower is an empowered borrower.

Understanding APR vs. Interest Rate

The Annual Percentage Rate (APR) is typically a more accurate measure of the true cost of a loan than the interest rate alone, as it includes certain fees in its calculation. When comparing offers, always compare APRs for a clearer picture of the total borrowing cost.

The Importance of a Cost-Benefit Analysis

Before committing, perform a thorough cost-benefit analysis. Calculate the total interest saved over the new loan term, subtract all associated fees (including any old loan prepayment penalties), and then divide by the number of months in the new term to see your net monthly savings. This will give you a clear financial picture of whether refinancing is truly worth it for your specific situation.

In conclusion, refinancing a car loan can be a powerful tool for improving your financial health, primarily by reducing your interest expenses and monthly payments. While there are potential costs involved, they are often minor compared to the long-term savings. By understanding the process, knowing what fees to look for, and diligently shopping around, you can navigate the refinancing landscape confidently and secure terms that benefit your budget significantly.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.