Tax season often brings a sense of trepidation, fueled by the complex interplay of income, deductions, and ever-changing legislation. For the savvy individual focused on personal finance and wealth management, the question “How much do I owe in taxes?” is not merely a seasonal inquiry—it is a critical component of annual financial planning. Understanding your tax liability is essential for maintaining liquidity, optimizing investment returns, and ensuring long-term fiscal health.

This guide delves into the mechanics of tax calculation, the nuances of different income streams, and the strategic maneuvers you can employ to minimize your obligation and maximize your net worth.

Understanding the Foundation of Your Tax Bill

Before you can determine the specific dollar amount owed to the government, you must understand the structural framework of the tax system. Your final tax bill is not a flat percentage of every dollar you earn; it is the result of a multi-layered process that begins with your total earnings and ends with your final credits.

Gross Income vs. Adjusted Gross Income (AGI)

The journey begins with your Gross Income. This includes everything from your salary and bonuses to dividends, interest, and rental income. However, the government does not tax you on this raw number. Instead, you calculate your Adjusted Gross Income (AGI) by subtracting specific “above-the-line” deductions. These can include contributions to a traditional IRA, student loan interest payments, and health savings account (HSA) contributions. Your AGI is a pivotal number because it often determines your eligibility for various tax credits and further deductions.

Standard Deduction vs. Itemized Deductions

Once you have your AGI, you must decide how to reduce your taxable income further. Most taxpayers opt for the Standard Deduction, a fixed dollar amount that reduces the income you’re taxed on. The alternative is Itemizing Deductions, where you list specific expenses such as mortgage interest, state and local taxes (SALT) up to a certain limit, and charitable contributions. If your itemized expenses exceed the standard deduction, itemizing is the mathematically superior choice for reducing what you owe.

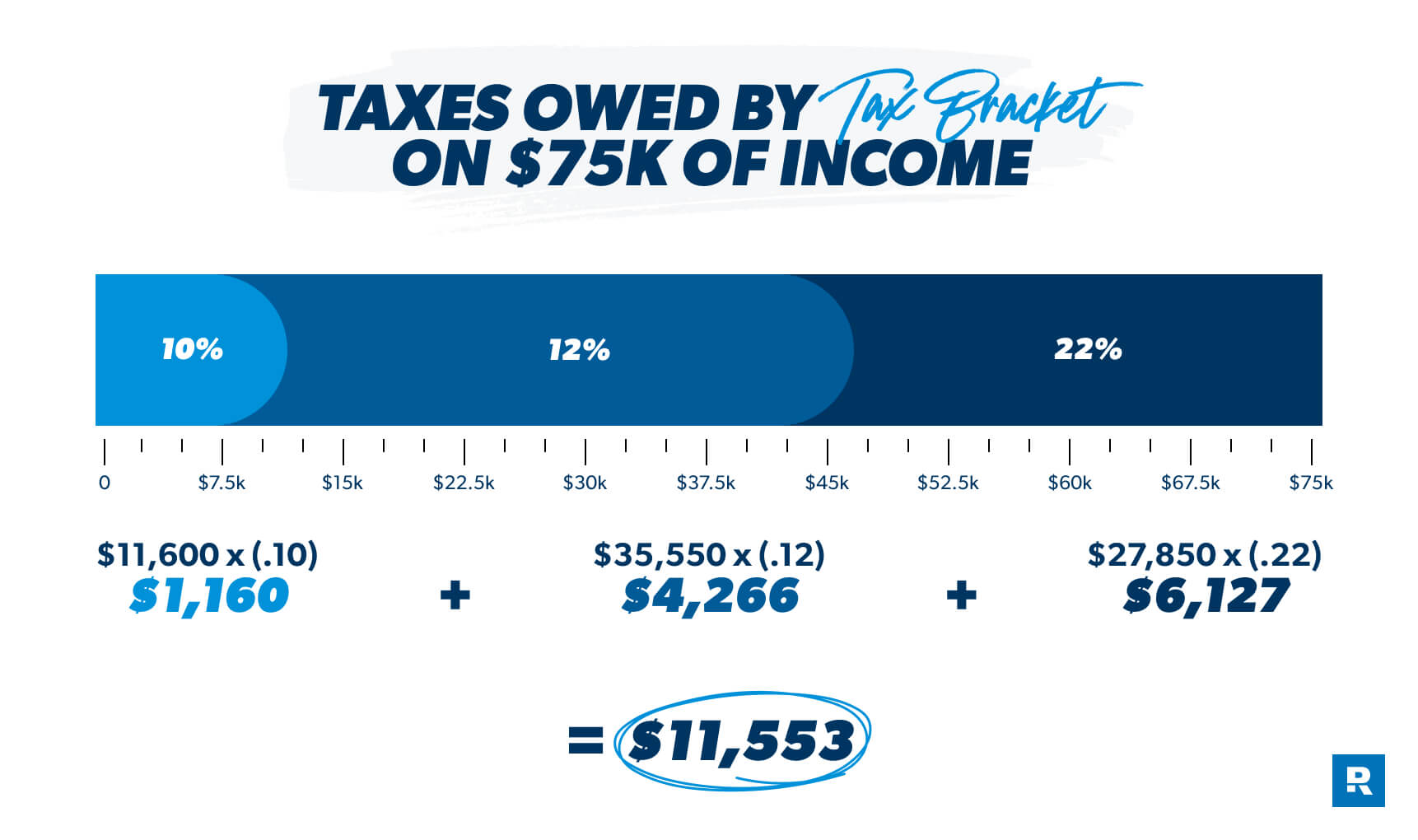

The Role of Tax Brackets and Marginal Rates

A common misconception in personal finance is that moving into a higher tax bracket means all your income is taxed at that higher rate. The U.S. uses a progressive tax system. This means your income is divided into “buckets.” The first bucket is taxed at the lowest rate, the next portion at the second rate, and so on. Your “marginal tax rate” is the rate applied to the last dollar you earned. Understanding this distinction helps in realizing that an increase in pay rarely results in less “take-home” pay due to taxes.

Calculating Tax Liability for Different Income Streams

In the modern economy, income rarely comes from a single source. Whether you are a traditional employee, a freelancer, or an investor, the way your income is classified significantly impacts your tax liability.

Traditional Employment (W-2) and Withholdings

For those with traditional W-2 employment, the process is largely automated. Your employer withholds a portion of your paycheck for federal and state taxes based on the information provided in your Form W-4. At the end of the year, if your total withholdings exceed your calculated tax liability, you receive a refund. If they are less, you owe the difference. Monitoring your withholdings mid-year is a proactive way to ensure you don’t face a massive, unexpected bill in April.

Self-Employment, Side Hustles, and the 1099 Economy

The rise of the “side hustle” has introduced many to the complexities of self-employment tax. If you earn income as a contractor or business owner, you are responsible for both the employer and employee portions of Social Security and Medicare taxes—commonly referred to as the Self-Employment Tax (currently 15.3%). Because there is no employer to withhold these funds, self-employed individuals must often pay “estimated taxes” quarterly. Failing to do so can lead to underpayment penalties, making it vital to set aside roughly 25-30% of your gross freelance earnings for the IRS.

Capital Gains and Investment Income

How much you owe on investments depends on how long you held the asset. Short-term capital gains (on assets held for a year or less) are taxed as ordinary income. However, long-term capital gains (on assets held for more than a year) benefit from preferential tax rates—0%, 15%, or 20%—depending on your total taxable income. For the long-term investor, this distinction is a powerful tool for wealth preservation, as it allows capital to grow with less friction from the tax man.

Strategies to Reduce What You Owe

Effective tax planning is a year-round activity, not a last-minute scramble. By understanding the levers available to you, you can significantly lower your effective tax rate.

Tax Credits vs. Tax Deductions

It is crucial to distinguish between these two. A deduction lowers the amount of income you are taxed on. If you are in the 24% tax bracket, a $1,000 deduction saves you $240. A tax credit, however, is a dollar-for-dollar reduction of your actual tax bill. A $1,000 credit saves you $1,000. Common credits include the Child Tax Credit, the Earned Income Tax Credit (EITC), and various energy-efficiency credits for home improvements. Always prioritize credits, as they offer the highest financial impact.

Maximizing Retirement Contributions

One of the most effective ways to lower your tax bill is to pay your future self. Contributions to a Traditional 401(k) or 403(b) and a Traditional IRA are typically tax-deductible. By diverting income into these accounts, you lower your AGI, which can potentially drop you into a lower tax bracket. While you will eventually pay taxes when you withdraw the money in retirement, the immediate tax savings allow more of your money to benefit from compound interest today.

Health Savings Accounts (HSA) and Flexible Spending Accounts (FSA)

For those with high-deductible health plans, an HSA is a triple-threat financial tool. Contributions are tax-deductible, the growth is tax-free, and withdrawals for qualified medical expenses are tax-free. Unlike an FSA, which is often “use-it-or-lose-it,” HSA funds roll over annually and can eventually act as a secondary retirement account. Using these accounts effectively reduces your taxable income while creating a safety net for healthcare costs.

Essential Financial Tools for Tax Estimation

In the digital age, you don’t have to guess how much you owe. Leveraging technology and professional expertise can turn tax estimation from a mystery into a manageable line item in your budget.

Using IRS Tax Withholding Estimators

The IRS provides a robust online Tax Withholding Estimator. By inputting your current pay stubs and most recent tax return, the tool can predict whether you are on track to owe money or receive a refund. This is particularly useful after major life events—such as getting married, having a child, or buying a home—all of which change your tax profile.

The Importance of Keeping Accurate Digital Records

The “how much do I owe” question is impossible to answer accurately without good data. Utilizing financial management software allows you to categorize expenses in real-time. For business owners and freelancers, tracking deductible expenses such as home office costs, professional development, and travel is essential. Every forgotten deduction is essentially a tip given to the government.

When to Consult a Financial Advisor or CPA

While tax software is sufficient for many, high-net-worth individuals or those with complex business structures should seek professional counsel. A Certified Public Accountant (CPA) or a tax-focused financial advisor can identify “tax-loss harvesting” opportunities in your investment portfolio or suggest corporate structures (like an S-Corp election) that could save thousands in self-employment taxes. The fee for a professional is often far less than the savings they generate.

Planning for the Future: Quarterly Payments and Tax Efficiency

Once you understand what you owe for the current year, the final step is to build a proactive strategy for the years to come.

Avoiding Underpayment Penalties

The IRS operates on a “pay-as-you-go” system. If you expect to owe more than $1,000 when you file your return, you may be required to make quarterly estimated tax payments. To avoid penalties, you generally must pay at least 90% of the current year’s tax or 100% of the tax shown on your return for the prior year (the “Safe Harbor” rule). Managing these payments quarterly prevents a massive cash flow crunch in April.

Long-term Tax-Efficient Investing

Finally, consider the “tax-efficiency” of your assets. Place tax-inefficient assets (like high-turnover mutual funds or bonds that pay regular interest) in tax-advantaged accounts like IRAs. Place tax-efficient assets (like index funds or stocks you plan to hold for decades) in standard taxable brokerage accounts. This strategy, known as Asset Location, ensures that your investment growth is hindered as little as possible by annual tax bites.

Understanding how much you owe in taxes is more than just a compliance requirement; it is a fundamental skill in personal finance. By mastering the components of your tax bill—from income classification to the strategic use of credits—you transition from a passive taxpayer to an active manager of your financial destiny. Knowledge of the tax code is, quite literally, money in the bank.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.