Understanding your annual income is arguably the single most crucial piece of information for effective personal financial management. It’s the bedrock upon which all budgeting, saving, investing, and long-term financial planning is built. Yet, for many, especially those with diverse income streams, variable work schedules, or complex compensation packages, accurately calculating this figure can feel like navigating a labyrinth. This is where an “annual income calculator” becomes an indispensable tool, transforming a daunting task into an accessible exercise in financial empowerment.

This comprehensive guide will delve into the critical importance of knowing your yearly earnings, break down the components that contribute to this figure, explore the practical applications of various calculation tools, and ultimately reveal how this seemingly simple number can unlock profound insights into your financial health and future potential. Whether you’re a salaried employee, a seasoned freelancer, a gig economy participant, or someone managing multiple revenue streams, mastering the annual income calculation is your first step towards greater financial control and confidence.

The Imperative of Knowing Your Annual Income

At its core, knowing your annual income isn’t just about a number; it’s about clarity, control, and foresight. It provides a definitive metric that informs every financial decision you make, from the mundane to the monumental. Without a clear understanding of what you earn annually, you’re essentially flying blind in your financial journey, making it difficult to set realistic goals or even understand your current position.

Foundation for Sound Financial Planning

The annual income figure is the cornerstone of any robust financial plan. It dictates the limits and possibilities of your spending, saving, and investment strategies. When you know your total yearly earnings, you can accurately project cash flow, allocate funds to different categories, and ensure that your expenditures do not consistently outstrip your income. This foundational knowledge prevents financial stress, reduces reliance on credit, and paves the way for responsible money management.

For budgeting, knowing your annual income allows you to create a realistic monthly budget that aligns with your true earning capacity. It moves you beyond guesswork, enabling you to set fixed percentages for housing, food, transportation, and discretionary spending, all relative to your actual earnings. This clarity fosters disciplined spending habits and ensures you’re not overextending your financial reach.

Empowering Financial Goal Setting

Whether your aspirations involve buying a home, funding a child’s education, saving for retirement, or launching a new business, each goal requires a clear understanding of your capacity to save and invest. Your annual income directly impacts how much you can reasonably set aside each month or year towards these objectives.

An accurate annual income calculation allows you to:

- Set Realistic Savings Targets: If you aim to save 10-20% of your income, knowing the total makes this calculation straightforward and achievable.

- Plan for Major Purchases: From down payments on property to financing a new car, lenders and financial advisors will always assess your affordability based on your annual income.

- Strategize Retirement Contributions: Understanding your income helps determine how much you can contribute to IRAs, 401(k)s, or other retirement vehicles to maximize tax advantages and compound growth.

- Evaluate Investment Potential: Your disposable income, derived from your annual earnings after expenses, determines your capacity for investments that can grow your wealth over time.

Navigating Tax Obligations and Loan Applications

Beyond personal planning, your annual income plays a critical role in your interactions with external financial entities. It’s the primary data point for tax authorities and a key determinant for loan approvals.

For tax planning, a precise annual income figure helps you estimate your tax liability, identify potential deductions, and plan for quarterly payments if you’re self-employed. It ensures you’re not caught off guard by unexpected tax bills and allows for proactive strategies to optimize your tax position. Understanding your gross vs. net annual income is particularly crucial here, as it clarifies your taxable income.

In the realm of loan and mortgage applications, lenders meticulously scrutinize your annual income to assess your creditworthiness and repayment capacity. Your debt-to-income ratio, a critical metric for loan approval, is directly calculated using your annual income. A higher, stable income often translates to better loan terms, lower interest rates, and greater access to financing for significant life purchases. Without an accurate figure, you risk misrepresenting your financial standing, which could lead to application rejections or less favorable terms.

Deconstructing Annual Income: Beyond the Paycheck

Calculating your annual income is not always as simple as multiplying your hourly wage by 2080 (40 hours x 52 weeks). It requires a holistic view that encompasses all sources of earnings and differentiates between various income types. Understanding these components is key to generating a truly accurate annual figure.

Gross vs. Net: Understanding the Core Difference

One of the most fundamental distinctions in income calculation is between gross income and net income.

- Gross Annual Income: This is your total earnings before any deductions are taken out. It includes your salary, wages, bonuses, commissions, tips, self-employment profits, investment gains, rental income, and any other money you receive. This is often the figure lenders and landlords are most interested in, as it represents your overall earning capacity.

- Net Annual Income: Also known as “take-home pay,” this is what you actually receive after all deductions. These deductions typically include federal, state, and local taxes, Social Security and Medicare contributions (FICA), health insurance premiums, retirement plan contributions (e.g., 401(k), IRA), union dues, and any other pre-tax or post-tax deductions. Your net income is the figure you use for budgeting your day-to-day expenses.

While an “annual income calculator” often focuses on gross income, a truly comprehensive tool will allow you to factor in common deductions to arrive at your net income, providing a more realistic picture of your spendable funds.

Comprehensive Income Streams: From Salary to Side Hustles

For many, annual income isn’t solely derived from a single, fixed salary. A robust calculation must account for every source of money flowing into your financial ecosystem.

- Salary and Wages: For salaried employees, this is typically the most straightforward component. It’s your agreed-upon annual compensation for your primary job. For hourly employees, it’s your hourly rate multiplied by the average number of hours worked per week, then by 52 weeks. Don’t forget any regularly scheduled overtime.

- Bonuses and Commissions: These variable components can significantly boost your annual income. While they might not be guaranteed, if they are a regular part of your compensation (e.g., annual performance bonuses, sales commissions), it’s crucial to estimate and include them, perhaps by using an average from previous years.

- Self-Employment and Freelance Income: For entrepreneurs, freelancers, and gig workers, calculating annual income involves summing all revenue generated from clients or sales and then deducting legitimate business expenses. What remains is your net profit, which contributes to your personal annual income. This often requires diligent record-keeping throughout the year.

- Investment Income: This includes dividends from stocks, interest from savings accounts or bonds, and capital gains from selling assets. Even if these are reinvested, they still count as income earned.

- Rental Income: If you own property and lease it out, the net income (rent received minus property-related expenses like mortgage interest, maintenance, taxes) contributes to your annual total.

- Other Income Sources: This broad category can include alimony, child support payments, certain government benefits (like unemployment or disability), royalties, and even prize winnings. It’s important to identify if these are recurring and taxable.

Accounting for Variable Earnings and Benefits

The challenge often arises with income sources that are not fixed or guaranteed. How do you accurately factor in unpredictable bonuses, fluctuating freelance projects, or seasonal work?

- Averaging: For variable income, a common approach is to average your earnings over a reasonable period (e.g., the last 3-6 months, or the previous year). While not perfect, it provides a solid estimate.

- Conservative Estimates: When in doubt or planning for the future, it’s often wise to use a conservative estimate for variable income. This ensures you don’t overestimate your funds and potentially overspend.

- Tracking: The most accurate method for variable income is meticulous tracking. Keeping detailed records of every payment received and expense incurred, especially for self-employment, is paramount. This data then feeds directly into your annual income calculator.

Additionally, certain non-cash benefits provided by employers, while not direct cash income, can impact your financial health and should be considered within a broader financial context. These might include employer contributions to health savings accounts (HSAs), retirement plan matching, or discounted services. While not typically included in the core “annual income” calculation for tax purposes, they contribute to your overall compensation package and financial security.

Mastering the Annual Income Calculator: Tools and Techniques

Once you understand the components of your annual income, the next step is to accurately calculate it. Fortunately, a variety of tools and techniques are available, ranging from simple manual calculations to sophisticated financial software. The best approach depends on your income complexity and preference for detail.

From Basic Conversions to Advanced Estimations

For many, the calculation starts with converting a regular pay schedule into an annual figure:

- Salaried Employees: If you have a stated annual salary (e.g., $60,000), this is your gross annual income.

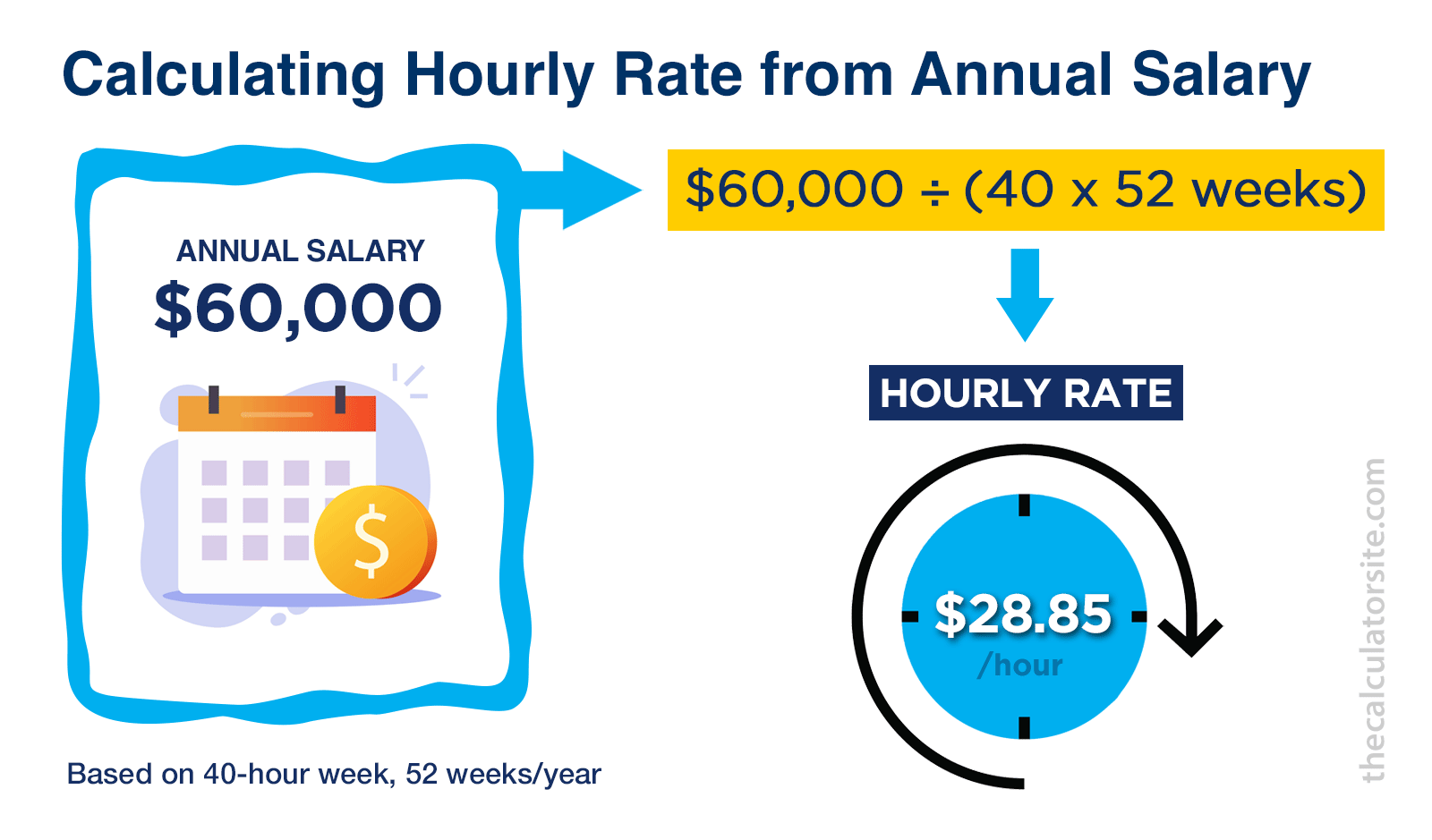

- Hourly Employees: Multiply your hourly wage by the number of hours you work per week, then multiply by 52 weeks.

- Example: $25/hour x 40 hours/week x 52 weeks/year = $52,000 gross annual income.

- Bi-Weekly Pay: If you get paid every two weeks, multiply your bi-weekly pay by 26 (the number of bi-weekly periods in a year).

- Semi-Monthly Pay: If you get paid twice a month, multiply your semi-monthly pay by 24.

- Monthly Pay: Multiply your monthly pay by 12.

The complexity escalates when you introduce variable income. For these scenarios, an “annual income calculator” becomes invaluable by providing fields for different income types and automatically summing them up. Many calculators also offer options to input estimated bonuses, commissions, and self-employment profits, often allowing you to average them over time or input a projected figure.

Leveraging Digital Tools: Online Calculators and Spreadsheets

The digital age offers numerous resources to simplify annual income calculation:

- Online Annual Income Calculators: A quick search reveals countless free online tools. These typically ask for your pay frequency (hourly, weekly, bi-weekly, monthly, annually) and your pay rate, then instantly display your gross annual income. More advanced versions allow you to input multiple income streams, estimated bonuses, and even pre-tax deductions to calculate net income.

- Advantages: User-friendly, instant results, often free.

- Limitations: May not account for all unique income situations or specific state/local tax nuances.

- Spreadsheet Templates (Excel/Google Sheets): For those who prefer a more customized and detailed approach, creating your own spreadsheet is highly effective. You can set up columns for different income sources, track payments as they come in, and automate calculations using formulas. This is particularly useful for freelancers and business owners who need to track expenses alongside revenue.

- Advantages: Highly customizable, excellent for tracking variable income and expenses, can integrate with budgeting.

- Limitations: Requires some familiarity with spreadsheet software.

- Financial Planning Software and Apps: Many personal finance apps (e.g., Mint, YNAB) and robust financial planning software have income tracking features built in. By linking your bank accounts, these tools can often automatically categorize and sum your income, providing real-time insights into your annual earnings.

- Advantages: Comprehensive, integrates with other financial data, often offers advanced analytics.

- Limitations: Can be subscription-based, may require initial setup and ongoing categorization.

Best Practices for Accuracy and Regular Review

To ensure your annual income calculation is always accurate and useful:

- Gather All Documentation: Have your pay stubs, W-2s, 1099s, bank statements, and investment statements readily available. This documentation is crucial for precise figures.

- Be Meticulous with Variable Income: For bonuses, commissions, and freelance earnings, keep a running log throughout the year. Don’t rely on memory.

- Differentiate Gross vs. Net: Always be clear about which figure you are calculating and why. For budgeting, net income is key; for loan applications, gross is often requested.

- Account for Deductions: Understand and factor in all pre-tax and post-tax deductions to get an accurate net income.

- Review Regularly: Your income can change due to raises, new jobs, side hustles, or changes in investment performance. Revisit your annual income calculation at least once a year, or whenever there’s a significant change in your financial situation.

- Consider Future Changes: When making long-term plans, project potential income changes (e.g., expected raises, new income streams) to refine your financial forecasts.

Unlocking Financial Insights: What Your Annual Income Reveals

Knowing your annual income is just the beginning. The real power lies in interpreting this number and using it to gain deeper insights into your financial health, make informed decisions, and strategically plan for your future. It’s a critical metric that influences everything from your daily spending habits to your long-term wealth accumulation.

Assessing Financial Health and Lifestyle Alignment

Your annual income provides a direct lens through which to view your overall financial health. It’s the primary factor determining your capacity for saving, debt repayment, and discretionary spending.

- Budgeting Realism: An accurate annual income figure allows you to create a budget that is truly sustainable. It helps you identify if your current lifestyle is aligned with your earnings or if you are consistently overspending, leading to debt accumulation. If your expenses consume nearly all your net income, it signals a need to adjust your lifestyle or increase your earning potential.

- Debt-to-Income Ratio (DTI): This crucial metric, calculated by dividing your total monthly debt payments by your gross monthly income, is heavily influenced by your annual earnings. A low DTI (typically below 36%) indicates good financial health and better chances for loan approvals, while a high DTI can signal financial strain and limits future borrowing capacity. Understanding your annual income allows you to proactively manage this ratio.

- Emergency Fund Adequacy: Financial experts often recommend having 3-6 months’ worth of living expenses saved in an emergency fund. Your annual income helps you determine this target amount, ensuring you have a buffer against unexpected life events like job loss or medical emergencies.

Strategizing for Savings, Investments, and Debt Management

With a clear picture of your annual income, you can implement more effective strategies for building wealth and reducing liabilities.

- Optimizing Savings: Knowing your income allows you to establish clear savings goals as a percentage of your earnings. For instance, if you aim to save 15% of your gross annual income, the calculation becomes straightforward. This clarity encourages consistent contributions to retirement accounts, investment portfolios, and short-term savings goals.

- Informed Investment Decisions: Your annual income, particularly your disposable income, dictates how much you can comfortably allocate to investments. It helps you assess your risk tolerance based on your financial cushion and decide on appropriate asset allocations. Furthermore, higher incomes can sometimes unlock access to certain investment opportunities or provide more flexibility in managing investment-related tax implications.

- Accelerated Debt Repayment: If you have consumer debt (credit cards, personal loans), your annual income determines how aggressively you can tackle it. By knowing your surplus income, you can allocate extra funds towards high-interest debts, reducing interest payments and shortening the repayment period. This also applies to managing student loan payments or planning for mortgage principal reductions.

Benchmarking for Career Growth and Income Optimization

Your annual income isn’t just a static number; it’s a dynamic indicator that can guide your professional trajectory and income-generating strategies.

- Salary Negotiation: Armed with an accurate understanding of your current annual income, and ideally, comparative industry data, you are in a stronger position to negotiate raises or new job offers. You know your worth and can articulate your salary expectations with confidence, preventing you from being underpaid.

- Identifying Income Gaps: By comparing your annual income to industry averages for your role, experience level, and geographic location, you can identify if you are earning below market rate. This insight can fuel discussions with your employer or prompt a job search for better-paying opportunities.

- Exploring Side Hustles and New Ventures: If your current annual income doesn’t meet your financial goals or lifestyle aspirations, it can serve as a powerful motivator to explore additional income streams. Whether it’s freelancing, starting a small business, or investing in passive income ventures, knowing your current baseline helps you determine how much extra income you need to generate.

- Career Planning: Over the long term, tracking your annual income provides a performance metric for your career. Are you progressing financially year over year? Is your income growth keeping pace with inflation or your increasing responsibilities? These insights are crucial for strategic career planning and professional development.

In conclusion, an “annual income calculator” is far more than a simple numerical tool. It’s a foundational element of financial literacy, offering unparalleled clarity into your economic standing. By meticulously calculating and understanding your annual earnings, you gain the power to budget wisely, save effectively, invest strategically, manage debt responsibly, and make informed decisions that pave the way for a secure and prosperous financial future. It transforms abstract financial concepts into actionable insights, empowering you to take control of your monetary destiny. Start calculating today, and unlock the full potential of your earnings.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.