Purchasing a vehicle is one of the most significant financial commitments the average consumer will make, second only to buying a home. However, the emotional allure of a sleek new car often overshadows the cold, hard mathematics of personal finance. Many buyers find themselves “car poor”—spending such a high percentage of their income on auto payments that they sacrifice their ability to save for retirement, build an emergency fund, or enjoy other life experiences.

Determining how much you can truly afford for an automobile requires a shift in perspective. It is not merely about whether you can clear the monthly payment hurdle; it is about how that vehicle fits into your broader financial ecosystem. In this guide, we will analyze the metrics of auto affordability, the hidden costs of ownership, and the strategic financing moves that protect your long-term wealth.

Understanding the Fundamentals of Auto Affordability

Before stepping onto a dealership lot or browsing online marketplaces, you must establish a baseline for what constitutes a “safe” expenditure. Financial experts often look toward standardized ratios to prevent buyers from overextending themselves.

The 20/4/10 Rule

The gold standard in personal finance for vehicle purchasing is the 20/4/10 rule. This framework provides a disciplined approach to budgeting:

- 20% Down Payment: You should aim to put at least 20% down. This protects you from “negative equity” (being underwater on your loan), as cars depreciate rapidly the moment they are driven off the lot.

- 4-Year Loan Term: While 72-month or even 84-month loans are becoming common, they are a trap. A 48-month (4-year) term ensures you pay less in interest and own the asset outright while it still has significant value.

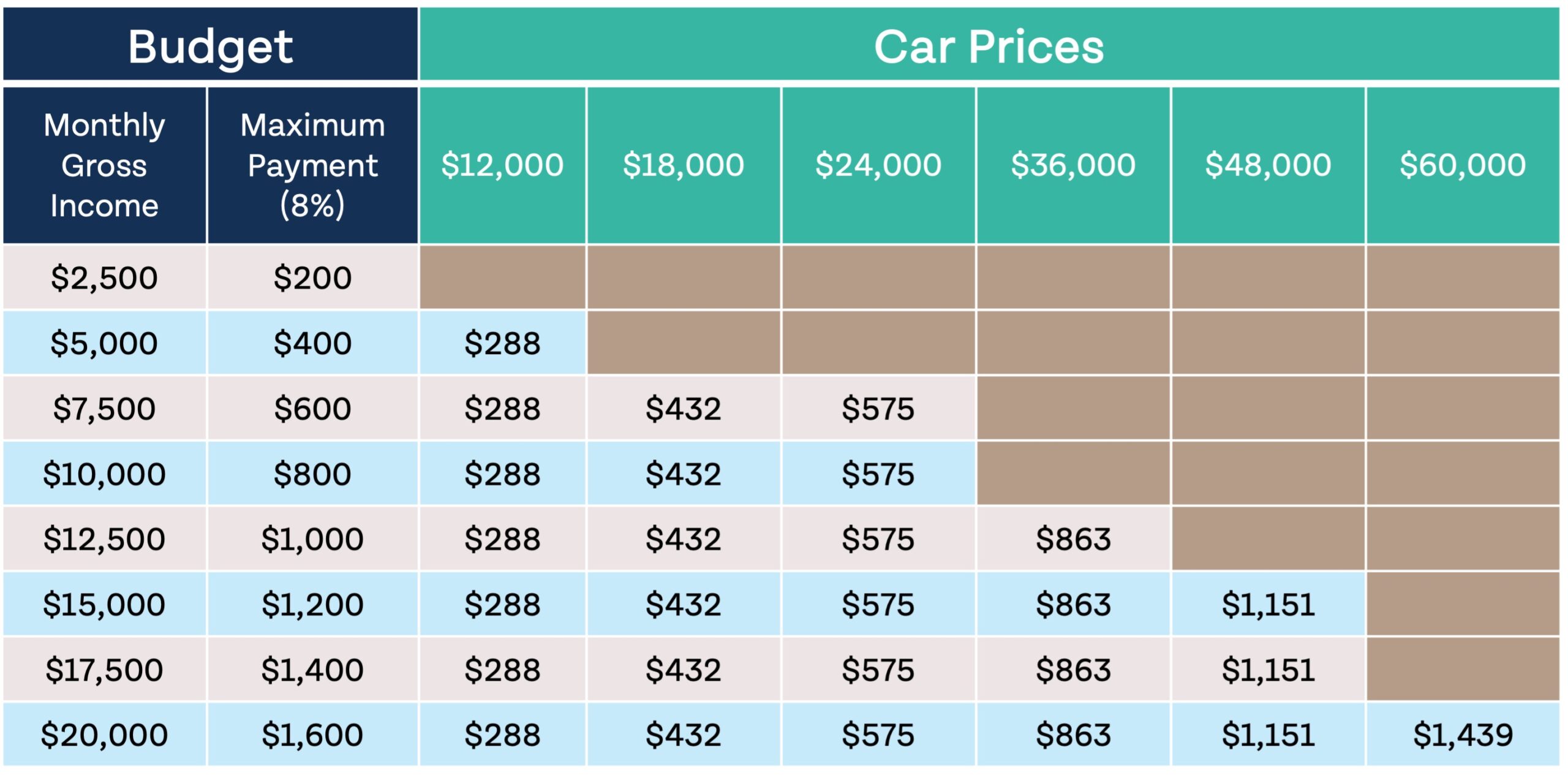

- 10% of Monthly Income: Your total transportation costs—including the loan payment, insurance, and maintenance—should not exceed 10% of your gross monthly income.

Beyond the Sticker Price: The True Cost of Ownership

The “affordability” of a car is frequently misunderstood as the “monthly payment.” This is a dangerous simplification. The True Cost of Ownership (TCO) includes several variables that do not appear on the window sticker. These include fuel, insurance premiums (which vary wildly based on the vehicle model), registration fees, and scheduled maintenance. For example, a luxury European sedan might have a similar monthly payment to a domestic truck, but the cost of oil changes, specialized tires, and premium fuel can make the sedan significantly more expensive over a five-year period.

Evaluating Your Financial Health Before the Purchase

A car loan does not exist in a vacuum. It interacts with your existing debts and your future credit capacity. To determine affordability, you must look at your balance sheet through the eyes of a lender while maintaining the skepticism of a savvy investor.

Debt-to-Income (DTI) Ratios and Auto Loans

Lenders use the Debt-to-Income (DTI) ratio to determine your creditworthiness. This is the percentage of your gross monthly income that goes toward paying debts (rent/mortgage, student loans, credit cards). If a new auto loan pushes your DTI above 36% to 43%, you may find it difficult to qualify for other financing, such as a mortgage, in the near future. Even if a lender approves a high-DTI loan, it is often at a predatory interest rate that compromises your financial stability.

The Impact of Credit Scores on Interest Rates

In the world of personal finance, your credit score is your most valuable currency. A difference of 100 points on your FICO score can translate to thousands of dollars in interest over the life of a loan. Buyers in the “prime” or “super-prime” categories (720+) often qualify for promotional 0% to 3% APRs. Conversely, “subprime” buyers may face rates of 15% or higher. Before deciding on a budget, pull your credit report. If your score is low, it may be financially wiser to delay the purchase by six months to improve your score, potentially saving you $50 to $100 every month in interest alone.

Financing Strategies for Long-Term Wealth

The way you structure your auto loan can either be a bridge to a better lifestyle or a weight that drags down your net worth. Strategic financing is about minimizing the cost of capital.

Down Payments: Why 20% Still Matters

In an era of “zero down” offers, the 20% down payment feels like an antique concept. However, from a wealth-building perspective, it is vital. A substantial down payment reduces the principal balance, which in turn reduces the total interest paid. More importantly, it provides a “buffer” against depreciation. If you need to sell the car unexpectedly due to a job loss or emergency, having 20% equity ensures you can sell the vehicle for more than you owe, rather than having to pay the bank to take the car away.

Loan Terms: The Trap of Long-Term Financing

Dealerships often focus on the monthly payment to distract buyers from the total cost of the loan. By stretching a loan to 72 or 84 months, they can make an expensive SUV “feel” affordable. However, these long-term loans are a primary driver of financial instability. Not only do you pay significantly more in interest, but you also risk being “upside down” for almost the entire duration of the loan. By the time the car is paid off, its maintenance costs may be rising sharply, leaving you with no period of “payment-free” driving to replenish your savings.

Practical Tools and Calculations for Car Buyers

To move from theory to practice, you need to run the numbers using a realistic framework. This involves looking at your cash flow and your “sinking funds.”

Calculating Your Monthly Payment Ceiling

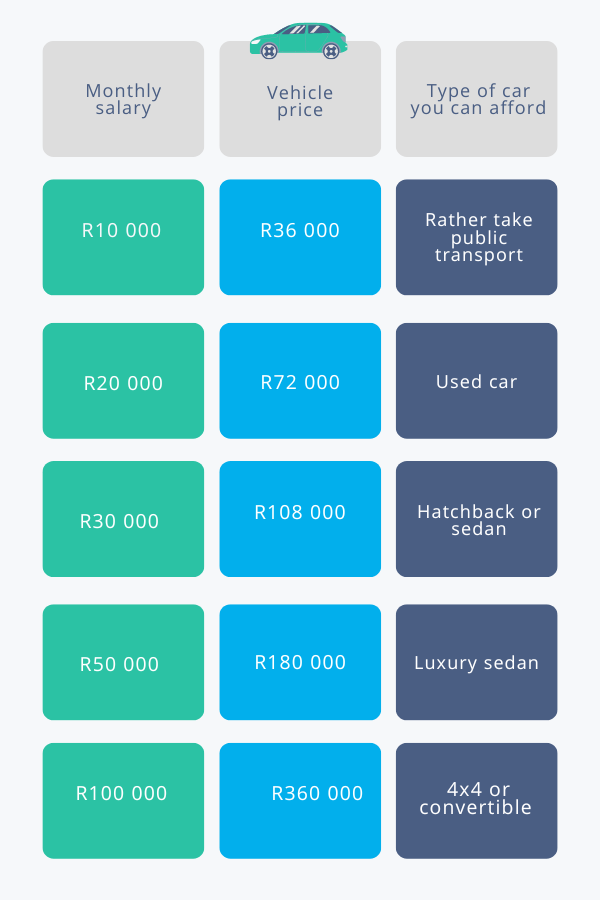

To find your ceiling, start with your take-home pay. Subtract your essential expenses (housing, food, utilities) and your mandatory savings (retirement and emergency fund). What remains is your discretionary income. If your “10% of gross income” calculation for the car exceeds 50% of your remaining discretionary income, you are likely overspending. A car is a depreciating asset; it should never starve your appreciating assets (like stocks or real estate).

Factor in Maintenance, Insurance, and Fuel

A smart financial plan includes a “sinking fund” for vehicle maintenance. For a new car, this might be $50 a month; for an older, used vehicle, it could be $150. Furthermore, call your insurance provider before buying. Providing them with the VIN of the vehicle you are considering can reveal surprising cost spikes. Some vehicles are more prone to theft or have higher repair costs for their sensors and safety systems, leading to higher premiums that could break your budget.

Making the Final Decision: New, Used, or Lease?

The final step in determining affordability is choosing the right vehicle “type” for your financial stage. Each has a different impact on your balance sheet.

The Depreciation Factor

The biggest “hidden” cost in auto finance is depreciation. A new car typically loses 20% of its value in the first year and roughly 60% after five years. From a pure money-management standpoint, buying a 2- to 3-year-old “certified pre-owned” (CPO) vehicle is often the most efficient choice. You allow the first owner to take the massive hit on depreciation while you receive a vehicle that is still under warranty and has modern safety features.

When Leasing Makes Financial Sense

Leasing is often criticized in personal finance circles because you don’t build equity. However, for business owners who can utilize tax deductions, or for individuals who prioritize predictable monthly costs and always want to be under warranty, leasing can be a structured expense. The key is to recognize that leasing is a lifestyle choice, not an investment. If your goal is to maximize your net worth, buying a reliable used vehicle and driving it for a decade is the statistically superior path.

In conclusion, “how much you can afford” is not a question for the car salesperson; it is a question for your budget. By adhering to the 20/4/10 rule, accounting for the total cost of ownership, and resisting the temptation of long-term debt, you ensure that your vehicle is a tool for mobility rather than a barrier to your financial freedom. Investing the time to run these numbers today will pay dividends in the form of reduced stress and increased wealth for years to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.