Understanding how your Social Security benefit is calculated is one of the most crucial elements of retirement planning. For many Americans, Social Security represents a foundational pillar of their financial security in their later years. Yet, the precise mechanisms that dictate the monthly amount received can often seem opaque and complex. It’s not a one-size-fits-all figure; rather, it’s a personalized calculation rooted deeply in your lifetime earnings history, age at claiming, and several other factors.

Dispelling the mystery behind these calculations empowers individuals to make informed decisions about their working careers, savings, and when to claim their benefits. This article will demystify the process, breaking down the core components the Social Security Administration (SSA) uses to arrive at your Primary Insurance Amount (PIA) and how various adjustments can influence your final monthly payment.

The Foundation: Understanding Your Earnings Record

The bedrock of your Social Security benefit calculation is your earnings history. The SSA meticulously tracks your earnings throughout your working life, and these records are central to determining your eventual benefit. However, not all earnings are treated equally, and only earnings up to a certain annual limit are subject to Social Security taxes and, consequently, factored into your benefit calculation.

The Importance of Indexed Earnings

One of the most critical concepts in understanding your earnings record is “indexing.” Social Security doesn’t simply use your raw historical earnings. To account for changes in general wage levels over time, the SSA indexes your past earnings to reflect their current value. This process ensures that benefits paid to today’s retirees reflect the general increase in wages that occurred during their working careers, rather than simply relying on nominal dollar amounts earned decades ago.

For example, $10,000 earned in 1980 had a significantly higher purchasing power than $10,000 earned today. Indexing adjusts those 1980 earnings upwards to an equivalent value in a more recent year (typically two years before your entitlement to benefits begins), thereby protecting your past contributions from inflation. This indexing typically applies up to age 60; earnings after that age are generally counted at their nominal value.

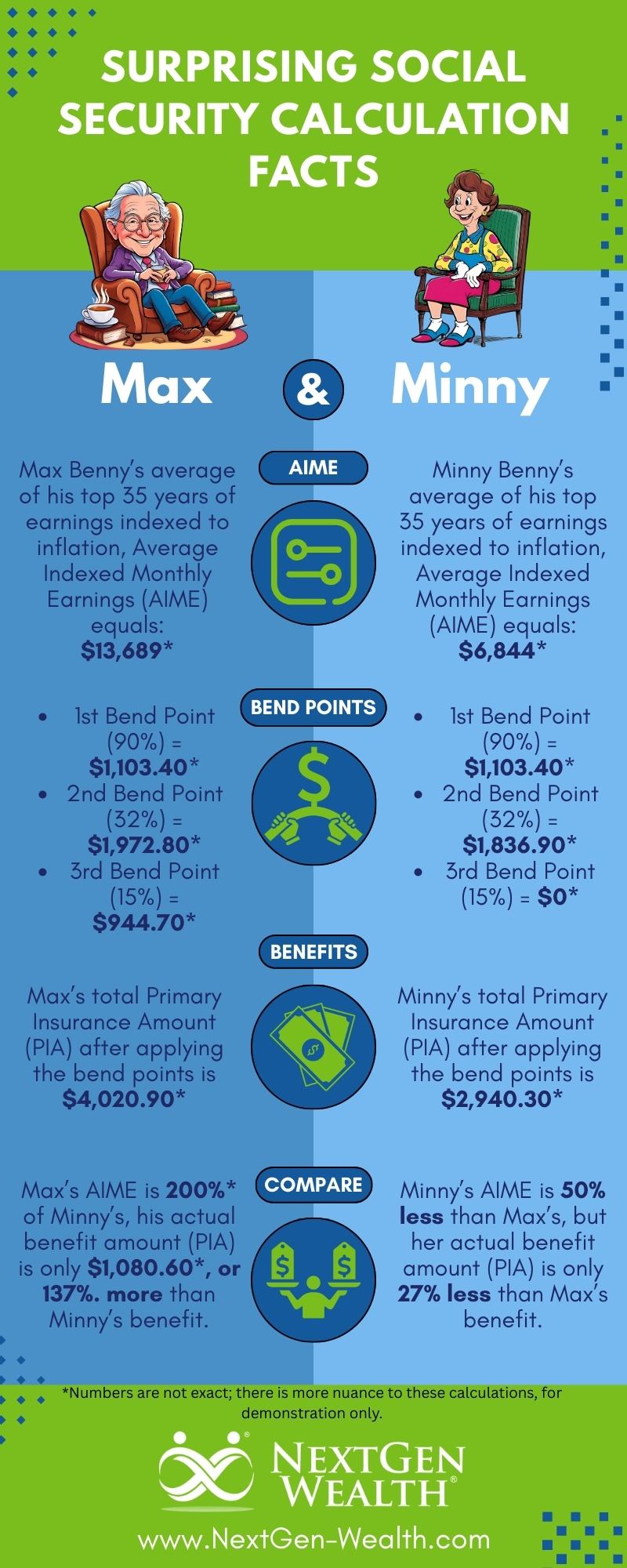

Calculating Your Average Indexed Monthly Earnings (AIME)

Once your annual earnings have been indexed, the SSA proceeds to calculate your Average Indexed Monthly Earnings (AIME). This is a pivotal step. The SSA reviews your entire indexed earnings record, identifying the 35 years during which you earned the most. It then sums the indexed earnings from these 35 highest-earning years. If you have fewer than 35 years of earnings, the calculation will include years with zero earnings, which can significantly lower your AIME.

After identifying the top 35 years and summing their indexed earnings, this total is divided by 420 (the number of months in 35 years). The result is your AIME. This AIME figure is the primary input for the next critical stage of the calculation: determining your Primary Insurance Amount.

From AIME to Primary Insurance Amount (PIA)

Your Primary Insurance Amount (PIA) is the monthly benefit you are entitled to receive if you claim Social Security benefits precisely at your full retirement age (FRA). It is the amount from which all other benefit amounts are derived, whether you claim early, late, or are entitled to spousal or survivor benefits. The PIA is not a simple percentage of your AIME; instead, it uses a progressive formula designed to replace a higher percentage of earnings for lower-income workers.

The Bend Points Formula

The SSA uses a progressive formula involving “bend points” to convert your AIME into your PIA. Bend points are specific dollar amounts in the AIME formula that separate different earning tiers, each with a different benefit accrual rate. These bend points are adjusted annually to reflect changes in the national average wage index.

For an individual who turns 62 in 2024, for example, the PIA formula might look something like this (actual bend points vary by year):

- 90% of the first $1,174 of AIME

- 32% of AIME over $1,174 up to $7,078

- 15% of AIME over $7,078

The “90%” tier is for relatively low earners, providing a significant replacement rate for their income. The “32%” tier applies to middle-income earners, and the “15%” tier applies to higher earners. This progressive structure means that Social Security replaces a larger proportion of pre-retirement earnings for lower-income individuals than it does for higher-income individuals, although higher earners still receive a larger absolute dollar amount.

What is Your Primary Insurance Amount (PIA)?

By applying your calculated AIME to the bend point formula for the year you turn 62 (or the year you become eligible for benefits), the SSA determines your PIA. This PIA is the basis for your future benefit. If you claim at your full retirement age, your monthly payment will be equal to your PIA, plus any cost-of-living adjustments that have occurred since you turned 62.

It’s crucial to understand that the PIA is a fixed amount determined once you become eligible for benefits, though it will be adjusted upwards by Cost-of-Living Adjustments (COLAs) in subsequent years. All decisions you make regarding when to start receiving benefits will then be applied to this PIA.

Factors Influencing Your Final Benefit Amount

While the PIA sets the baseline, several critical factors can significantly alter the actual monthly benefit you receive. These adjustments can either increase or decrease your payment from your PIA.

The Critical Role of Claiming Age

The age at which you decide to start receiving Social Security benefits is perhaps the most impactful decision affecting your monthly payment.

- Full Retirement Age (FRA): This is the age at which you are entitled to 100% of your PIA. FRA varies based on your birth year, ranging from 66 for those born between 1943 and 1954, gradually increasing to 67 for those born in 1960 or later.

- Claiming Early: You can start receiving benefits as early as age 62. However, claiming before your FRA results in a permanent reduction in your monthly benefit. The reduction is approximately 5/9 of 1% for each month before FRA, up to 36 months, and 5/12 of 1% for each month beyond 36 months. For someone with an FRA of 67, claiming at 62 means a permanent reduction of about 30%.

- Claiming Late: Conversely, delaying benefits beyond your FRA can result in a significant increase. For each month you delay past your FRA, up to age 70, you earn delayed retirement credits. These credits increase your monthly benefit by approximately 2/3 of 1% per month (or 8% per year). Delaying until age 70 for someone with an FRA of 67 could result in a 24% increase over their PIA.

This trade-off between receiving benefits sooner (but at a reduced rate) or later (but at an increased rate) is a key strategic decision influenced by personal health, financial needs, and longevity expectations.

The Impact of Continued Work While Receiving Benefits

If you claim Social Security benefits before your full retirement age and continue to work, your benefits may be temporarily reduced if your earnings exceed certain annual limits. This is known as the “earnings test.”

- Before FRA: If you are under your FRA, the SSA will deduct $1 from your benefits for every $2 you earn above a specific annual limit (e.g., $22,320 in 2024).

- In the Year You Reach FRA: In the year you reach your FRA, a higher earnings limit applies, and the SSA will deduct $1 for every $3 you earn above that limit (e.g., $59,520 in 2024), but only for earnings before the month you reach FRA.

- At or After FRA: Once you reach your full retirement age, the earnings test no longer applies, and you can earn any amount without your Social Security benefits being reduced.

Any benefits withheld due to the earnings test are not permanently lost; they are factored back into your benefit calculation at your FRA, leading to a slightly higher monthly payment.

Cost-of-Living Adjustments (COLAs)

Once you begin receiving benefits, your monthly payment is subject to annual Cost-of-Living Adjustments (COLAs). These adjustments are designed to help Social Security benefits keep pace with inflation. COLAs are typically announced in October and take effect in December (reflected in January payments). The percentage increase is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). While COLAs aim to preserve purchasing power, they don’t always perfectly match individual inflation experiences.

Adjustments for Government Pension Offset (GPO) and Windfall Elimination Provision (WEP)

Two provisions, the Government Pension Offset (GPO) and the Windfall Elimination Provision (WEP), can significantly reduce Social Security benefits for individuals who also receive a pension from employment not covered by Social Security (e.g., some government jobs).

- Government Pension Offset (GPO): Affects spouses or surviving spouses who receive a pension from non-covered government employment. Their Social Security spousal or survivor benefits will be reduced by two-thirds of their non-covered pension amount.

- Windfall Elimination Provision (WEP): Affects individuals who receive a pension from non-covered employment and also have enough earnings in covered employment to qualify for their own Social Security retirement benefit. The WEP modifies the PIA formula, replacing the 90% factor for the lowest AIME tier with a lower percentage (e.g., 40%) to reduce the perceived “windfall” for those who benefit from both a non-covered pension and Social Security.

These provisions are complex and can drastically alter expected benefits, making it crucial for affected individuals to understand their implications.

Maximizing Your Social Security Benefits

Given the various factors at play, a proactive approach to understanding and planning for Social Security can help maximize your lifetime benefits.

Strategic Claiming Decisions

The decision of when to claim benefits is highly personal and multifaceted. While delaying until age 70 often provides the highest monthly payment, it requires a robust financial plan to cover expenses during the delay period. Factors to consider include:

- Personal Health and Longevity: If you anticipate a long lifespan, delayed claiming might offer greater lifetime benefits. If health issues suggest a shorter lifespan, earlier claiming might be advantageous.

- Current Financial Needs: Can you afford to delay benefits without drawing down retirement savings too aggressively?

- Spousal Benefits: For married couples, strategic claiming can maximize combined lifetime benefits. Often, the higher earner delays, while the lower earner claims earlier.

- Other Income Sources: The availability of pensions, 401(k)s, IRAs, and other investments can influence the optimal claiming age.

Financial advisors specializing in retirement planning can provide personalized guidance to navigate these complex decisions.

Ensuring Your Earnings Record is Accurate

Periodically reviewing your Social Security earnings record is a critical, yet often overlooked, step. Mistakes can happen, and missing or incorrect earnings entries can negatively impact your future AIME and, consequently, your PIA.

- Create an Account: You can create a “my Social Security” account online at ssa.gov to access your earnings record, review your estimated benefits, and track your progress toward retirement.

- Verify Accuracy: Compare the earnings listed on your Social Security statement with your W-2s or tax returns. Report any discrepancies to the SSA promptly, as there are time limits for correcting errors.

Beyond the Basics: Important Considerations

A comprehensive understanding of Social Security extends beyond just the benefit calculation.

Maximum and Minimum Benefits

While Social Security aims to provide a safety net, there are both maximum and minimum benefit amounts.

- Maximum Benefit: There is an annual earnings limit subject to Social Security taxes, which means there’s also an upper limit to the AIME and, consequently, the maximum PIA. For someone claiming at FRA in 2024, the maximum monthly benefit is approximately $3,822. This requires consistent high earnings over 35 years at or above the taxable maximum.

- Minimum Benefit: While there isn’t a traditional “minimum Social Security benefit” in the sense of a fixed amount, the progressive bend point formula ensures that even individuals with very low career earnings still receive a benefit that replaces a higher percentage of those earnings, providing a basic level of support. There used to be a special minimum benefit for long-term low earners, but this has largely been superseded by the current PIA calculation.

Taxation of Social Security Benefits

It’s important to remember that Social Security benefits can be subject to federal income tax, and in some states, to state income tax as well.

- Federal Taxation: If your “combined income” (Adjusted Gross Income + nontaxable interest + one-half of your Social Security benefits) exceeds certain thresholds, a portion of your benefits (up to 85%) may be taxable. These thresholds are not indexed for inflation, meaning more retirees find their benefits subject to tax over time.

- State Taxation: Several states also tax Social Security benefits, though many exempt them or offer specific deductions. It’s essential to understand the tax laws in your state of residence.

Conclusion

The determination of your Social Security benefit amount is a sophisticated process, weaving together your lifetime earnings, economic indexing, and specific age-related decisions into a personalized financial outcome. From the calculation of your Average Indexed Monthly Earnings (AIME) and the application of bend points to arrive at your Primary Insurance Amount (PIA), to the critical adjustments based on claiming age, continued work, and specialized provisions, each step plays a vital role.

By understanding these intricacies, individuals can move beyond simply hoping for the best and instead strategically plan for their retirement. Regularly checking your earnings record, carefully considering your claiming age, and factoring in potential tax implications are not merely administrative tasks but essential components of robust financial planning. Social Security remains a cornerstone of retirement for millions; knowledge of its mechanics is the first step toward optimizing its significant financial contribution to your golden years.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.