Understanding how interest is calculated is a fundamental skill for anyone navigating the world of personal finance, from managing savings accounts to taking out loans. It’s the engine that drives both the growth of your wealth and the cost of borrowing. While the concept might seem straightforward – a percentage of the principal amount – the nuances of calculation can significantly impact financial outcomes over time. This article delves into the core principles of interest calculation, exploring the common methods, key variables, and practical implications for your financial journey.

The Building Blocks of Interest Calculation

At its heart, interest is the cost of borrowing money or the reward for lending it. When you deposit money into a savings account or an investment, the financial institution pays you interest for the use of your funds. Conversely, when you take out a loan, whether it’s a mortgage, a car loan, or a credit card, you pay interest to the lender for the privilege of using their money. The calculation hinges on several key components:

Principal: The Foundation of Your Calculation

The principal is the initial amount of money borrowed or invested. For a loan, it’s the total sum you receive. For a savings account, it’s the initial deposit. The principal is the base upon which interest is calculated. Any changes to the principal, such as additional deposits, withdrawals, or loan repayments, will directly affect the subsequent interest calculations.

- Loan Principal: When you take out a $20,000 car loan, $20,000 is the principal. Each payment you make will first go towards paying off the accrued interest, and then the remainder will reduce the principal balance.

- Investment Principal: If you invest $5,000 in a mutual fund, $5,000 is your principal. This is the amount that will earn returns, which are akin to interest in this context.

- Savings Account Principal: Depositing $1,000 into a high-yield savings account makes $1,000 your principal. This amount, along with any accrued interest, will grow over time.

Interest Rate: The Percentage of Growth or Cost

The interest rate, usually expressed as an annual percentage (APR), is the most crucial factor determining how much interest you’ll earn or pay. It represents the cost of borrowing or the return on investment over a specific period, typically one year. Interest rates can vary widely based on the type of financial product, the lender, your creditworthiness, and prevailing economic conditions.

- Nominal vs. Effective Interest Rate: It’s important to distinguish between the nominal interest rate and the effective interest rate. The nominal rate is the stated annual rate. The effective annual rate (EAR) accounts for the effect of compounding, meaning it reflects the total amount of interest earned or paid over a year when interest is compounded more than once a year. The EAR will always be slightly higher than the nominal rate if compounding occurs more frequently than annually.

- Factors Influencing Interest Rates: For lenders, interest rates are influenced by factors such as the risk associated with the borrower (credit score), the term of the loan, and the overall economic environment (inflation, central bank policies). For borrowers, a higher interest rate means a higher cost of borrowing, while for investors, a higher rate means a greater potential return.

Time Period: The Duration of the Financial Relationship

The length of time over which interest is calculated is another critical component. The longer money is borrowed or invested, the more interest will accumulate. This is where the power of compounding truly becomes apparent. Interest is typically calculated over specific periods, such as daily, monthly, or annually, depending on the terms of the financial agreement.

- Loan Terms: A 30-year mortgage will accrue significantly more interest than a 5-year car loan, even with the same principal and interest rate, simply due to the extended duration.

- Investment Horizons: An investment held for 20 years has a much greater potential to grow through compounding than one held for only two years.

Types of Interest Calculations: Simple vs. Compound

The fundamental difference in how interest is calculated boils down to two primary methods: simple interest and compound interest. While both are based on the principal, interest rate, and time, their implications for financial growth and cost are vastly different.

Simple Interest: The Straightforward Approach

Simple interest is calculated only on the initial principal amount. This means that the interest earned or paid in each period remains constant, regardless of whether previous interest has been added back to the principal. It’s a straightforward calculation, often used for short-term loans or basic interest scenarios.

Formula for Simple Interest:

Simple Interest (SI) = Principal (P) × Rate (R) × Time (T)

Where:

- P = Principal amount

- R = Annual interest rate (expressed as a decimal)

- T = Time period in years

Example:

Suppose you invest $1,000 at an annual simple interest rate of 5% for 3 years.

- SI = $1,000 × 0.05 × 3 = $150

- The total amount after 3 years would be $1,000 (principal) + $150 (interest) = $1,150.

Simple interest is easy to understand and calculate, but it doesn’t reflect the true earning potential of money over longer periods because it doesn’t account for the snowball effect of earning interest on previously earned interest.

Compound Interest: The Snowball Effect

Compound interest, often referred to as “interest on interest,” is calculated on the initial principal amount and also on the accumulated interest from previous periods. This means that the interest earned in one period is added to the principal, and in the next period, interest is calculated on this new, larger sum. This compounding effect can dramatically accelerate the growth of investments and significantly increase the cost of loans over time.

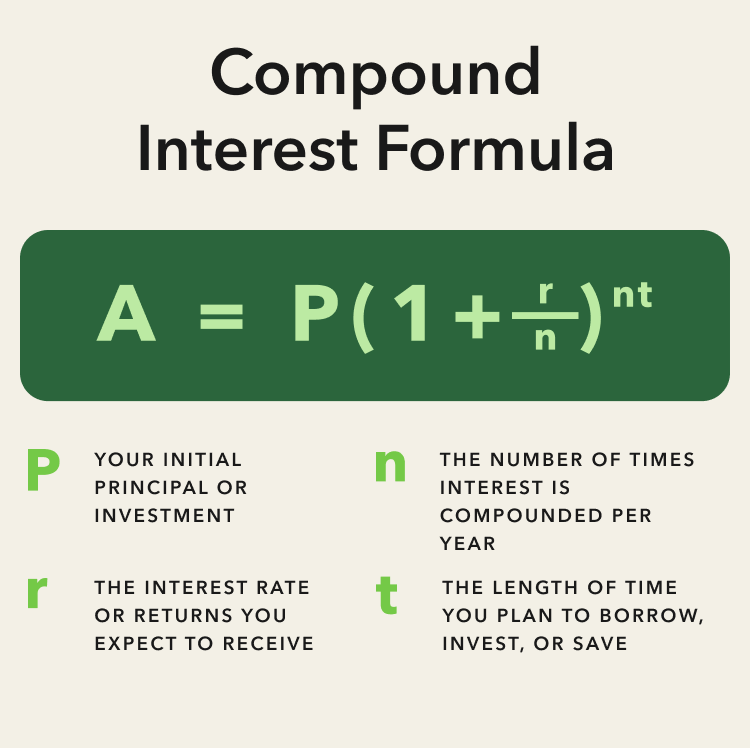

Formula for Compound Interest:

Future Value (FV) = P (1 + R/n)^(nt)

Where:

- FV = Future Value of the investment/loan, including interest

- P = Principal amount

- R = Annual interest rate (expressed as a decimal)

- n = Number of times that interest is compounded per year

- t = Number of years the money is invested or borrowed for

Example:

Let’s use the same scenario: investing $1,000 at an annual interest rate of 5% for 3 years, but this time with annual compounding.

- Year 1:

- Interest = $1,000 × 0.05 = $50

- Balance = $1,000 + $50 = $1,050

- Year 2:

- Interest = $1,050 × 0.05 = $52.50

- Balance = $1,050 + $52.50 = $1,102.50

- Year 3:

- Interest = $1,102.50 × 0.05 = $55.13 (rounded)

- Balance = $1,102.50 + $55.13 = $1,157.63

Using the compound interest formula:

- FV = $1,000 (1 + 0.05/1)^(1*3) = $1,000 (1.05)^3 = $1,157.63

As you can see, the compound interest calculation resulted in a higher final amount ($1,157.63) compared to simple interest ($1,150). The difference of $7.63 might seem small in this short example, but over longer periods and with higher interest rates, the divergence becomes substantial.

The Impact of Compounding Frequency

The frequency with which interest is compounded has a significant impact on the final outcome. Interest can be compounded daily, monthly, quarterly, semi-annually, or annually. The more frequently interest is compounded, the faster your money will grow (or the more you’ll pay on a loan).

- Daily Compounding: This is the most frequent compounding period offered by many financial institutions for savings accounts and some loans. It means interest is calculated and added to the principal every single day.

- Monthly Compounding: Common for many loans, including mortgages and personal loans, as well as some savings accounts.

- Quarterly/Semi-Annual Compounding: Often seen in bonds or certificates of deposit (CDs).

- Annual Compounding: The simplest form, where interest is calculated and added only once a year.

Consider the earlier example of $1,000 at 5% for 3 years.

- Annual compounding: $1,157.63

- Monthly compounding: Using the formula FV = $1,000 (1 + 0.05/12)^(12*3) ≈ $1,161.47. The extra $3.84 comes from earning interest on the monthly accrued interest.

This demonstrates that even small differences in compounding frequency can lead to meaningful financial gains or costs over time.

Practical Applications of Interest Calculation

The principles of interest calculation are not just theoretical; they have direct and profound implications for your personal finances. Understanding these calculations empowers you to make informed decisions about saving, borrowing, and investing.

Savings and Investments: Growing Your Wealth

For savers and investors, compound interest is your most powerful ally. The longer your money is invested and the higher the interest rate, the more substantial your returns will be.

- High-Yield Savings Accounts: These accounts offer higher interest rates than traditional savings accounts, making your money grow faster. Understanding the interest rate and compounding frequency helps you choose the best account for your needs.

- Certificates of Deposit (CDs): CDs typically offer a fixed interest rate for a specific term. Knowing how interest is calculated helps you compare different CD offerings and estimate your earnings.

- Retirement Accounts (401(k), IRA): These long-term investment vehicles benefit immensely from compounding. Even modest contributions, when invested consistently and allowed to grow over decades, can result in significant wealth due to the power of compound interest.

- Stocks and Bonds: While not strictly interest in the same way as a bank account, the returns from these investments are often calculated and reinvested, leading to a compounding effect on your overall portfolio value.

Loans and Debt: Managing Your Obligations

On the flip side, interest is the cost of borrowing, and understanding how it’s calculated is crucial for managing debt effectively.

- Mortgages: The interest on a mortgage is typically calculated on the outstanding principal balance. A small reduction in the interest rate or making extra principal payments can save you tens or even hundreds of thousands of dollars in interest over the life of the loan.

- Credit Cards: Credit card interest rates are notoriously high. Understanding how interest is compounded daily on your outstanding balance, especially if you only make minimum payments, can lead to a debt spiral where you pay significantly more than you initially borrowed.

- Personal Loans and Auto Loans: These loans also accrue interest based on the principal, rate, and term. Comparing loan offers requires careful attention to the APR and how interest will be calculated.

Conclusion: Mastering Your Financial Future Through Interest Awareness

The ability to understand and calculate interest is not just an academic exercise; it’s a vital component of financial literacy. Whether you’re aiming to grow your savings, invest wisely, or manage debt responsibly, a firm grasp of simple and compound interest is indispensable. The key takeaways are clear: for growing your money, favor compound interest and long investment horizons. For borrowing, aim for lower interest rates and shorter terms, and prioritize paying down principal to minimize the cost of interest. By consistently applying these principles, you can harness the power of interest to build a more secure and prosperous financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.