Understanding how your Social Security benefit is calculated is a cornerstone of effective retirement planning. For many Americans, Social Security represents a significant portion of their guaranteed income in their golden years, acting as a vital safety net. Yet, the precise methodology behind these calculations often remains a mystery, shrouded in jargon and perceived complexity. Demystifying this process is not just an academic exercise; it empowers individuals to make informed decisions about their claiming age, retirement savings, and overall financial future.

This article aims to unravel the intricacies of Social Security benefit calculation, breaking down the key components that determine your monthly payment. From your lifetime earnings history to the crucial impact of your claiming age, we’ll explore the mechanisms the Social Security Administration (SSA) employs to arrive at your Primary Insurance Amount (PIA) and, ultimately, your monthly benefit.

The Foundation: Your Lifetime Earnings Record

At its heart, Social Security is an earned benefit. Your eligibility and the size of your future payments are inextricably linked to your work history and the contributions you’ve made to the system through payroll taxes over your career. The SSA maintains a comprehensive record of your earnings, and this record forms the bedrock of all benefit calculations.

A Lifetime of Contributions

Every dollar you earn from employment or self-employment, up to an annual maximum known as the “taxable earnings limit” (which changes year to year), is subject to Social Security taxes. These taxes, deducted from your paycheck, are what fund the system and, in turn, build your individual earnings record. The SSA tracks these earnings year by year, and it is this detailed history that will eventually be used to determine your benefit. It’s crucial to understand that only earnings up to the taxable limit for each year are considered in the calculation. If you earned above this limit in a particular year, only the amount up to the limit is factored in.

Adjusting for Inflation: Averaged Indexed Monthly Earnings (AIME)

While your raw earnings record is the starting point, the SSA doesn’t simply sum up your nominal earnings over the decades. To ensure that your past earnings accurately reflect their purchasing power in today’s economy, a process called “wage indexing” is applied. This indexing adjusts your earnings from past years to account for changes in the national average wage level over time. Without indexing, earnings from, say, the 1980s would appear much lower in value compared to current wages, unfairly reducing your benefit.

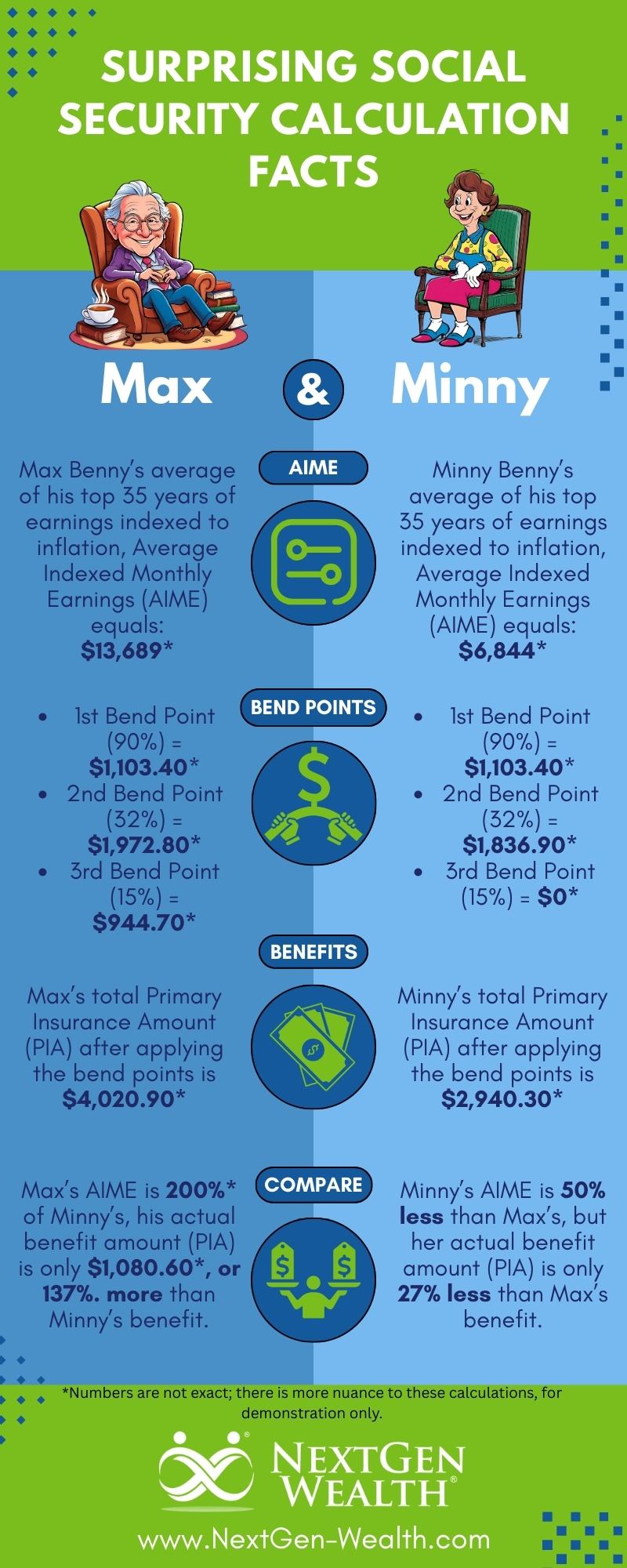

The SSA then identifies your 35 highest earning years after these wages have been indexed. These 35 years are then summed up, and that total is divided by 420 (the number of months in 35 years) to arrive at your Averaged Indexed Monthly Earnings (AIME). This AIME is the average of your top 35 years of indexed earnings, and it represents the average monthly income upon which your Social Security benefit will be primarily based. If you have fewer than 35 years of earnings, the missing years will be recorded as zero, which can significantly lower your AIME and, consequently, your benefit. This highlights the importance of a consistent work history.

The Core Formula: Primary Insurance Amount (PIA)

Once your AIME is established, the next critical step is to calculate your Primary Insurance Amount (PIA). Your PIA is the monthly benefit you are entitled to receive if you file for Social Security benefits precisely at your Full Retirement Age (FRA). It’s the benchmark figure from which all other benefit amounts (early, delayed, spousal, survivor) are derived.

Bending Points and Progressive Formula

The Social Security benefit formula is intentionally progressive, meaning it replaces a higher percentage of pre-retirement earnings for lower-income workers than for higher-income workers. This is achieved through a “three-tiered” system that uses what are known as “bending points.” The AIME is divided into three segments, and a different percentage is applied to each segment.

For example, for someone reaching age 62 in 2024:

- 90% of the first $1,174 of their AIME

- 32% of their AIME between $1,174 and $7,078

- 15% of their AIME above $7,078

(Note: These bending points are adjusted annually based on changes in the national average wage index.)

By applying higher percentages to the lower portions of AIME, the formula provides a more substantial safety net for those with lower lifetime earnings. The sum of these three calculations results in your PIA. It’s important to recognize that the PIA is a fixed amount for you, determined by your earnings and the year you reach age 62 (as this determines which bending points apply), before any adjustments for early or delayed claiming.

The Role of Full Retirement Age (FRA)

Your Full Retirement Age (FRA) is a pivotal concept in Social Security. It’s the age at which you are eligible to receive 100% of your calculated PIA. Your FRA depends on your birth year:

- Born 1943-1954: FRA is 66

- Born 1955: FRA is 66 and 2 months

- Born 1956: FRA is 66 and 4 months

- Born 1957: FRA is 66 and 6 months

- Born 1958: FRA is 66 and 8 months

- Born 1959: FRA is 66 and 10 months

- Born 1960 or later: FRA is 67

Knowing your FRA is critical because it’s the baseline against which all other claiming decisions are measured. Claiming before your FRA results in a permanently reduced benefit, while delaying past your FRA results in a permanently increased benefit.

Factors Modifying Your Monthly Benefit

While your PIA represents your full benefit at FRA, the actual monthly payment you receive can be significantly altered by several factors, most notably your claiming age. Understanding these adjustments is key to optimizing your Social Security income.

Claiming Age: Early vs. Delayed Retirement

The decision of when to start receiving your Social Security benefits is perhaps the most impactful choice you’ll make regarding your retirement income.

- Early Claiming (Age 62): You can start receiving Social Security benefits as early as age 62. However, claiming before your FRA results in a permanent reduction in your monthly benefit. The reduction is approximately 5/9 of 1% for each month you claim before FRA, up to 36 months, and 5/12 of 1% for each month beyond 36 months. For someone with an FRA of 67, claiming at age 62 would result in a permanent reduction of about 30% of their PIA. This reduction is designed to actuarially balance the fact that you will be receiving benefits for a longer period.

- Delayed Claiming (Up to Age 70): Conversely, you can choose to delay claiming your benefits past your FRA, up to age 70. For each month you delay past your FRA, your benefit amount increases by a certain percentage, known as Delayed Retirement Credits (DRCs). These credits typically add 2/3 of 1% (or 8% annually) to your monthly benefit for each year you delay. For someone with an FRA of 67, delaying until age 70 could result in a permanent increase of 24% (3 years x 8% per year) above their PIA. This strategy is often recommended for individuals who are healthy, have other income sources, and anticipate a long lifespan, as it maximizes their guaranteed income stream.

The choice between early and delayed claiming involves a careful consideration of your health, other retirement savings, immediate financial needs, and family longevity history.

Spousal and Survivor Benefits

Social Security isn’t just for primary earners; it also provides benefits for eligible family members based on a worker’s earnings record.

-

Spousal Benefits: A spouse can claim up to 50% of the primary earner’s PIA if they claim at their own FRA. If they claim earlier, their spousal benefit will also be reduced. Importantly, a spouse can only claim spousal benefits once the primary earner has filed for their own benefits. Divorced spouses may also be eligible if the marriage lasted at least 10 years, and other conditions are met.

-

Survivor Benefits: When a worker dies, certain family members may be eligible for survivor benefits. A surviving spouse, for instance, can receive 100% of the deceased worker’s benefit if they claim at their own FRA, or a reduced amount if they claim earlier (as early as age 60, or age 50 if disabled). Children under 18 (or 19 if still in high school) and disabled adult children may also be eligible for benefits.

Working While Receiving Benefits

If you claim Social Security benefits before your FRA and continue to work, your benefits may be temporarily reduced or withheld if your earnings exceed certain annual limits. This is known as the “earnings test.”

- Before FRA: If you are under your FRA, the SSA will withhold $1 in benefits for every $2 you earn above the annual earnings limit ($22,320 in 2024).

- In the year you reach FRA: In the year you reach FRA, the SSA will withhold $1 in benefits for every $3 you earn above a higher limit ($59,520 in 2024), but only counting earnings before the month you reach FRA.

- At or After FRA: Once you reach your FRA, the earnings test no longer applies, and you can earn any amount without it affecting your Social Security benefits.

It’s important to note that any benefits withheld due to the earnings test are not permanently lost. When you reach your FRA, your monthly benefit will be recalculated to account for the withheld amounts, effectively giving you credit for those past withholdings and potentially increasing your future payments.

Taxation of Benefits

While Social Security benefits are often seen as “tax-free,” a portion of them may be subject to federal income tax, depending on your “provisional income.” Provisional income is calculated as your adjusted gross income (AGI) + nontaxable interest + one-half of your Social Security benefits.

- Individual Filers: If your provisional income is between $25,000 and $34,000, up to 50% of your benefits may be taxable. If it’s over $34,000, up to 85% of your benefits may be taxable.

- Joint Filers: If your provisional income is between $32,000 and $44,000, up to 50% of your benefits may be taxable. If it’s over $44,000, up to 85% of your benefits may be taxable.

Some states also tax Social Security benefits, so it’s essential to check your state’s specific tax laws.

Understanding Your Statement and Planning for the Future

Navigating the complexities of Social Security is made significantly easier by leveraging the resources available from the SSA and incorporating this knowledge into your broader financial planning.

Accessing Your Social Security Statement

The single most important tool for understanding your personal Social Security outlook is your Social Security Statement. You can access it by creating an account on the SSA’s official website (ssa.gov). Your statement provides:

- Your complete earnings history, year by year, as reported to the SSA. It’s crucial to review this periodically to ensure its accuracy. Any discrepancies could impact your future benefits.

- Your estimated Social Security benefits at different claiming ages (early, full, and delayed retirement).

- Estimated benefits for disability and survivor benefits.

- An overview of your estimated contributions to Social Security and Medicare.

Regularly reviewing your statement allows you to track your progress, identify potential issues with your earnings record, and gain a clearer picture of your future retirement income.

Proactive Financial Planning

While Social Security provides a critical base for retirement, it’s rarely sufficient as the sole source of income. For most individuals, Social Security is designed to replace only about 40% of their pre-retirement earnings, a percentage that is lower for higher earners due to the progressive nature of the benefit formula.

Therefore, understanding how your benefit is calculated should serve as a catalyst for proactive and comprehensive financial planning. This includes:

- Saving and Investing: Building robust personal savings through 401(k)s, IRAs, and other investment vehicles is paramount.

- Developing a Claiming Strategy: Based on your individual circumstances, health, other income sources, and longevity expectations, carefully decide the optimal age to claim your Social Security benefits. This often involves modeling different scenarios.

- Factoring in Inflation and Healthcare: Remember that healthcare costs in retirement can be substantial, and inflation will erode the purchasing power of your fixed benefits over time.

By treating Social Security as a foundational component of your retirement income, rather than the entirety, you position yourself for greater financial security and peace of mind in your later years.

Conclusion

The calculation of Social Security benefits, while seemingly intricate, follows a logical and predictable path rooted in your lifetime earnings. From the indexing of your wages to derive your Averaged Indexed Monthly Earnings (AIME), through the progressive Primary Insurance Amount (PIA) formula, and finally to the critical adjustments based on your claiming age, each step plays a vital role.

Understanding these mechanics empowers you to move beyond uncertainty and make strategic decisions that can significantly impact your financial well-being in retirement. Regularly checking your Social Security statement and engaging in thoughtful financial planning, integrating your projected benefits with personal savings, are crucial steps towards securing a comfortable and stable future. Social Security remains a powerful and essential program, and a clear grasp of its workings is an invaluable asset for every individual planning for retirement.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.