Paying taxes is an unavoidable aspect of financial life for individuals and businesses alike, forming the bedrock of modern economies. While often perceived as a complex and burdensome obligation, understanding the fundamental mechanisms of taxation can demystify the process and empower taxpayers to navigate their responsibilities effectively. At its core, paying taxes is the mandatory financial contribution levied by governments on income, property, goods, services, and other economic activities to fund public expenditures.

The Foundation of Taxation: Why We Pay

The concept of taxation dates back millennia, evolving from simple tributes to intricate systems designed to support diverse societal needs. Governments, whether local, state, or federal, rely on tax revenue to operate and provide a vast array of services essential for collective well-being and economic stability.

Government Services and Infrastructure

A significant portion of tax revenue is allocated to public services that benefit everyone. This includes critical infrastructure projects like roads, bridges, public transportation, and utilities. Taxes also fund national defense, law enforcement, fire protection, and emergency services, ensuring safety and order. Education systems, from public schools to state universities, are heavily subsidized by taxpayer dollars, fostering an educated workforce and informed citizenry. Public health initiatives, research, and healthcare programs also draw from this pool, aiming to improve national health outcomes. Without taxes, the scale and quality of these essential services would be severely diminished, impacting daily life and economic productivity.

Wealth Redistribution and Social Programs

Beyond direct services, taxation plays a crucial role in wealth redistribution and funding social safety nets. Progressive tax systems, where higher earners pay a larger percentage of their income in taxes, aim to mitigate income inequality. These revenues support social programs designed to assist vulnerable populations. Examples include Social Security, which provides retirement, disability, and survivor benefits; Medicare and Medicaid, offering healthcare coverage to seniors and low-income individuals; unemployment benefits; and various welfare programs. These initiatives provide a crucial safety net, reduce poverty, and promote social cohesion, demonstrating taxes as an investment in human capital and societal stability.

Understanding Different Types of Taxes

The tax landscape is diverse, encompassing various forms each with distinct purposes and methods of collection. Understanding these categories is key to comprehending one’s overall tax burden and obligations.

Income Tax: Federal, State, and Local

Income tax is perhaps the most widely recognized form of taxation. It is levied on an individual’s or company’s earnings, including wages, salaries, investment gains, and business profits. In the United States, federal income tax is imposed by the Internal Revenue Service (IRS) and is progressive, meaning higher income brackets pay a larger percentage. Many states also impose their own income taxes, which can be progressive, proportional (flat rate), or non-existent in some cases. A few cities or localities might also levy a local income tax. Employers typically withhold a portion of an employee’s income from each paycheck and send it directly to the relevant tax authorities, estimating the annual tax liability.

Payroll Taxes: Social Security and Medicare

Separate from federal income tax, payroll taxes are specifically earmarked to fund Social Security and Medicare. These taxes are paid by both employees and employers. The employee’s share is withheld from their paycheck, along with the employer’s matching contribution. Social Security tax funds retirement, disability, and survivor benefits, while Medicare tax contributes to health insurance for seniors and certain disabled individuals. These are often referred to as FICA (Federal Insurance Contributions Act) taxes and are flat rates up to a certain income threshold for Social Security, while Medicare is applied to all earned income.

Sales Tax and Excise Taxes

Sales tax is imposed on the purchase of goods and services, typically added at the point of sale. The rate varies significantly by state and local jurisdiction, with some states having no sales tax at all. It is generally a regressive tax, as it consumes a larger percentage of income from lower-income individuals who spend a greater proportion of their earnings. Excise taxes are a specific type of sales tax applied to certain goods or services, often those deemed harmful or luxurious, such as tobacco, alcohol, gasoline, and sometimes luxury items. These taxes are often included in the product’s price and are designed to both raise revenue and discourage consumption of specific items.

Property Tax

Property tax is levied on real estate, including land and any structures built upon it. It is primarily collected by local governments (counties, cities, school districts) and is a major source of funding for local public services such as schools, libraries, and local law enforcement. The amount of property tax owed is typically based on the assessed value of the property, which is determined by local tax assessors. Rates vary widely depending on the jurisdiction and the specific needs of the local community.

Capital Gains Tax

When an asset, such as stocks, real estate, or other investments, is sold for a profit, the profit is considered a capital gain and may be subject to capital gains tax. The tax rate depends on how long the asset was held. Short-term capital gains (assets held for one year or less) are typically taxed at ordinary income tax rates, while long-term capital gains (assets held for more than one year) usually qualify for lower preferential tax rates, designed to encourage long-term investment.

The Tax Filing Process: A Step-by-Step Guide

The annual tax filing process can seem daunting, but breaking it down into manageable steps simplifies the journey from gathering documents to submitting your return.

Gathering Your Documents (W-2s, 1099s, Receipts)

The first crucial step is to collect all relevant financial documents. For most employees, this means a Form W-2, provided by your employer, which summarizes your annual wages and taxes withheld. If you have other sources of income, such as from freelancing, investments, or retirement distributions, you’ll receive various Form 1099s (e.g., 1099-NEC for non-employee compensation, 1099-DIV for dividends, 1099-INT for interest). Keep meticulous records of any deductible expenses, such as charitable contributions, medical expenses, or business-related costs, as these will require receipts or other documentation. Mortgage interest statements (Form 1098), student loan interest statements (Form 1098-E), and healthcare statements (Form 1095) are also important.

Choosing Your Filing Method (Software, Professional, Mail)

Taxpayers have several options for preparing and filing their returns. Many opt for tax software programs (e.g., TurboTax, H&R Block), which guide users through the process, perform calculations, and often allow for electronic filing (e-filing). For those with more complex financial situations or who prefer expert assistance, hiring a tax professional (e.g., CPA, enrolled agent) is a common choice. Lower-income individuals may qualify for free tax preparation services offered by the IRS (Free File) or through volunteer programs. Finally, some still choose to manually fill out paper forms and mail them in, though e-filing is generally faster and reduces errors.

Calculating Your Tax Liability

Once all income and deduction information is compiled, the next step is to calculate your total tax liability. This involves determining your gross income, then subtracting eligible deductions to arrive at your Adjusted Gross Income (AGI). From AGI, you’ll subtract either the standard deduction (a fixed amount provided by the IRS) or itemized deductions (specific expenses listed on Schedule A, such as medical expenses, state and local taxes, and mortgage interest), whichever is greater. This results in your taxable income. Your taxable income is then applied to the appropriate tax brackets to determine your gross tax.

Deductions, Credits, and Exemptions

Understanding the difference between deductions and credits is vital for minimizing your tax burden. Deductions reduce your taxable income, thereby lowering the amount of income subject to tax. For example, a $1,000 deduction for someone in the 22% tax bracket saves $220. Tax credits, on the other hand, directly reduce the amount of tax you owe, dollar for dollar. A $1,000 tax credit saves $1,000, regardless of your tax bracket. Some credits are refundable, meaning you can get money back even if you owe no tax, while others are non-refundable. Common credits include the Child Tax Credit, Earned Income Tax Credit, and education credits. Exemptions, largely eliminated for individuals under the Tax Cuts and Jobs Act of 2017 in favor of a higher standard deduction, used to reduce taxable income based on the number of dependents.

Submitting Your Return and Paying What You Owe

After completing all calculations and review, you must submit your tax return by the filing deadline (typically April 15th for most individual taxpayers in the U.S.). If you e-file, your return is transmitted electronically to the IRS and state tax authorities. If you owe additional tax, you can pay electronically (e.g., direct debit from a bank account, credit card), by check, or money order. If you are due a refund, it will typically be issued via direct deposit or a paper check. It’s crucial to file on time, even if you can’t pay the full amount, as failure to file incurs more significant penalties than failure to pay. An extension to file can be requested, but this does not extend the time to pay any taxes due.

Key Concepts and Strategies for Taxpayers

Navigating the tax system effectively requires an understanding of certain key concepts and proactive strategies throughout the year, not just during tax season.

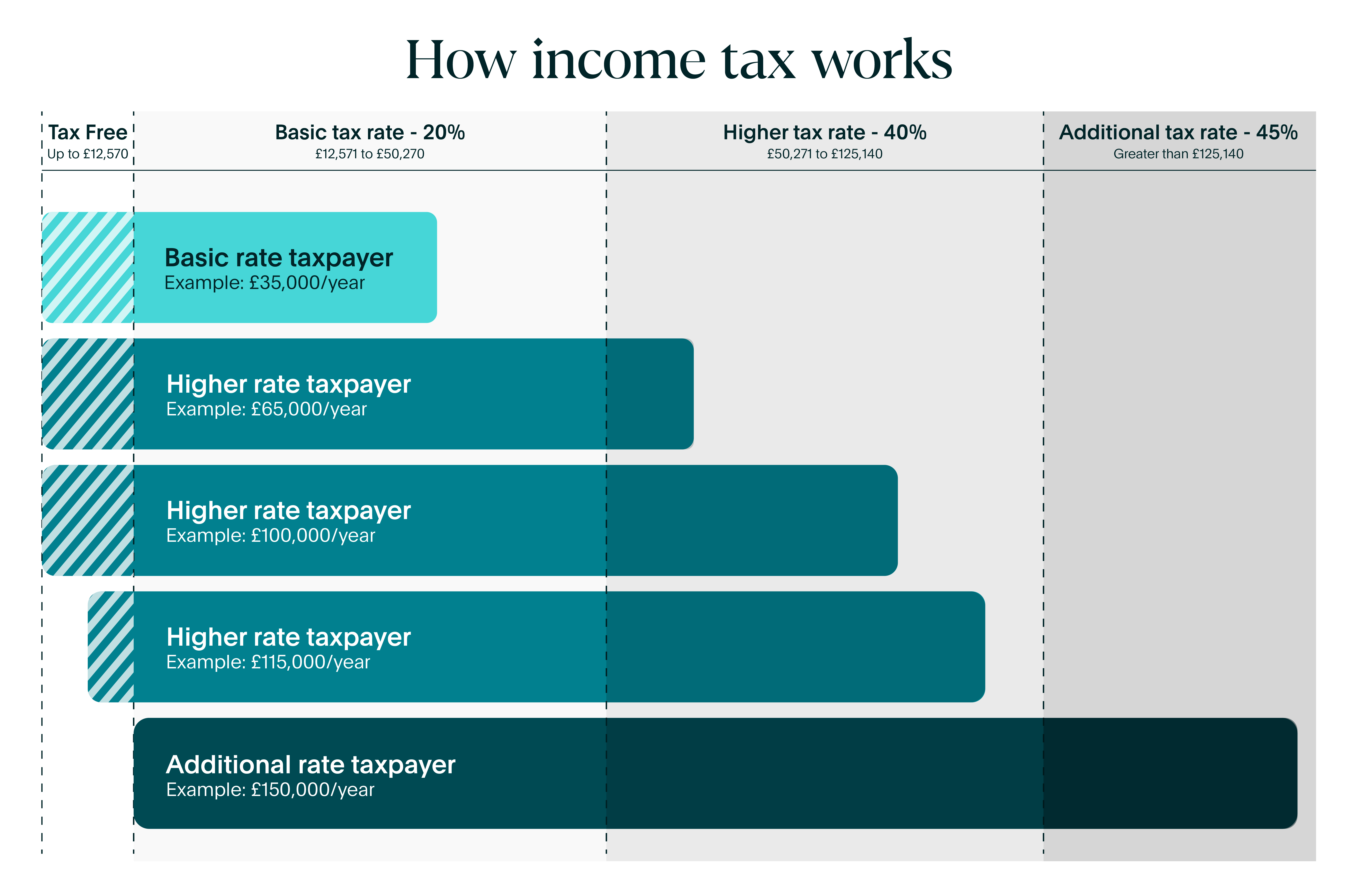

Tax Brackets and Progressive Taxation

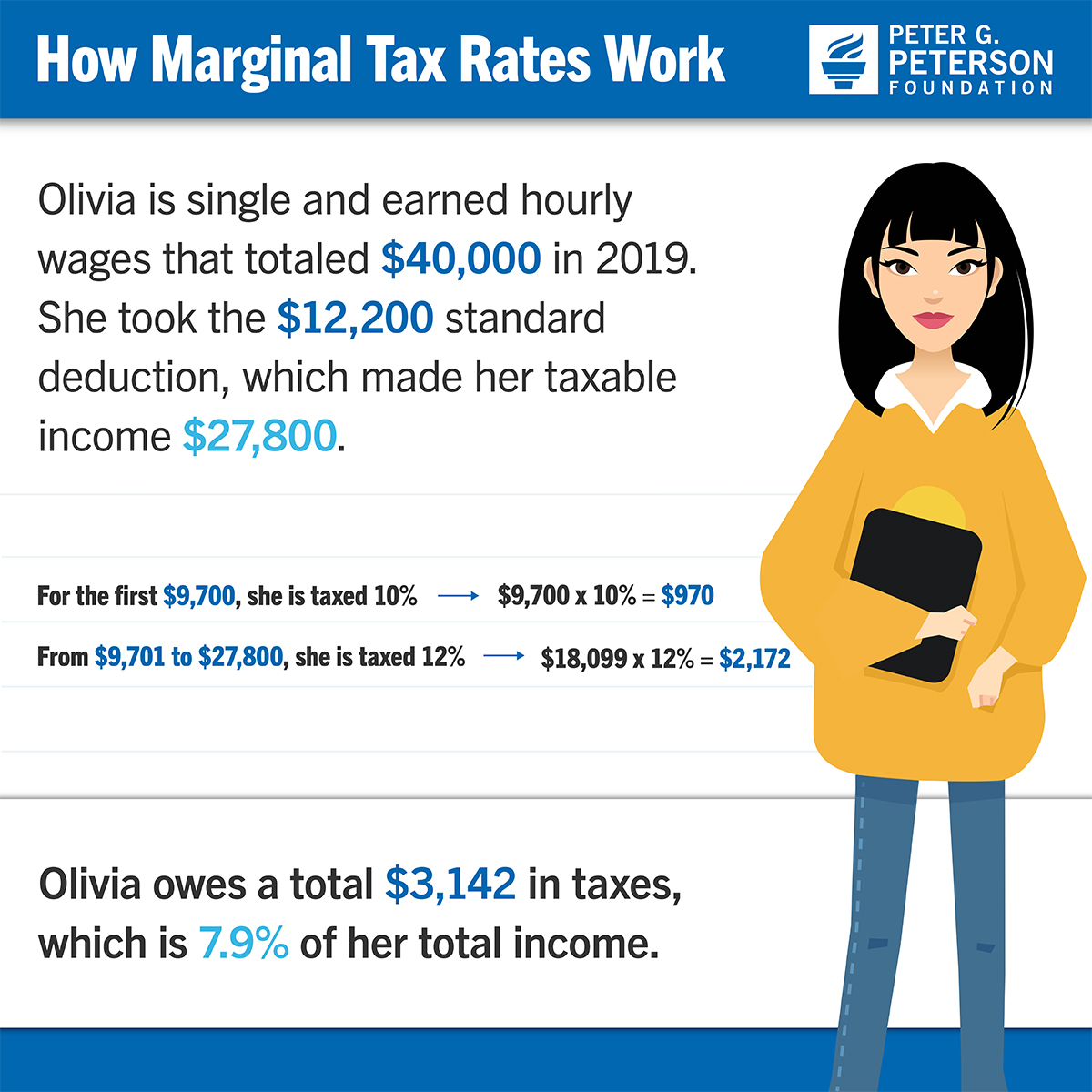

The U.S. federal income tax system operates on a progressive scale, divided into various tax brackets. Each bracket corresponds to a range of income taxed at a specific marginal rate. This means that only the portion of your income that falls within a particular bracket is taxed at that bracket’s rate. For example, if the first $10,000 of income is taxed at 10% and the next $30,000 at 12%, an individual earning $40,000 pays 10% on the first $10,000 and 12% on the remaining $30,000. This progressive structure aims to distribute the tax burden more equitably based on the ability to pay.

Withholding and Estimated Taxes

For most employees, income tax is paid throughout the year via payroll withholding. Your employer estimates your annual tax liability based on the information you provide on Form W-4 and deducts a portion from each paycheck. It’s important to review your W-4 periodically, especially after major life changes, to ensure your withholding accurately reflects your tax situation and avoids a large tax bill or an excessive refund. Self-employed individuals, independent contractors, and those with significant unearned income (e.g., investments, rental property) are generally required to pay estimated taxes quarterly. This ensures they meet their tax obligations throughout the year, similar to employee withholding, to avoid underpayment penalties.

Tax Planning Throughout the Year

Effective tax management is an ongoing process, not just an annual event. Proactive tax planning involves making financial decisions with tax implications in mind. This might include contributing to tax-advantaged retirement accounts (like 401(k)s or IRAs) to reduce taxable income, timing large purchases or sales to optimize capital gains or losses, or planning charitable contributions. Understanding potential deductions and credits you might qualify for and keeping accurate records throughout the year can significantly impact your financial outcome during tax season.

The Importance of Record-Keeping

Meticulous record-keeping is paramount for accurate tax filing and for successfully navigating any inquiries from tax authorities. This includes retaining all W-2s, 1099s, receipts for deductible expenses, bank statements, investment statements, and records of any estimated tax payments. The IRS generally recommends keeping tax records for at least three years from the date you filed your original return or two years from the date you paid the tax, whichever is later. For certain types of records, such as those related to property basis, longer retention periods may be necessary. Good records not only simplify filing but also provide essential documentation if your return is ever audited.

What Happens If You Don’t Pay or Make Mistakes?

While the tax system is designed for compliance, there are mechanisms in place to address non-payment, underpayment, or errors, often involving penalties and potential legal consequences.

Penalties and Interest

Failure to file a tax return on time, even if you don’t owe taxes, can result in significant penalties. The penalty for failure to file is generally 5% of the unpaid taxes for each month or part of a month that a return is late, capped at 25% of your unpaid tax. Similarly, failure to pay taxes by the due date incurs a penalty, typically 0.5% of the unpaid taxes for each month or part of a month the taxes remain unpaid, also capped at 25%. Additionally, interest is charged on underpayments and unpaid taxes, which can compound over time. The IRS also imposes penalties for various other reasons, such as accuracy-related penalties for substantial understatements of tax or negligence.

Audits and Compliance

The IRS conducts audits to ensure the accuracy of tax returns and compliance with tax laws. An audit is a review of an individual’s or organization’s accounts and financial information to confirm that reported income, deductions, and credits are correct. Audits can range from simple correspondence audits (where the IRS requests specific information by mail) to more complex in-person examinations. While relatively few returns are audited each year, being prepared with thorough documentation is essential. If an audit reveals discrepancies or errors, it can lead to additional tax assessments, penalties, and interest. Serious cases of tax evasion can lead to criminal prosecution, including substantial fines and imprisonment.

Seeking Professional Help

When faced with complex tax situations, difficulty understanding the rules, or issues with non-compliance, seeking professional help is highly advisable. Tax professionals, such as Certified Public Accountants (CPAs), enrolled agents, or tax attorneys, possess specialized knowledge and can provide guidance on tax planning, prepare accurate returns, represent taxpayers during audits, and help resolve disputes with tax authorities. While there is a cost associated with professional services, the potential savings in taxes, avoidance of penalties, and peace of mind can often outweigh the expense, particularly for individuals or businesses with intricate financial dealings.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.