The American healthcare system is often criticized for its lack of transparency, particularly when it comes to the fluctuating costs of prescription medications. For many consumers, the price of a life-saving drug can vary by hundreds of dollars depending on which side of the street a pharmacy sits. This financial volatility created a vacuum that GoodRx, a financial technology giant in the healthcare space, stepped in to fill. To understand how GoodRx works, one must look past the user-friendly interface and delve into the complex world of Pharmacy Benefit Managers (PBMs), negotiated rates, and the business of healthcare arbitrage.

By positioning itself as a price aggregator and a financial intermediary, GoodRx has fundamentally changed how millions of Americans manage their personal healthcare budgets. This article explores the mechanics of GoodRx through the lens of finance, detailing how it saves consumers money and how it sustains its own billion-dollar business model.

The Financial Landscape of Prescription Pricing

To grasp the utility of GoodRx, it is essential to first understand why prescription prices are so inconsistent. Unlike a gallon of milk or a digital book, the “price” of a drug is not a fixed number. Instead, it is the result of a complex web of negotiations between manufacturers, wholesalers, insurance companies, and pharmacies.

The Role of Pharmacy Benefit Managers (PBMs)

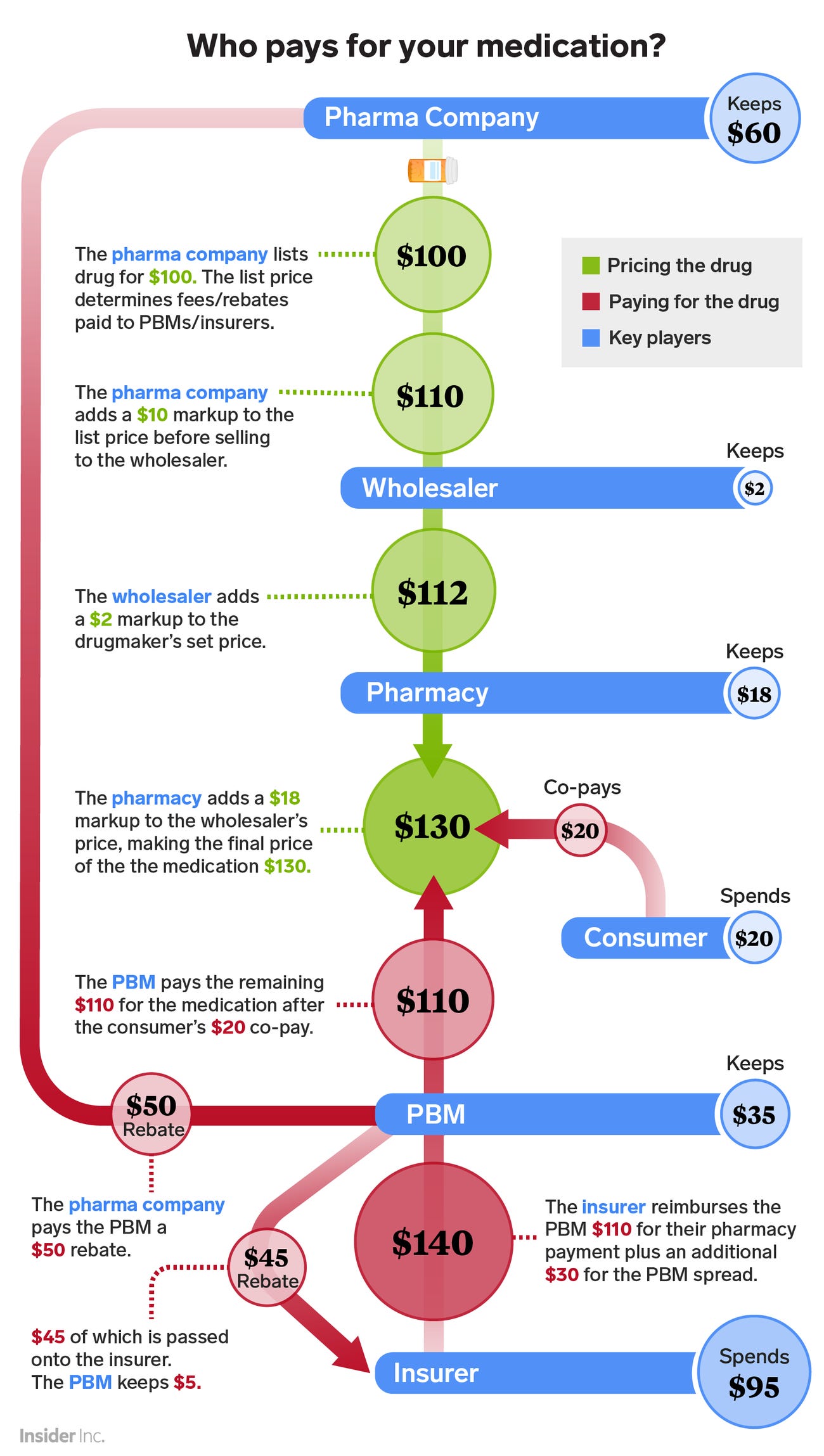

At the heart of the pharmaceutical money trail are Pharmacy Benefit Managers. PBMs are third-party administrators of prescription drug programs for health plans, large employers, and government entities. They are the “middlemen” who negotiate discounts and rebates with drug manufacturers and contract with pharmacies to create reimbursement rates.

GoodRx works by partnering with multiple PBMs to access their proprietary negotiated rates. When you search for a drug on GoodRx, you aren’t seeing the “retail” price; you are seeing the various discounted rates that different PBMs have negotiated with specific pharmacies. Because different PBMs have different contracts, the price for the same drug can vary wildly between providers. GoodRx acts as a financial clearinghouse, surfacing these hidden rates for the general public.

Why Retail Prices Aren’t Fixed

Pharmacies often set high “Usual and Customary” (U&C) prices—essentially the “sticker price” for those paying cash without any insurance or discount. These prices are often inflated to ensure the pharmacy receives the maximum possible reimbursement from insurance companies. However, this leaves the uninsured or underinsured in a precarious financial position. GoodRx exploits this gap by providing consumers access to “contracted rates” that were previously only available to people with premium insurance plans.

Decoding the GoodRx Business Model: How the Platform Generates Revenue

A common question among fiscally-minded observers is: “If the service is free for consumers, how does GoodRx make money?” The answer lies in a sophisticated revenue-sharing model that leverages transaction fees and subscription-based financial products.

Referral Fees and Transactional Commissions

The primary way GoodRx generates revenue is through administrative fees paid by its PBM partners. Every time a consumer uses a GoodRx discount code at a pharmacy, the pharmacy pays a fee to the PBM for processing the transaction. The PBM, in turn, shares a portion of that fee with GoodRx for directing the customer to their specific negotiated rate.

From a business finance perspective, this is a volume-based model. While the commission per transaction might be small, the sheer scale of GoodRx—which facilitates millions of prescriptions monthly—results in significant recurring revenue. This creates a symbiotic relationship: the consumer saves money, the PBM gains a transaction they otherwise wouldn’t have had, and GoodRx earns a commission for facilitating the match.

Gold Subscriptions and Premium Revenue Streams

Recognizing the volatility of transaction-based income, GoodRx expanded its financial portfolio by introducing “GoodRx Gold.” This is a monthly subscription service that provides even deeper discounts on medications and healthcare services.

By shifting a segment of its user base to a subscription model, GoodRx creates “sticky” revenue. This predictable, monthly cash flow is highly valued by investors and allows the company to hedge against fluctuations in the broader PBM market. For the consumer, the financial math is simple: if the monthly subscription fee is lower than the additional savings generated on their recurring medications, the service provides a clear return on investment (ROI).

Advertising and Pharma Manufacturer Solutions

Beyond direct transaction fees, GoodRx utilizes its platform as a high-intent financial marketplace. Pharmaceutical manufacturers often pay GoodRx to feature “co-pay cards” or brand-name advertisements. When a manufacturer wants to encourage patients to choose their brand-name drug over a generic, they provide subsidies. GoodRx integrates these financial incentives into its search results, earning advertising and integration fees while further lowering the out-of-pocket cost for the patient.

Maximizing Personal Finance: Strategies for Using GoodRx Effectively

For the savvy consumer, GoodRx is more than just a coupon app; it is a tool for strategic financial planning. Managing healthcare costs requires a proactive approach to comparing insurance benefits against the cash-price marketplace.

Comparing Insurance Copays vs. GoodRx Cash Prices

One of the most surprising financial realities in modern healthcare is that the GoodRx price is occasionally lower than an insurance copay. This happens because insurance companies often have fixed-tier pricing (e.g., $15 for all Tier 1 generics), while the market “cash” price might drop to $8 due to competition.

A disciplined personal finance strategy involves checking the GoodRx price even if you have insurance. However, there is a trade-off: payments made via GoodRx typically do not count toward an insurance deductible or out-of-pocket maximum. Therefore, consumers must calculate whether the immediate cash savings outweigh the long-term benefit of reaching their insurance deductible sooner.

Geographic Arbitrage: Why Location Matters

The price of a medication can fluctuate based on the zip code or even the specific pharmacy chain. Large retailers like Costco, Walmart, and CVS have different overhead costs and different contracts with PBMs. GoodRx allows for a form of “geographic arbitrage,” where a consumer can save 50% or more just by driving an extra mile to a different provider. For individuals on fixed incomes or those managing chronic conditions, this price comparison can result in thousands of dollars of annual savings.

The Broader Economic Impact on the Healthcare Market

GoodRx does not just benefit the individual; it has broader implications for the economics of the entire healthcare industry. By introducing price transparency, it forces a level of competition that was previously non-existent in the pharmacy sector.

Price Transparency as a Disruptive Force

Before the digital aggregation of drug prices, pharmacies operated in a “black box” environment where consumers had no way of knowing if they were overpaying. In economic terms, this is known as information asymmetry. GoodRx breaks this asymmetry by putting real-time pricing data into the hands of the buyer. This transparency pressures pharmacies to keep their prices competitive to avoid losing foot traffic to rivals, effectively regulating the market through consumer choice rather than government mandate.

Long-term Financial Benefits for the Uninsured and Underinsured

The high cost of medication is a leading cause of “non-adherence,” where patients stop taking their medicine because they cannot afford it. From a macro-financial perspective, non-adherence leads to increased emergency room visits and higher long-term healthcare costs, which burdens the overall economy. By lowering the barrier to entry for essential medications, GoodRx provides a vital financial safety net. It allows the uninsured to access “insured-level” pricing, reducing the risk of medical bankruptcy and improving the overall financial stability of vulnerable populations.

Conclusion: The Intersection of Healthcare and Finance

GoodRx is a prime example of how financial technology can disrupt a legacy industry to the benefit of the consumer. By understanding the underlying mechanics—how PBMs negotiate, how pharmacies set prices, and how the platform extracts value through commissions—users can better navigate the often-confusing world of medical expenses.

Ultimately, “How GoodRx works” is a story of market efficiency. It takes a fractured, opaque system and uses data to create a transparent marketplace. For the modern consumer, utilizing such tools is no longer just a way to save a few dollars; it is an essential component of a sophisticated personal finance strategy in an era of rising healthcare costs. Whether through its free discount codes or its premium subscription tiers, GoodRx remains a powerful ally in the ongoing effort to bring fiscal sanity to the pharmacy counter.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.