Navigating the world of taxes can be complex, especially when you’re responsible for paying them directly to the government throughout the year rather than through employer withholdings. This is the reality for millions of self-employed individuals, small business owners, and those with significant income from sources other than a traditional W-2 job. Understanding how to pay estimated quarterly taxes is not just a compliance requirement; it’s a critical component of sound financial planning, helping you avoid unexpected tax bills and potential penalties.

Understanding Estimated Taxes: Who Needs to Pay?

Estimated taxes are the method used to pay income tax, self-employment tax, and certain other taxes through the year as you earn income, rather than waiting until the annual tax filing deadline. The IRS operates on a “pay-as-you-go” system. If you expect to owe at least $1,000 in tax for the year and your withholding and credits are less than the smaller of (1) 90% of the tax to be shown on your current year’s return, or (2) 100% of the tax shown on your prior year’s return (110% if your adjusted gross income was over $150,000), you likely need to pay estimated taxes.

Self-Employed Individuals and Gig Workers

This is perhaps the most common group subject to estimated taxes. Freelancers, independent contractors, consultants, and individuals earning income through the gig economy (e.g., rideshare drivers, delivery services, online content creators) typically do not have taxes withheld from their payments. Instead, their income is usually reported on Form 1099-NEC (Nonemployee Compensation) or Form 1099-K (Payment Card and Third-Party Network Transactions). Without an employer to manage tax withholdings, the responsibility falls squarely on the individual to estimate and pay their tax liability quarterly. This includes not only income tax but also self-employment tax, which covers Social Security and Medicare contributions for those who work for themselves.

Business Owners (Partnerships, S-Corps, Sole Proprietors)

Owners of sole proprietorships, partnerships, and S-corporations also typically fall into the estimated tax category. While corporations pay estimated taxes, individuals who draw income from these pass-through entities (where profits and losses are passed through to the owners’ personal income) must account for their share of the business’s taxable income. For sole proprietors and partners, this income is subject to self-employment tax in addition to income tax. S-corporation shareholders who also work for the business are often paid a reasonable salary from which taxes are withheld, but distributions beyond that salary may still trigger estimated tax obligations if they are significant.

Individuals with Other Unwithheld Income (Investments, Rental Income)

Estimated taxes aren’t just for business owners. Anyone who receives a substantial amount of income not subject to withholding may need to pay estimated taxes. This includes:

- Investment income: Capital gains from stock sales, dividends, interest from savings accounts or bonds, and certain retirement account distributions.

- Rental income: Profits from renting out properties.

- Alimony: While subject to change, certain alimony payments might require estimated tax payments.

- Gambling winnings: Substantial winnings from lotteries, casinos, or other forms of gambling are generally subject to tax.

The “Substantial Income” Threshold

The general rule of thumb is that if you expect to owe at least $1,000 in taxes for the year, you should be paying estimated taxes. For corporations, the threshold is $500. It’s crucial to remember that this isn’t just about income; it’s about your net tax liability after any credits or deductions. Many people fail to factor in estimated taxes and are hit with a large tax bill and potential penalties at tax time, highlighting the importance of proactive planning.

Calculating Your Estimated Tax Liability

Accurately calculating your estimated tax liability is the cornerstone of effective quarterly tax payments. It involves forecasting your income and deductions for the entire year, which can be challenging, especially for new businesses or freelancers with fluctuating income.

Projecting Your Annual Income and Deductions

The first step is to project your adjusted gross income (AGI) for the entire tax year. This includes all expected income from your self-employment, investments, rentals, and any other sources. Then, estimate your standard or itemized deductions and any tax credits you anticipate qualifying for (e.g., child tax credit, education credits). Subtracting your deductions from your AGI gives you your taxable income, which you then multiply by the appropriate tax rates to determine your gross tax liability. Finally, subtract any expected tax credits to arrive at your estimated total tax for the year. Don’t forget to factor in self-employment taxes (15.3% on the first $168,600 of net earnings for Social Security and 2.9% for Medicare on all net earnings, for 2024, half of which is deductible as an adjustment to income).

Using Form 1040-ES (Estimated Tax for Individuals)

The IRS provides Form 1040-ES, Estimated Tax for Individuals, specifically to help taxpayers calculate their estimated tax. This form includes a worksheet that guides you through projecting your income, deductions, credits, and ultimately, your total estimated tax for the year. It also breaks down how to divide your annual estimated tax into four quarterly payments. While you don’t submit the worksheet itself, it’s an invaluable tool for your personal records and calculation.

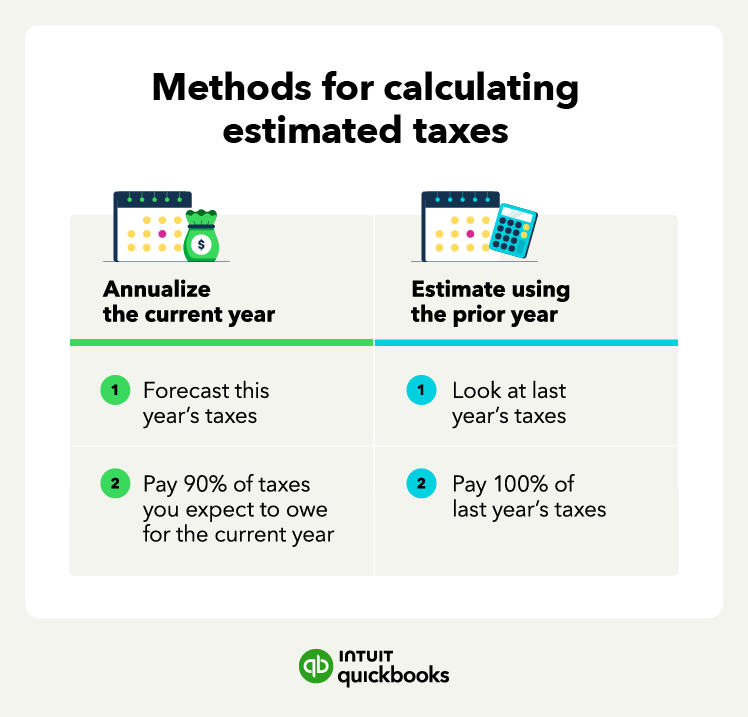

The “Safe Harbor” Rules

To avoid underpayment penalties, you generally need to pay at least 90% of your current year’s tax liability or 100% of your prior year’s tax liability (110% if your prior year’s AGI was over $150,000). These are known as the “safe harbor” rules. Meeting either of these criteria protects you from penalties, even if you end up owing more when you file your annual return. Many prefer to use the prior year’s tax liability as a safe harbor if their income is expected to be similar or higher, as it offers a more concrete figure to work with. If your income fluctuates significantly, you might need to continually adjust your estimates or use the annualized income method.

State Estimated Taxes

Remember that in addition to federal estimated taxes, most states with an income tax also require estimated tax payments if you anticipate owing a certain amount (often around $500-$1,000, but varies by state). The calculation process is similar to federal taxes, using state-specific income, deductions, and tax rates. Be sure to check your state’s tax agency website for their specific requirements and payment methods.

Methods for Paying Your Estimated Taxes

The IRS offers several convenient ways to pay your estimated quarterly taxes, with electronic methods generally being the most efficient and secure.

IRS Direct Pay (Recommended)

IRS Direct Pay is a free, secure web service that allows you to pay your taxes directly from your checking or savings account. You can schedule payments up to 365 days in advance and receive immediate confirmation. This is often the preferred method for individuals as it’s straightforward and doesn’t require pre-registration. You simply choose the type of payment (estimated tax), apply it to Form 1040-ES, and select the tax period.

Electronic Federal Tax Payment System (EFTPS)

EFTPS is another free service offered by the Treasury Department. While it requires enrollment (which can take 5-7 business days to process), it’s highly recommended for business owners and individuals who make multiple tax payments throughout the year. EFTPS allows you to schedule payments up to 365 days in advance, view your payment history, and receive email confirmations. It offers more robust features than IRS Direct Pay, making it suitable for those with more complex tax situations.

Payment by Debit/Credit Card, Digital Wallet

You can also pay your estimated taxes using a debit card, credit card, or digital wallet (PayPal, PayIt, etc.) through one of the IRS-authorized third-party payment processors. While convenient, these processors charge a fee based on the payment amount (typically a percentage for credit/debit and a flat fee for digital wallets). This option might be appealing for those who want to earn credit card rewards or prefer not to use their bank account directly, but the fees should be considered.

Payment by Check or Money Order

For those who prefer traditional methods, you can pay by check or money order. You must make the check or money order payable to the “U.S. Treasury” and include your name, address, daytime phone number, Social Security number, the tax year, and “Form 1040-ES” on the payment. Crucially, you must also include the appropriate payment voucher from Form 1040-ES (Form 1040-ES, Payment Voucher) with your payment and mail it to the correct IRS address. This method is slower and requires careful attention to detail to ensure proper credit.

Withholding from Wages (for those with both W-2 and other income)

If you have a W-2 job in addition to other income that requires estimated taxes, you might be able to avoid making quarterly payments by adjusting the tax withholding from your salary or wages. You can submit a new Form W-4 to your employer, requesting additional tax to be withheld from each paycheck. This can be an effective way to meet your annual tax obligation without the administrative burden of separate quarterly payments. Just ensure the additional withholding is sufficient to cover your estimated tax liability.

Key Deadlines and Avoiding Penalties

Missing deadlines or underpaying your estimated taxes can result in penalties, making it essential to be aware of the due dates and rules.

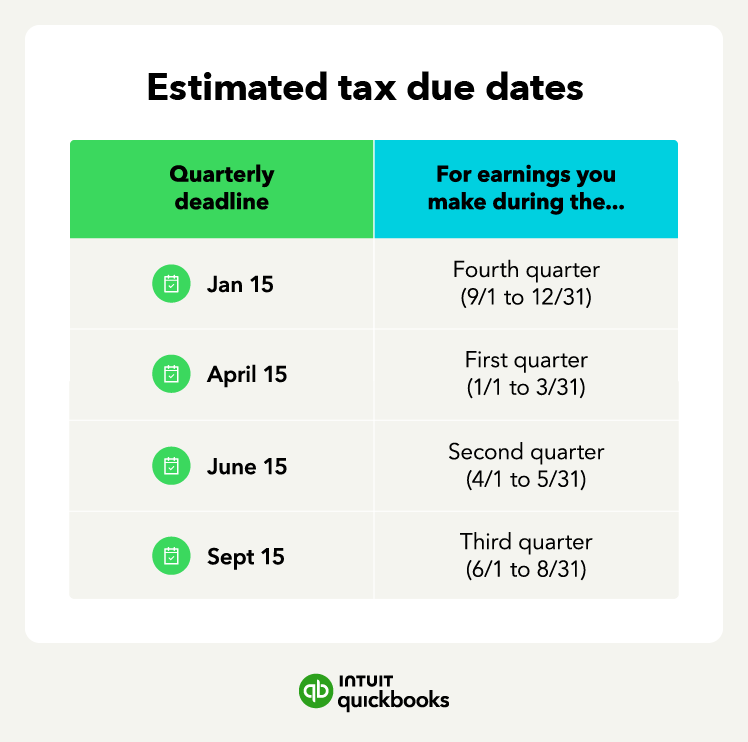

Quarterly Payment Due Dates

The tax year is divided into four payment periods, each with a specific deadline:

- Period 1 (January 1 to March 31): Due April 15

- Period 2 (April 1 to May 31): Due June 15

- Period 3 (June 1 to August 31): Due September 15

- Period 4 (September 1 to December 31): Due January 15 of the following year

If any of these dates fall on a weekend or holiday, the deadline is shifted to the next business day. It’s crucial to mark these dates on your calendar and schedule payments accordingly.

Understanding Underpayment Penalties

The IRS may charge a penalty for underpayment of estimated tax if you don’t pay enough tax throughout the year, either through withholding or by making estimated tax payments. The penalty is typically calculated on the underpaid amount for the period it was underpaid. Even if you receive a refund at the end of the year, you could still be subject to an underpayment penalty if your payments weren’t made on time throughout the year.

Exceptions to the Penalty

There are several situations where the IRS may waive the underpayment penalty:

- Annualized Income Method: If your income varies during the year (e.g., you earn most of your income late in the year), you can use the annualized income method. This allows you to pay less in earlier quarters and more in later quarters, reflecting when the income was earned. You’ll use Form 2210, Underpayment of Estimated Tax by Individuals, Estates, and Trusts, to calculate this.

- Casualty, Disaster, or Other Unusual Circumstances: If the underpayment was due to a casualty, disaster, or other unusual circumstance, and it would be inequitable to impose the penalty, the IRS may waive it.

- Retirement or Disability: If you retired or became disabled during the tax year or the preceding tax year, and you were at least 62 years old, the penalty may be waived if the underpayment was due to reasonable cause and not willful neglect.

Strategies for Managing Estimated Tax Payments Effectively

Proactive management of your estimated taxes can save you stress, time, and money.

Setting Aside Funds Regularly

One of the most effective strategies is to treat a portion of every payment or sale you receive as “tax money.” Open a separate savings account dedicated solely to estimated tax payments and transfer a percentage of your income (e.g., 25-35%, depending on your income level and state taxes) into it immediately. This prevents you from inadvertently spending the money and ensures funds are available when payment deadlines arrive.

Re-evaluating Income and Deductions Periodically

Your initial estimate might not hold true for the entire year. Life happens, and your income or expenses can fluctuate. It’s wise to review your income, deductions, and credits at least once a quarter, or whenever you experience a significant change in your financial situation (e.g., a major new client, a large unexpected expense, a significant investment gain or loss). Adjust your subsequent estimated payments if needed to avoid underpayment or overpayment.

Leveraging Technology: Financial Tools and Software

Modern accounting and financial management software can be invaluable. Many platforms integrate with your bank accounts and automatically track your income and expenses. Some even offer features that help you estimate your tax liability in real-time or set aside funds for taxes. Tools like QuickBooks Self-Employed, FreshBooks, or even robust personal finance software can streamline the process and provide clearer insights into your financial standing.

Seeking Professional Guidance

When in doubt, consult a qualified tax professional. An enrolled agent (EA), certified public accountant (CPA), or tax attorney can help you accurately calculate your estimated tax liability, ensure compliance with federal and state regulations, and advise on strategies to minimize your tax burden legally. They can also help you understand and apply complex rules like the annualized income method, especially if your income patterns are irregular. Investing in professional advice can often save you more than the cost of their services by preventing penalties and optimizing your tax strategy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.