Managing your credit card effectively is a fundamental pillar of sound personal finance. While the question “how do you pay a credit card?” might seem straightforward, its answer encompasses a variety of methods, strategic considerations, and vital implications for your financial health. Beyond simply transferring funds, understanding the nuances of credit card payments is crucial for avoiding debt, building a strong credit score, and achieving financial stability. This guide will walk you through the various payment options, best practices, and essential financial insights to empower you in mastering your credit card payments.

Demystifying Your Credit Card Statement

Before you even consider making a payment, it’s paramount to thoroughly understand your monthly credit card statement. This document isn’t just a bill; it’s a comprehensive report of your spending, payments, and the terms of your credit agreement. Ignoring or misunderstanding it can lead to costly mistakes.

Key Information to Look For

Your credit card statement contains several critical pieces of information that demand your attention. Firstly, locate your Account Summary, which provides an overview of your previous balance, new charges, payments made, and any finance charges or fees. Next, identify your Current Balance, which is the total amount you owe. Crucially, find the Minimum Payment Due, the smallest amount you must pay by the due date to avoid late fees and negative credit reporting. You’ll also see your Payment Due Date, the deadline by which your payment must be received. Other important sections include a detailed list of Transactions, the Interest Rate (Annual Percentage Rate or APR), and any applicable Fees (e.g., late payment fees, annual fees, foreign transaction fees). Understanding each of these components is the first step towards informed payment decisions.

Minimum Payment vs. Full Balance

One of the most significant distinctions on your statement is between the minimum payment and the full balance. The minimum payment is designed to be affordable, but it primarily covers a small portion of your principal balance plus all the accrued interest and fees. Paying only the minimum can significantly prolong your debt repayment journey, accrue substantial interest charges over time, and keep you in debt for years, even decades. In contrast, paying your full balance — also known as “paying in full” — means you settle the entire amount you owe for that billing cycle. This strategy is highly recommended as it allows you to avoid interest charges altogether, assuming you pay by the due date and haven’t carried a balance from a previous cycle (i.e., you are within your grace period). Paying in full is the hallmark of responsible credit card usage.

Due Dates and Grace Periods

The payment due date is the deadline for your payment to be processed and received by your credit card issuer. Missing this date, even by a day, can trigger late fees and, if the payment is more than 30 days late, negatively impact your credit score. Most credit cards offer a grace period, which is the window of time between the end of your billing cycle and your payment due date, during which no interest is charged on new purchases, provided you’ve paid your previous month’s statement balance in full. If you carry a balance from month to month, you typically lose your grace period, and interest starts accruing immediately on new purchases. Understanding and leveraging your grace period by paying your full balance on time is key to using a credit card without incurring interest.

Modern Methods for Credit Card Payments

The landscape of credit card payments has evolved dramatically, offering a plethora of convenient and secure options. Gone are the days when mailing a check was the sole reliable method. Today, digital solutions dominate, providing speed, efficiency, and often, greater control.

Online Banking Portals

The most common and efficient way to pay your credit card is through the issuer’s online banking portal or website. After logging into your account, you can typically navigate to a “Payments” or “Pay Bill” section. Here, you can link your checking or savings account (if you haven’t already), specify the amount you wish to pay (minimum, full balance, or a custom amount), and schedule the payment for a specific date. Online portals often allow you to view past statements, monitor pending payments, and set up alerts, making them a comprehensive tool for credit card management.

Mobile Banking Apps

For even greater convenience, most major credit card issuers offer dedicated mobile banking apps. These apps provide virtually all the functionalities of their online counterparts, optimized for smartphone and tablet use. You can quickly check your balance, review transactions, and make payments on the go. Many apps also support biometric logins (fingerprint or facial recognition) for enhanced security and push notifications to remind you of due dates or payment confirmations. Their ease of access makes them an incredibly popular choice for busy individuals.

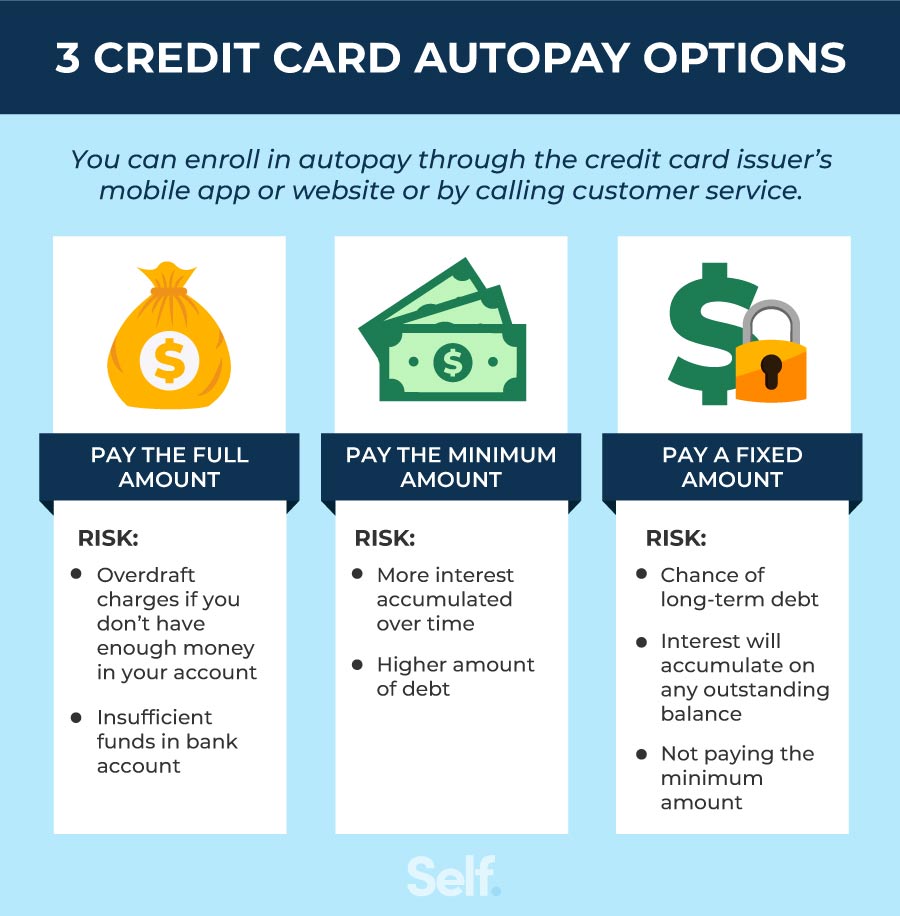

Autopay and Scheduled Payments

To ensure you never miss a payment, setting up autopay is an excellent strategy. This feature automatically deducts a pre-determined amount (e.g., minimum payment, statement balance, or a fixed amount) from your linked bank account on or before your due date. While autopay guarantees timely payments, it’s crucial to ensure you always have sufficient funds in your linked account to avoid overdraft fees. Alternatively, you can schedule one-time or recurring payments manually through your online portal or app, giving you more granular control over each transaction while still benefiting from automation.

Telephone Payments

If you prefer a more traditional, direct interaction, most credit card companies offer the option to make payments over the phone. You can usually find the customer service number on the back of your card or on your statement. You’ll typically speak to an automated system or a customer service representative, providing your account details and bank information. While convenient for those without internet access or who prefer verbal confirmation, be aware that some issuers might charge a small fee for payments made over the phone, especially if assisted by a representative.

Mail-in Payments (Checks)

While less common today, paying by mail with a check remains an option. Your credit card statement will typically include a payment slip and the mailing address for remittances. It’s essential to mail your payment several business days before the due date to account for postal delivery times and processing. This method carries the risk of delays or loss in transit and offers less immediate confirmation compared to digital methods.

In-Person Payments

For those who prefer face-to-face transactions, some credit card issuers allow in-person payments at their bank branches. Additionally, certain retailers or payment centers might facilitate credit card payments. This option can be useful if you need to make a last-minute payment and want immediate confirmation, but its availability depends on your issuer and location. Always verify if this service is offered and if any fees apply before heading out.

Strategic Approaches to Credit Card Payment

Paying your credit card isn’t just about the “how”; it’s significantly about the “when” and “how much.” Strategic payment approaches can save you money, improve your credit, and reduce financial stress.

Always Pay More Than the Minimum

The single most impactful strategy for responsible credit card usage is to always pay more than the minimum payment due. As discussed, the minimum payment is designed to keep you in debt. By paying extra, you reduce your principal balance more quickly, which in turn reduces the amount of interest you’re charged on that balance in subsequent billing cycles. Even a small additional amount can make a significant difference over time, accelerating your path to debt freedom.

Paying Your Balance in Full

The gold standard of credit card management is paying your statement balance in full every single month. When you do this, you avoid all interest charges on new purchases (provided you have a grace period), effectively using the credit card as a convenient payment tool rather than a loan. This practice also demonstrates excellent financial discipline and contributes positively to your credit utilization ratio, a key factor in your credit score.

Timing Your Payments

Consider making payments strategically, especially if you carry a balance. You don’t have to wait until the due date. Making multiple smaller payments throughout the month (e.g., after each paycheck) can help reduce your average daily balance, which is what some issuers use to calculate interest. This can also help you keep track of your spending and prevent a large balance from accumulating by the end of the billing cycle. For those who pay in full, simply ensuring your payment processes by the due date is sufficient.

Dealing with Multiple Credit Cards

If you manage multiple credit cards, developing a coherent payment strategy is crucial. One common approach is the debt avalanche method, where you pay the minimum on all cards except the one with the highest interest rate, on which you focus all extra payments. Once that card is paid off, you move to the next highest interest rate. Another method is the debt snowball method, where you focus on paying off the card with the smallest balance first for psychological motivation, regardless of interest rate. Both methods require diligence but can be highly effective in tackling multi-card debt.

Understanding Interest Charges and Fees

A clear understanding of how interest charges and fees work is essential. Interest is typically calculated based on your average daily balance and your Annual Percentage Rate (APR). High APRs mean higher interest costs. Fees can include late payment fees, over-limit fees, foreign transaction fees, and annual fees. Always strive to avoid these by paying on time, staying within your credit limit, and being aware of any specific card terms. If you incur a fee, understand why and try to prevent it in the future.

Protecting Your Credit Score and Financial Future

Your credit card payment habits are a direct reflection of your financial responsibility and significantly impact your credit score. Maintaining good payment practices is vital for unlocking future financial opportunities.

The Dangers of Late Payments

Late payments are among the most detrimental actions to your credit score. A payment reported 30 days or more past due can cause a significant drop in your score, which can take years to recover from. Beyond the immediate late fees imposed by the issuer, a poor payment history signals risk to potential lenders, impacting your ability to secure loans, mortgages, or even rental agreements in the future. Prioritize timely payments above all else.

Impact on Your Credit Score

Your credit score is primarily determined by five factors: payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%), and credit mix (10%). Your payment habits directly influence the largest two factors. Consistently paying on time builds a strong payment history. Keeping your balances low relative to your credit limits (known as credit utilization) positively impacts the “amounts owed” category. Ideally, aim to keep your credit utilization below 30%, but below 10% is even better for top scores.

Managing High Balances (Credit Utilization)

If you find yourself carrying high balances, work actively to reduce them. A high credit utilization ratio (e.g., using 70% or more of your available credit) can signal financial distress to credit bureaus, even if you’re making payments on time. Focus on paying down your most expensive debts first, or consider a balance transfer to a lower-APR card if you qualify and can pay it off within the promotional period. Actively managing down high balances not only saves you interest but also demonstrably improves your credit score.

Setting Up Alerts and Reminders

Leverage technology to help you stay on track. Most credit card issuers allow you to set up email or SMS alerts for upcoming due dates, payment confirmations, or when your balance approaches your credit limit. Budgeting apps and calendar reminders can also serve as invaluable tools to ensure you never miss a payment and remain aware of your financial obligations. Proactive monitoring can prevent costly mistakes.

Leveraging Financial Tools for Payment Management

Beyond the immediate payment mechanics, effective credit card management is integrated with broader personal finance practices and tools.

Budgeting Apps and Software

Modern budgeting apps (like Mint, YNAB, Personal Capital, or even simple spreadsheets) can be incredibly effective in helping you track your spending, understand your cash flow, and allocate funds for credit card payments. By categorizing your expenses and income, you can clearly see how much disposable income you have available to put towards your credit card debt, making it easier to consistently pay more than the minimum or pay in full. These tools provide a holistic view of your finances, ensuring credit card payments are part of a larger, well-planned financial strategy.

Debt Repayment Strategies

If you’re facing significant credit card debt, consider structured debt repayment strategies. As mentioned earlier, the debt snowball (paying smallest balance first for motivation) and debt avalanche (paying highest interest rate first to save money) methods can provide a clear roadmap. These strategies help you focus your efforts and maintain momentum, making the daunting task of debt repayment more manageable and structured.

Consolidating Debt

For individuals with high-interest debt spread across multiple credit cards, debt consolidation might be an option. This involves combining several debts into a single, new loan, often with a lower interest rate. Options include personal loans, balance transfer credit cards, or home equity loans. While consolidation can simplify payments and potentially save on interest, it’s crucial to address the underlying spending habits to avoid accumulating new debt on the old cards. It’s a tool for managing existing debt, not a license for new spending.

In conclusion, paying a credit card is more than a transactional act; it’s a critical component of personal finance management. By understanding your statements, utilizing modern payment methods, adopting strategic payment habits, and proactively protecting your credit score, you can transform credit cards from potential liabilities into powerful tools for building a robust financial future. Responsible credit card usage is a testament to financial literacy and discipline, paving the way for greater economic freedom and opportunity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.