Securing a business loan is a pivotal milestone in the lifecycle of any enterprise. Whether you are a startup seeking initial capital to launch operations or an established corporation looking to scale, the infusion of debt capital can provide the necessary leverage to achieve strategic objectives. However, the path to funding is often perceived as a labyrinth of complex requirements, stringent credit assessments, and exhaustive paperwork. To navigate this process successfully, an entrepreneur must shift their perspective from that of a solicitor to that of a strategic partner.

Obtaining a business loan is not merely about asking for money; it is about demonstrating to a financial institution that your business is a viable, low-risk vehicle for investment. This guide explores the multifaceted landscape of business finance, detailing the types of loans available, the criteria lenders use for evaluation, and the systematic steps required to move from application to disbursement.

Understanding the Landscape: Different Types of Business Loans

Before approaching a lender, it is critical to understand that “business loans” are not a monolithic product. Different financial needs require different structures. Selecting the wrong type of loan can lead to unnecessary interest expenses or cash flow bottlenecks.

Traditional Term Loans

The most common form of business financing is the term loan. In this arrangement, a lender provides a lump sum of capital, which the borrower repays over a fixed schedule with either a fixed or variable interest rate. Term loans are typically used for long-term investments, such as business expansion, acquisitions, or significant capital expenditures. They are categorized by their duration: short-term loans (3–18 months) for immediate needs and long-term loans (up to 10 years or more) for major projects.

Business Lines of Credit

Unlike a term loan, a business line of credit offers flexibility. It operates similarly to a credit card, where a lender approves a maximum credit limit. The business can draw from this pool of funds as needed and only pays interest on the amount actually borrowed. This is an ideal tool for managing seasonal fluctuations in cash flow, covering unexpected repairs, or taking advantage of short-term inventory discounts.

SBA Loans

The U.S. Small Business Administration (SBA) does not lend money directly to business owners. Instead, it provides a federal guarantee to banks and credit unions, reducing the risk for the lender. The most popular programs, such as the 7(a) and 504 loans, offer some of the most competitive interest rates and longest repayment terms in the market. However, because of these favorable terms, the application process for SBA loans is famously rigorous and time-consuming.

Equipment and Invoice Financing

Asset-based lending allows businesses to use their own collateral to secure funding. In equipment financing, the equipment itself serves as the security for the loan, often allowing for lower interest rates. Invoice financing (or factoring) allows businesses to “sell” their outstanding accounts receivable to a lender for an immediate cash advance. This is particularly useful for B2B companies with long payment cycles who need to unlock working capital trapped in unpaid invoices.

Evaluating Your Readiness: Key Financial Requirements

Lenders operate on the principle of risk mitigation. To get a “yes,” you must prove that the probability of default is minimal. This evaluation generally centers on the “Five Cs of Credit”: Character, Capacity, Capital, Collateral, and Conditions.

Credit Scores: Personal and Business

While your business may be a separate legal entity, most lenders—especially for small to mid-sized enterprises—will scrutinize the personal credit score of the owner. A score above 680 is generally required for traditional bank loans, while SBA loans may require even higher benchmarks. Additionally, as your business grows, it will develop its own credit profile through agencies like Dun & Bradstreet. Maintaining a clean repayment history is the foundational requirement for any loan approval.

Cash Flow and Revenue Statements

Profitability is important, but cash flow is king. A lender will analyze your Debt Service Coverage Ratio (DSCR), which measures your business’s ability to use its operating cash flow to pay back its debt obligations. Generally, lenders look for a DSCR of 1.25 or higher, meaning for every dollar of debt, the business generates $1.25 in income. You will need to provide at least two years of profit and loss (P&L) statements and balance sheets to prove consistent revenue generation.

Collateral and Personal Guarantees

Even with a strong cash flow, many lenders require collateral—tangible assets like real estate, inventory, or equipment—that can be seized if the loan is not repaid. For many small business owners, a “personal guarantee” is also a standard requirement. This legally binds the owner’s personal assets to the loan, ensuring that the borrower is fully committed to the success of the venture.

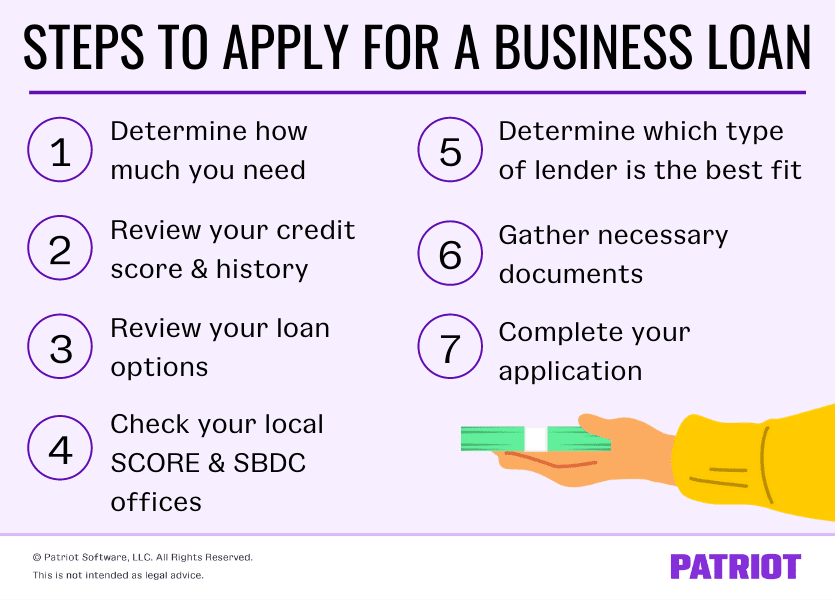

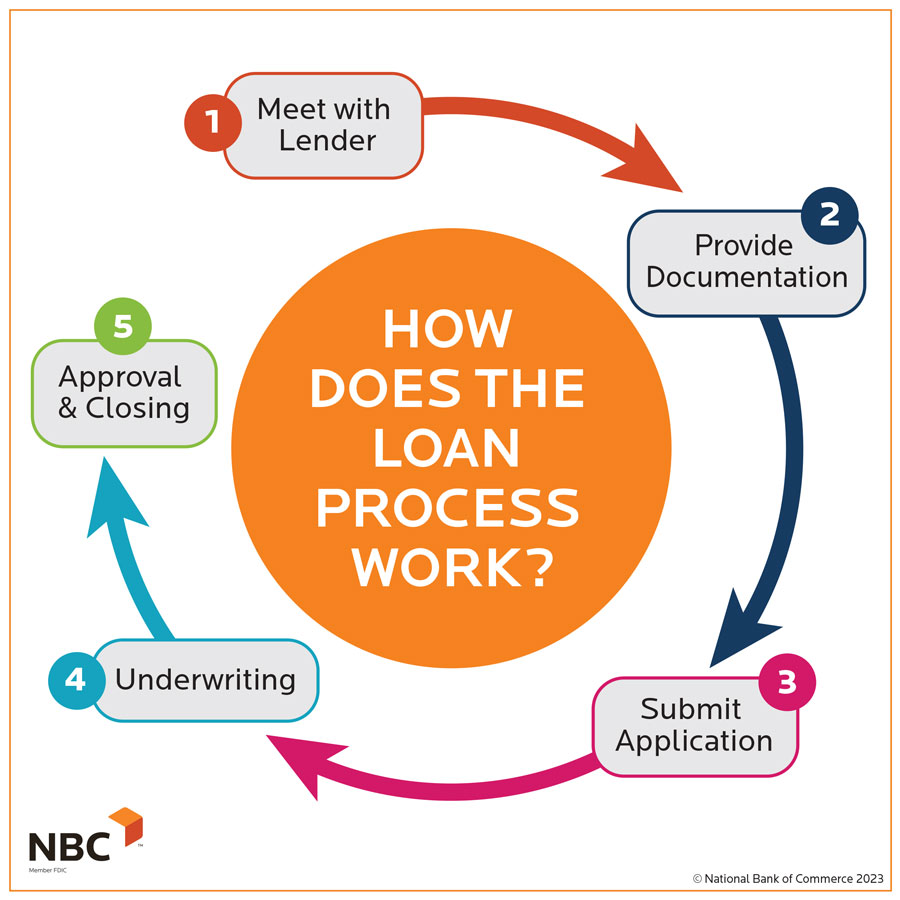

The Application Process: Step-by-Step Execution

Once you have identified the appropriate loan type and verified your financial health, the application process begins. Preparation is the difference between a quick approval and a frustrating rejection.

Developing a Solid Business Plan

A business plan is more than a roadmap for the owner; it is a persuasive document for the lender. It should clearly outline the purpose of the loan, how the funds will be deployed, and the specific ways in which the capital will generate additional revenue. Lenders want to see that you have a deep understanding of your market, your competitors, and your financial projections. A vague request for “working capital” is far less effective than a detailed plan to “expand the sales team to capture an additional 15% of the regional market.”

Gathering Essential Documentation

The “paperwork” phase is where many applications stall. To streamline the process, prepare a comprehensive digital folder containing:

- Federal and state income tax returns (personal and business) for the last three years.

- Interim financial statements (P&L and Balance Sheet).

- Business licenses and articles of incorporation.

- Existing lease agreements and contracts.

- A detailed “Use of Proceeds” statement.

Choosing the Right Lender

Not all financial institutions are created equal. Large national banks offer the lowest rates but have the strictest criteria. Community banks and credit unions may be more flexible and willing to look at the “story” behind the numbers. On the other end of the spectrum, online alternative lenders (FinTechs) offer rapid funding—sometimes within 24 hours—but often at significantly higher interest rates. Matching your business’s profile with the lender’s risk appetite is crucial.

Strategies for Success: Improving Your Approval Odds

If your initial financial profile isn’t perfect, there are proactive steps you can take to make your business more “bankable” before you submit your application.

Debt-to-Income Ratio Optimization

Before applying for new debt, consider consolidating or paying down existing high-interest debt. Reducing your current liabilities improves your DSCR and signals to the lender that you are a disciplined borrower. Even a minor improvement in your debt-to-income ratio can move you into a different risk tier, potentially saving you thousands of dollars in interest over the life of the loan.

Building Professional Relationships

Banking is still a relationship business. Establishing a rapport with a commercial loan officer long before you need a loan can be highly beneficial. If a banker understands your business model and has seen your growth over time, they are more likely to advocate for your application when it reaches the credit committee. Attend local networking events or ask for an introductory meeting to discuss your long-term vision.

Accuracy and Transparency

The fastest way to a rejection is a discrepancy in your financial data. Ensure that your tax returns match your internal accounting software. If there were “one-time” losses or anomalies in your financial history (such as a pandemic-related dip), be transparent and provide a written explanation. Lenders value honesty and a proactive approach to addressing potential red flags.

By treating the loan process as a professional presentation of your business’s value and stability, you position yourself not as a borrower in need, but as a partner in growth. Understanding the mechanics of finance allows you to secure the capital necessary to turn your corporate vision into a reality, ensuring the long-term sustainability and success of your brand.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.