In the realm of finance, numbers are the fundamental building blocks, but percentages are the language that gives those numbers meaning. Whether you are analyzing the performance of a stock portfolio, determining the sustainability of a household budget, or calculating the interest on a high-yield savings account, the question of “how do you find the percentage” is central to making informed decisions.

Understanding percentages allows you to strip away the raw dollar amounts and see the relative health of your financial life. A $500 profit might seem substantial in isolation, but its significance changes drastically if it represents a 5% return on a $10,000 investment versus a 50% return on a $1,000 investment. This article explores the essential methods for calculating percentages within the context of money management, providing you with the tools to navigate personal finance, investing, and business with precision.

The Fundamentals of Financial Percentages

Before diving into complex financial models, one must master the basic arithmetic of percentages. At its core, a percentage is simply a ratio or a fraction of 100. In money management, this usually represents a “part” of a “whole”—such as a tax portion of a total salary or a dividend portion of a stock price.

The Basic Formula for Financial Proportions

The most common way to find a percentage in finance is to divide the part by the whole and then multiply by 100.

Formula: (Part / Whole) x 100 = Percentage

For example, if you are setting aside $500 from a $4,000 monthly paycheck for savings, the calculation would be ($500 / $4,000) x 100. This equals 0.125 x 100, or 12.5%. Understanding this allows you to compare your savings rate against industry benchmarks or your own historical performance.

Calculating Percentage Increase and Decrease

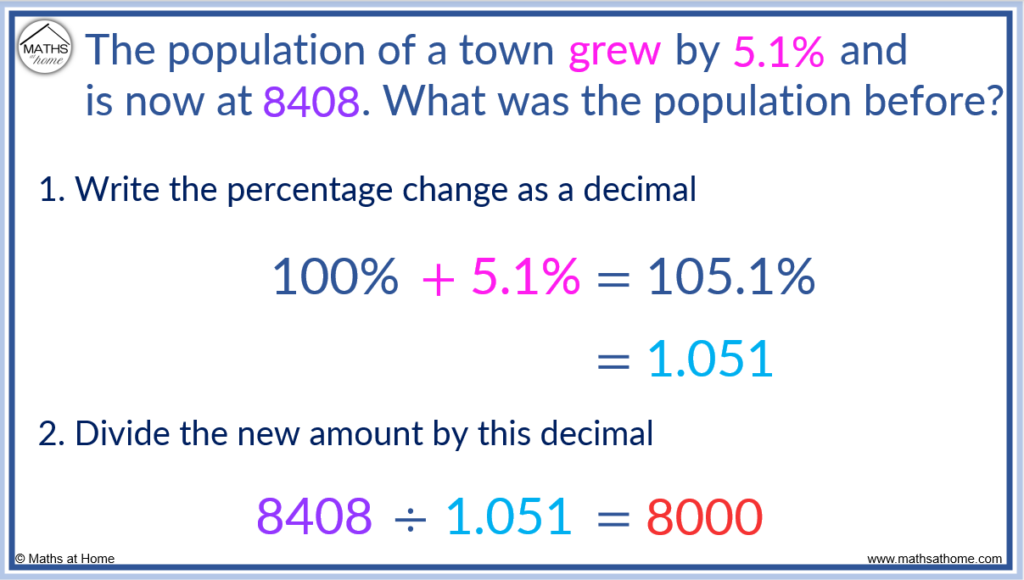

In the world of investing and market trends, we rarely look at static numbers; we look at movement. To find the percentage change—such as a stock’s growth or a currency’s devaluation—you must use the change formula.

Formula: [(New Value – Old Value) / Old Value] x 100

If an index fund you own grows from $150 per share to $180 per share, the “New Value” is $180 and the “Old Value” is $150. The difference is $30. Dividing $30 by the original $150 gives you 0.2, or a 20% increase. Conversely, if the price dropped, the result would be negative, representing a percentage loss. Mastering this calculation is vital for tracking the volatility and growth of any financial asset.

Percentages in Personal Finance and Budgeting

Strategic budgeting is less about tracking every penny and more about managing the percentages of your income. By viewing your finances through the lens of percentages, you create a scalable system that works whether you earn $30,000 or $300,000 a year.

The 50/30/20 Rule of Allocation

One of the most effective ways to apply percentages to personal finance is the 50/30/20 rule. This framework suggests that you should allocate:

- 50% to Needs: Housing, utilities, groceries, and insurance.

- 30% to Wants: Dining out, hobbies, and travel.

- 20% to Financial Goals: Debt repayment, emergency funds, and retirement.

By calculating these percentages monthly, you can identify if your “needs” are consuming too much of your income. If your rent alone takes up 45% of your income, the percentage-based view warns you that you are “house poor,” a realization that might be obscured if you only looked at the dollar amount of your remaining balance.

Debt-to-Income Ratio (DTI)

Lenders use percentages to determine your creditworthiness, specifically the Debt-to-Income (DTI) ratio. This is calculated by dividing your total monthly debt payments by your gross monthly income.

A DTI of 36% or lower is generally considered healthy. If you are applying for a mortgage, the lender will find the percentage of your income that will go toward the new loan. If that percentage pushes your total DTI above 43%, you may face higher interest rates or loan rejection. Knowing how to calculate this percentage yourself allows you to “stress test” your finances before approaching a bank.

Investing and Wealth Building Metrics

In the investment world, percentages are the ultimate equalizer. They allow you to compare a multi-billion dollar corporation to a small-cap startup on equal footing.

Return on Investment (ROI)

ROI is the most critical percentage for any investor. It measures the efficiency of an investment or compares the efficiencies of several different investments.

Formula: (Net Profit / Cost of Investment) x 100

Consider a real estate investment where you buy a property for $200,000 and sell it for $250,000 after expenses. Your net profit is $50,000. Your ROI is ($50,000 / $200,000) x 100 = 25%. Without the percentage, the $50,000 might look impressive, but the ROI tells you exactly how hard your money worked for you over the duration of the holding period.

Understanding Compound Interest and Annual Yields

Wealth is built through the magic of compounding, which is essentially a percentage being applied to a balance that includes previously earned percentages. When evaluating a certificate of deposit (CD) or a dividend-paying stock, you must understand the Annual Percentage Yield (APY).

Unlike a simple interest rate, the APY reflects the effect of compounding. If a bank offers a 5% interest rate compounded monthly, the APY will actually be slightly higher (approximately 5.12%). Knowing how to find and compare these percentages ensures that you are placing your capital in the most productive environment possible.

Business Finance and Profitability

For entrepreneurs and business owners, percentages are the primary indicators of operational health. Revenue is often referred to as the “top line,” but it is the “bottom line” percentages—the margins—that determine a company’s survival.

Gross vs. Net Profit Margins

A business might generate $1 million in sales, but if its expenses are $950,000, it is in a precarious position. Profit margins provide the necessary context.

- Gross Profit Margin: This is (Gross Profit / Revenue) x 100. It shows how efficiently a company produces its goods or services before overhead.

- Net Profit Margin: This is (Net Income / Revenue) x 100. This is the “true” percentage of every dollar that remains as profit after all taxes, interest, and operating expenses are paid.

A high net profit margin (e.g., 20% or more) suggests a business with a strong competitive advantage and disciplined cost management. If you find the percentage of your margin is shrinking year-over-year, it serves as an early warning system to adjust pricing or cut costs.

Tax Obligations and Effective Tax Rates

In business and personal finance, your “tax bracket” is a percentage, but it is rarely the percentage you actually pay. Your Effective Tax Rate is the percentage of your total income that goes to the government after deductions and credits.

To find this percentage, divide your total tax paid by your total earned income. Understanding this percentage is vital for “tax-loss harvesting” and other wealth-preservation strategies. For example, if you are in a 32% marginal bracket but your effective rate is only 18%, your financial planning should be based on the latter to ensure accurate cash flow projections.

Practical Tools and Modern Financial Calculators

While understanding the manual formulas is essential for financial literacy, modern tools have made finding percentages faster and more integrated into our daily workflows.

Spreadsheet Formulas for Dynamic Analysis

For anyone serious about money, Excel or Google Sheets is the ultimate tool. You don’t need to do the long-form math; you only need to know the syntax.

- To find the percentage of a total:

=A1/B1(then click the “%” button in the toolbar). - To find a percentage increase:

=(New-Old)/Old. - To calculate a tip or tax:

=Total * 0.15(for a 15% rate).

Automating these calculations in a personal budget or a business P&L (Profit and Loss) statement allows for “what-if” scenarios. You can change one percentage—like your savings rate—and instantly see the impact on your projected retirement date.

Digital Wealth Management and Fintech Apps

We live in an era of “Fintech,” where apps like Mint, YNAB (You Need A Budget), or Personal Capital do the heavy lifting. These tools automatically find the percentages of your spending by category (e.g., “You spent 12% more on dining out this month”).

However, the professional approach is to use these tools as a starting point, not a crutch. By knowing the underlying math, you can spot errors in how an app categorizes a transaction or better understand the “expense ratio” of a mutual fund—a percentage that represents the fee you pay to the fund’s managers. A seemingly small 1% fee can consume nearly 25% of your total gains over a 30-year investment horizon due to the loss of compounding.

Conclusion

Finding the percentage is more than a simple math problem; it is a fundamental skill for anyone seeking financial independence. Whether you are measuring the growth of a small side hustle, optimizing your personal budget, or evaluating the net profit margins of a Fortune 500 company, percentages provide the clarity needed to cut through the noise of raw data. By mastering these formulas and understanding their implications, you transform from a passive observer of your bank account into an active architect of your financial future. Money, after all, is a game of margins, and those who understand the percentages are the ones who ultimately win.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.