In the world of finance, numbers are the raw data, but percentages are the story. Whether you are tracking the growth of a retirement portfolio, calculating the interest on a high-yield savings account, or analyzing the profit margins of a side hustle, the ability to convert raw numbers into percentages is an essential skill. Understanding this conversion allows investors and savers to compare disparate assets on an equal playing field. While a $500 gain on a stock might sound impressive, it takes on a different meaning when you realize it represents a 50% return on a $1,000 investment versus a 0.5% return on a $100,000 investment.

This guide explores the mechanics of converting numbers into percentages within the context of personal and business finance, providing you with the tools to make more informed economic decisions.

The Fundamental Role of Percentages in Personal and Business Finance

Percentages serve as the universal language of the financial markets. They provide a standardized way to measure change, risk, and reward regardless of the currency or the scale of the capital involved. In personal finance, we use percentages to determine if our spending is within budget; in business finance, we use them to assess the health of a company’s balance sheet.

Why Decimals and Fractions Matter in Your Bank Account

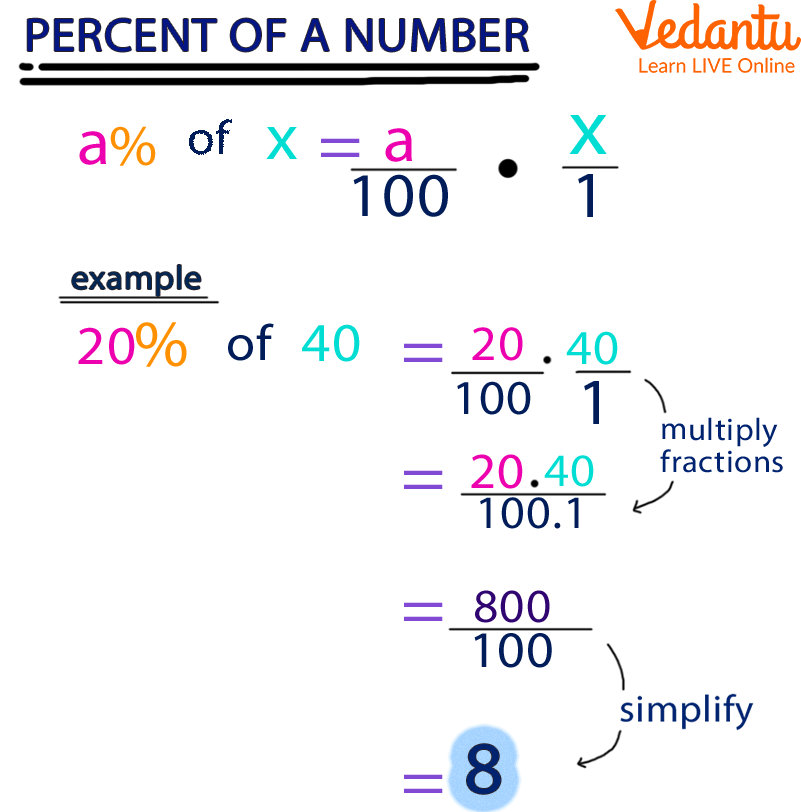

To master percentage conversion, one must first understand that a percentage is simply a different way of expressing a fraction or a decimal. The word “percent” literally translates to “per one hundred.” Therefore, every percentage is a ratio with 100 as its denominator.

In a financial context, seeing your savings account interest rate as 0.04 (decimal) is less intuitive than seeing it as 4% (percentage). Converting decimals to percentages is the most common mathematical operation in finance. The rule is simple: multiply the decimal by 100 and add the “%” sign. For example, if a financial advisor tells you that a specific expense represents 0.25 of your income, moving the decimal point two places to the right reveals that you are spending 25% of your earnings in that category.

The Basic Formula: Part Over Whole

At the heart of every financial percentage is the “Part over Whole” formula. To convert any two numbers into a percentage, you divide the portion you are analyzing (the part) by the total amount (the whole), then multiply by 100.

Formula: (Part / Whole) × 100 = Percentage

Consider a household budget. If your total monthly income is $5,000 and your rent is $1,500, the calculation would be ($1,500 / $5,000) = 0.30. Multiply by 100, and you find that your rent consumes 30% of your income. This conversion is the first step in applying the “50/30/20” rule of budgeting, where 50% goes to needs, 30% to wants, and 20% to savings.

Practical Applications: Converting Investment Returns and Gains

For investors, converting numbers to percentages is not just a mathematical exercise; it is the primary way to measure performance. Raw dollar amounts can be deceptive because they do not account for the size of the initial capital outlay.

Calculating Return on Investment (ROI)

The most critical percentage for any wealth-builder is the Return on Investment (ROI). This metric allows you to compare the efficiency of different investments, such as real estate versus the stock market.

To calculate ROI as a percentage, you take the net profit of the investment, divide it by the initial cost, and multiply by 100.

ROI = [(Current Value – Original Cost) / Original Cost] × 100

For instance, if you bought a share of a tech company for $150 and sold it for $180, your profit is $30. While $30 might seem like a small amount in isolation, the conversion reveals a different story: ($30 / $150) × 100 = 20%. A 20% return is a significant gain, regardless of whether the dollar amount was $30 or $30,000.

Understanding Yield and Interest Rates

Yield is another area where conversion is paramount. Bond yields and dividend yields are expressed as percentages to show how much cash flow an investment generates relative to its price. If a stock pays an annual dividend of $2.00 per share and the stock is trading at $50.00, the dividend yield is ($2 / $50) × 100 = 4%.

Similarly, when dealing with debt, such as credit cards or mortgages, the interest is always expressed as an Annual Percentage Rate (APR). Knowing how to convert the interest charges on your monthly statement back into a percentage can help you verify that you are being charged the correct rate and understand the true cost of borrowing.

Analyzing Market Trends and Business Growth

In business finance and macroeconomics, we are rarely interested in static numbers. We want to know the direction and velocity of change. This is where calculating percentage increases and decreases becomes essential for tracking inflation, revenue growth, and market share.

Calculating Percentage Increase and Decrease

Whether you are looking at a rise in the Consumer Price Index (CPI) or a drop in your business expenses, the formula for percentage change is a staple of financial analysis.

Percentage Change = [(New Value – Old Value) / Old Value] × 100

If the price of a gallon of gas rises from $3.00 to $3.60, the numerical increase is $0.60. To find the percentage increase: ($0.60 / $3.00) × 100 = 20%. This conversion helps consumers understand the impact of inflation on their purchasing power. Conversely, if a business reduces its overhead from $10,000 to $8,500, it has achieved a 15% reduction in costs, which is a key performance indicator (KPI) for operational efficiency.

Margin vs. Markup: The Entrepreneur’s Essential Conversions

Small business owners often confuse margin and markup, yet converting these numbers correctly is the difference between profit and loss.

- Markup is the percentage added to the cost to reach the selling price. If an item costs $100 and you sell it for $150, your markup is 50%.

- Profit Margin is the percentage of the selling price that is profit. Using the same numbers, your profit is $50, but your margin is ($50 / $150) × 100 = 33.3%.

Understanding how to convert these figures ensures that a business owner doesn’t set prices too low, thinking they have a “50% cushion” when their actual margin is much thinner.

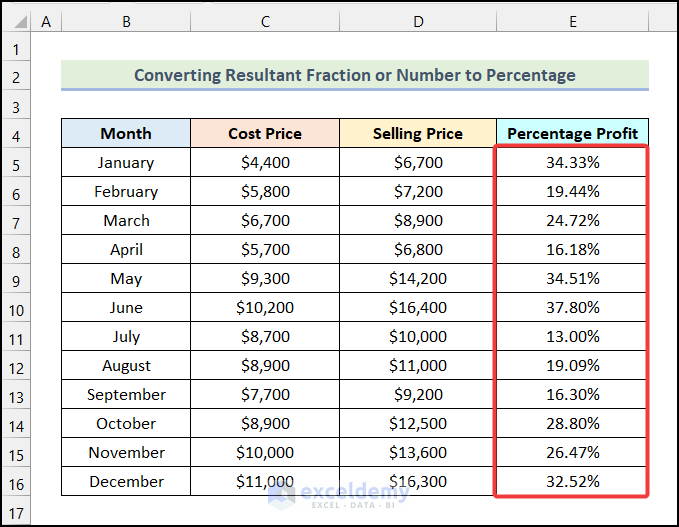

Using Financial Tools to Automate Percentage Conversions

While understanding the manual calculation is vital for financial literacy, modern financial tools allow for the rapid conversion of large datasets. Professional investors and financial planners rely on software to handle these conversions at scale.

Excel and Google Sheets for Budgeting

Spreadsheets are perhaps the most powerful tools for anyone managing money. They have built-in functions that eliminate the need to multiply by 100 manually. In Excel, you can simply divide the “Part” cell by the “Whole” cell and then click the “Percent Style” button in the toolbar. This automatically formats the decimal as a percentage and allows you to adjust the number of decimal places for greater precision.

For example, a “Debt-to-Income” spreadsheet would use a formula like =SUM(Monthly_Debts)/SUM(Monthly_Income). By formatting the resulting cell as a percentage, an individual can instantly see if they exceed the 36% threshold often used by lenders to determine creditworthiness.

The Power of Compound Interest Calculators

When planning for retirement, converting annual growth rates into long-term projections requires complex calculations. Financial tools like compound interest calculators take a percentage (the expected rate of return) and convert it into a future numerical value. This helps individuals visualize how a 7% average annual return on a $10,000 investment can convert into over $76,000 over 30 years. Seeing the interaction between percentages and time is the cornerstone of long-term wealth strategy.

Avoiding Common Pitfalls in Financial Percentage Calculations

Percentages can be misleading if not interpreted within the correct context. Financial literacy requires not just the ability to calculate a percentage, but the wisdom to understand what that percentage represents.

The Trap of Relative vs. Absolute Change

One of the most common mistakes in financial reporting is focusing on a large percentage change without looking at the absolute dollar amount. For instance, if a penny stock increases from $0.01 to $0.02, it has experienced a 100% increase. While “100% growth” sounds phenomenal, the absolute gain is only one cent. In contrast, a 2% increase in a $500 billion company represents $10 billion in value. When evaluating investment news, always convert the percentages back into raw numbers to see the “weight” of the change.

Why Context is Everything in Financial Reporting

Percentages can also be used to mask poor performance. A company might report a “50% increase in profits,” which sounds excellent. However, if the previous year’s profit was only $1,000, then a 50% increase only brings them to $1,500—hardly enough to sustain a large enterprise.

Furthermore, be wary of “Percentage Points” versus “Percentages.” If an interest rate moves from 4% to 5%, it has increased by one percentage point, but it has actually increased by 25% (since 1 is 25% of 4). In the world of finance and money management, failing to make this distinction can lead to significant errors in projecting interest costs or investment growth.

By mastering the conversion of numbers into percentages, you gain a clearer lens through which to view your financial life. It allows for better comparisons, more accurate budgeting, and a deeper understanding of the forces—like interest, inflation, and ROI—that dictate the movement of wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.