In the world of finance, numbers are rarely useful in isolation. If an investor tells you they made $1,000 in the stock market today, you don’t yet have enough information to determine if that was a successful day. If they invested $1,000,000 to make that $1,000, their return is negligible. However, if they invested $2,000 to make that $1,000, they have achieved a monumental gain. This is why percentages are the true language of money.

Converting a raw number into a percentage allows for a standardized comparison across different asset classes, timeframes, and budget scales. Whether you are tracking the growth of a retirement account, calculating the impact of inflation, or determining your debt-to-income ratio, understanding how to convert numbers to percentages is a fundamental skill for financial literacy.

The Mathematical Foundation: How to Convert Numbers to Percentages

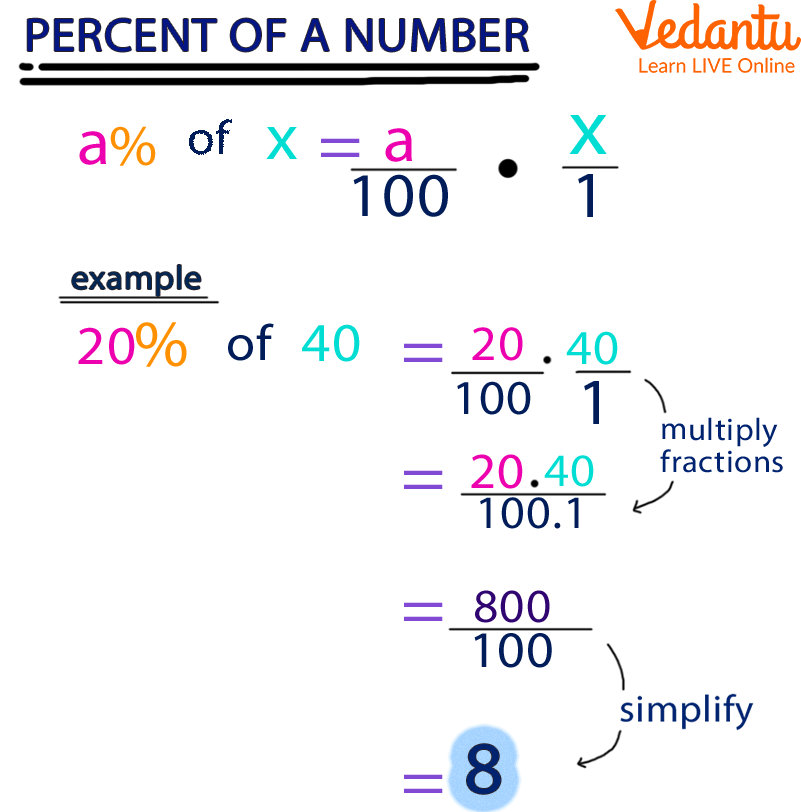

Before applying these concepts to complex investment portfolios, one must master the basic arithmetic. A percentage is simply a way of expressing a number as a fraction of 100. The word “percent” literally stems from the Latin per centum, meaning “by the hundred.”

The Basic Conversion Formula

To convert any number or fraction into a percentage, you follow a simple three-step process:

- Identify the Part and the Whole: Determine the specific value you are analyzing (the “part”) and the total value it is being compared against (the “whole”).

- Divide the Part by the Whole: This calculation results in a decimal. For example, if you saved $20 out of a $100 paycheck, you divide 20 by 100 to get 0.2.

- Multiply by 100: To turn the decimal into a percentage, multiply by 100 (or simply move the decimal point two places to the right) and add the “%” symbol. In our example, 0.2 becomes 20%.

Converting Decimals and Fractions in a Financial Context

In finance, you will often encounter decimals (like bond yields) or fractions (like equity stakes). Converting these is essential for clarity.

- Decimals to Percentages: If a savings account offers a 0.045 interest rate, multiplying by 100 reveals a 4.5% annual percentage yield (APY).

- Fractions to Percentages: If you own 1/8th of a small business, you divide 1 by 8 to get 0.125, which converts to a 12.5% ownership stake.

Analyzing Investment Performance through Percentage Gains

One of the most critical applications of percentage conversion in the “Money” niche is calculating Return on Investment (ROI). Without converting gains into percentages, it is nearly impossible to compare the performance of a high-yield savings account against a volatile stock or a real estate investment.

Calculating ROI and Capital Gains

To calculate the percentage growth of an investment, the formula is slightly more specific:

((Current Value – Original Value) / Original Value) * 100.

Suppose you purchased a share of a tech company for $150 and its current market price is $180. The numerical gain is $30. To find the percentage gain:

- Subtract $150 from $180 to get $30.

- Divide $30 by the original cost of $150, which equals 0.2.

- Multiply by 100 to find a 20% return.

This percentage allows you to compare this stock to other opportunities. If another stock gained $50 but cost $500 to buy, its percentage return is only 10%. Even though the second stock produced more “raw dollars,” the first stock was the superior investment relative to the capital deployed.

The Significance of Annualized Returns and CAGR

While a simple percentage gain tells you how much you made, the Compound Annual Growth Rate (CAGR) tells you how efficiently your money worked over time. Converting total growth into an annualized percentage is how professionals evaluate fund managers. If a portfolio grows by 50% over five years, it sounds impressive. However, converting that to an annualized return reveals a growth rate of approximately 8.4% per year, which is a standard benchmark for the S&P 500.

Percentages in Personal Budgeting and Debt Management

Financial health is often dictated by ratios—which are simply percentages that compare two financial figures. If you cannot convert your income and expenses into percentages, you are managing your money in the dark.

The 50/30/20 Rule: Allocating Your Income

A popular framework for personal finance is the 50/30/20 rule. To apply this, you must convert your net income into specific percentage buckets:

- 50% for Needs: Housing, groceries, and utilities.

- 30% for Wants: Dining out, travel, and hobbies.

- 20% for Savings and Debt Repayment: Building an emergency fund or paying down principal.

By converting your monthly spending into these percentages, you can identify “budget leaks.” If your “Needs” are taking up 70% of your income, you are “house poor,” a realization that is much clearer when viewed as a percentage rather than a raw dollar amount.

Understanding APR and the Cost of Debt

When you take out a loan or use a credit card, the “number” you are charged is the Annual Percentage Rate (APR). Converting this percentage back into a dollar amount helps you understand the true cost of borrowing.

If you carry a $5,000 balance on a credit card with a 24% APR, you can estimate the annual interest cost by converting the percentage back to a decimal (0.24) and multiplying it by the balance ($5,000), which equals $1,200 a year in interest alone. Mastering these conversions allows you to prioritize high-interest debt, which is the single most effective way to improve your net worth.

Business Finance: Margins, Markups, and Profitability

For entrepreneurs and side-hustlers, converting numbers to percentages is the difference between a thriving business and a failing one. Gross and net profit margins are the primary indicators of a company’s health.

Gross Profit Margin vs. Net Profit Margin

A business might have $1 million in sales, but that number is meaningless without knowing the margins.

- Gross Margin: This is calculated by taking (Revenue – Cost of Goods Sold) / Revenue. If it costs $60 to manufacture a product that sells for $100, the gross margin is 40%.

- Net Margin: This is the “bottom line” percentage. It takes into account all expenses, including taxes and overhead. If that same $100 sale results in only $10 of actual profit after all bills are paid, the net margin is 10%.

High-growth companies often focus on increasing these percentages by 1% or 2% through efficiency, as a small percentage shift can result in millions of dollars in additional profit.

The Importance of Percentage Change in Market Trends

In business and investing, we often look at “Year-over-Year” (YoY) or “Quarter-over-Quarter” (QoQ) growth. This is a percentage conversion of the change in a metric. If your side hustle earned $1,000 last month and $1,200 this month, you have a 20% QoQ growth rate. Tracking these percentages helps you identify whether your business is scaling or stagnating, providing a clearer trendline than volatile monthly dollar amounts.

Leveraging Financial Tools for Precision

While manual calculation is vital for conceptual understanding, the modern financial landscape offers tools that automate these conversions. Using technology effectively can prevent the costly errors that often occur with mental math.

Using Spreadsheets for Financial Analysis

Programs like Microsoft Excel and Google Sheets are designed around percentage conversions. By formatting a cell as a “Percentage,” the software automatically handles the multiplication by 100.

- The “Percent Style” Button: In most spreadsheets, selecting a decimal (like 0.07) and clicking the “%” icon instantly converts it.

- Formulas for Variance: You can use formulas like

=(B2-A2)/A2to automatically track the percentage change in your stock portfolio or monthly spending habits.

Avoiding Common Pitfalls: Percentages vs. Percentage Points

One of the most common mistakes in financial reporting is confusing a “percentage change” with a “percentage point change.”

If interest rates rise from 3% to 4%, that is a 1 percentage point increase. However, in terms of the cost of interest, it is a 33.3% increase (1 divided by 3). Understanding this distinction is crucial when reading financial news or bank disclosures. A “small” 1% increase in an interest rate can actually represent a massive percentage increase in your monthly mortgage payment.

Conclusion: The Strategic Value of the Percentage

Converting a number to a percentage is more than a mathematical exercise; it is a strategic lens through which you can view your entire financial life. It allows you to strip away the noise of large or small dollar amounts to see the underlying efficiency of your money. By consistently applying the “part divided by whole” formula, you gain the ability to compare investments, optimize budgets, and manage debt with professional-grade precision. In the pursuit of financial independence, the percentage is your most reliable compass.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.