Understanding how Social Security wages are calculated is a fundamental aspect of personal finance, impacting everything from your current tax obligations to your future retirement benefits. For many, Social Security represents a cornerstone of their financial planning, providing a safety net in old age, disability, or for survivors. Yet, the precise mechanics of how the wages contributing to this system are determined often remain a mystery. This guide aims to demystify the process, offering a clear, professional, and insightful look into the calculation of Social Security wages for both employees and the self-employed.

At its core, Social Security is an earned benefit program, funded primarily through dedicated payroll taxes. The amount you pay into the system, directly tied to your “Social Security wages,” dictates the level of benefits you (and potentially your family) will receive down the line. Grasping these calculations isn’t just about compliance; it’s about informed financial decision-making and ensuring your earnings record accurately reflects your contributions to this vital program.

Understanding the Fundamentals of Social Security Wages

Before diving into the numbers, it’s crucial to grasp the foundational concepts that underpin Social Security wage calculations. These principles define what income is considered, how much of it is subject to taxation, and the broader mechanism of funding.

What Qualifies as “Wages” for Social Security?

The term “wages” for Social Security purposes is broader than many assume, encompassing most forms of remuneration an employee receives from an employer. This typically includes:

- Cash wages: Your regular salary, hourly pay, commissions, bonuses, and tips (if reported to your employer).

- Non-cash payments: The fair market value of goods, lodging, or services provided by an employer in lieu of cash wages.

- Certain fringe benefits: While many fringe benefits are tax-exempt for income tax purposes, some, like employer-provided group term life insurance above a certain limit, can be considered Social Security wages.

- Vacation pay, sick pay, and severance pay: These are generally subject to Social Security taxes.

It’s important to note that certain types of income are not counted as Social Security wages, such as some employer contributions to qualified retirement plans, health insurance premiums paid by an employer, or specific expense reimbursements. The distinction is critical because only wages subject to Social Security tax contribute to your earnings record and, consequently, your future benefits.

The Role of the Social Security Wage Base

Perhaps the most significant concept in Social Security wage calculation is the Social Security wage base (also known as the maximum taxable earnings). This is an annually adjusted cap on the amount of earnings subject to Social Security tax. For any given year, once an individual’s earnings reach this limit, no further Social Security tax is withheld or paid on earnings above that threshold.

For example, if the wage base for a particular year is $168,600 (as it is in 2024), and an individual earns $200,000, only the first $168,600 of their earnings will be subject to Social Security tax. Earnings above this amount are not taxed for Social Security, nor do they count towards your Social Security earnings record for benefit calculation purposes. This wage base is adjusted each year to account for changes in the national average wage index. There is no wage base limit for Medicare taxes; all earned income is subject to Medicare tax.

FICA Taxes: The Funding Mechanism

Social Security and Medicare are primarily funded through the Federal Insurance Contributions Act (FICA) tax. When you see “FICA” on your pay stub, it represents your contribution to both programs. The FICA tax rate is divided as follows:

- Social Security tax: 12.4% on earnings up to the annual wage base.

- Medicare tax: 2.9% on all earnings, with no wage base limit.

For employees, this 12.4% Social Security tax is split evenly between the employee and the employer. Each pays 6.2%. The 2.9% Medicare tax is also split, with each paying 1.45%. This means an employee sees 7.65% (6.2% + 1.45%) withheld from their paycheck, and their employer pays an additional 7.65% on their behalf. This “matching” contribution from employers is a critical component of the system.

Step-by-Step Calculation for Employees

Calculating your Social Security wages as an employee is relatively straightforward, primarily involving identifying your gross earnings and applying the annual wage base limit.

Identifying Your Gross Wages

The first step is to determine your gross wages for the pay period. This is your total earnings before any deductions for taxes, insurance premiums, retirement contributions, or other items. Your pay stub will clearly show your gross pay. For the purpose of Social Security, it’s the cumulative gross wages throughout the year that matter. Employers are responsible for tracking these cumulative wages.

Applying the Social Security Wage Base Limit

Once you have your gross wages, the next step is to apply the Social Security wage base limit. This is typically handled automatically by your employer’s payroll system. As you earn throughout the year, Social Security taxes are withheld from your gross pay. However, once your year-to-date earnings reach the annual wage base, your employer will stop withholding Social Security tax from any subsequent paychecks for that year. Medicare tax withholding will continue on all earnings.

For example, if the wage base is $168,600, and you earn $10,000 per month:

- For the first 16 months ($160,000 total), Social Security tax will be withheld.

- In the 17th month, you earn another $10,000. Your cumulative earnings reach $170,000. Social Security tax will only be withheld on the first $8,600 of that month’s earnings (to reach the $168,600 limit). No Social Security tax will be withheld on the remaining $1,400 for that month, or on any earnings in subsequent months of that year.

Calculating the Employee’s Contribution (6.2%)

With the Social Security taxable wages identified, calculating your direct contribution is simple: multiply the taxable wages (up to the wage base) by the employee’s Social Security tax rate of 6.2%. This is the amount that will be withheld from your paycheck. Your employer will then pay their matching 6.2% on those same wages.

It’s worth noting that if an employee inadvertently has too much Social Security tax withheld (e.g., if they worked for multiple employers and collectively exceeded the wage base without each employer realizing), they can claim a credit for the excess withholding on their income tax return.

Social Security Wages for Self-Employed Individuals

The calculation process differs significantly for self-employed individuals, who are responsible for both the employee and employer portions of FICA taxes. This is commonly referred to as the Self-Employment Contributions Act (SECA) tax.

Net Earnings from Self-Employment (NESE)

For the self-employed, the starting point isn’t “wages” but Net Earnings from Self-Employment (NESE). This is generally the net profit from your business activity, calculated as your gross income from your trade or business minus all ordinary and necessary business expenses.

However, there’s a specific adjustment: you don’t pay SECA tax on 100% of your NESE. Instead, the law allows you to deduct one-half of your self-employment tax when calculating your NESE for Social Security and Medicare purposes. This effectively mirrors the employer’s deduction of their half of FICA taxes. Thus, you pay SECA tax on 92.35% of your NESE.

The SECA Tax and its Components

Self-employed individuals pay the full FICA tax rate of 15.3% (12.4% for Social Security + 2.9% for Medicare) on their net earnings from self-employment. This 15.3% is applied to the 92.35% of NESE, up to the Social Security wage base for the Social Security portion. The Medicare portion (2.9%) is applied to all 92.35% of NESE, without a limit.

Calculating Self-Employment Contributions

Let’s illustrate with an example:

Suppose a self-employed individual has $100,000 in NESE for a year when the wage base is $168,600.

- Calculate taxable NESE: $100,000 * 0.9235 = $92,350.

- Apply Social Security wage base: Since $92,350 is less than the $168,600 wage base, all of it is subject to Social Security tax.

- Calculate Social Security tax: $92,350 * 0.124 (12.4%) = $11,451.40.

- Calculate Medicare tax: $92,350 * 0.029 (2.9%) = $2,678.15.

- Total SECA Tax: $11,451.40 + $2,678.15 = $14,129.55.

Self-employed individuals typically pay estimated taxes quarterly to cover their SECA tax obligations, along with their income tax. This ensures they meet their tax responsibilities throughout the year rather than facing a large bill at tax time.

Impact of Social Security Wages on Future Benefits

The accuracy and consistency of your reported Social Security wages are paramount, as they directly influence the level of benefits you will receive in retirement, in case of disability, or for your survivors.

How Your Earnings Record is Maintained

The Social Security Administration (SSA) maintains an earnings record for every individual who works and pays FICA or SECA taxes. This record meticulously tracks your taxed earnings throughout your working life. Each year, your employer (or you, if self-employed) reports your Social Security taxable wages to the SSA. It is crucial to regularly review your Social Security Statement to ensure your earnings record is accurate. Discrepancies can lead to lower benefits later on.

The Importance of “Credits”

To qualify for Social Security benefits, you need to earn a certain number of “credits.” In 2024, you earn one credit for each $1,730 of earnings, up to a maximum of four credits per year. Most people need 40 credits (10 years of work) to be “fully insured” for retirement benefits. The number of credits required for disability or survivor benefits can be less, depending on age and circumstances. Your Social Security wages are the basis for earning these credits.

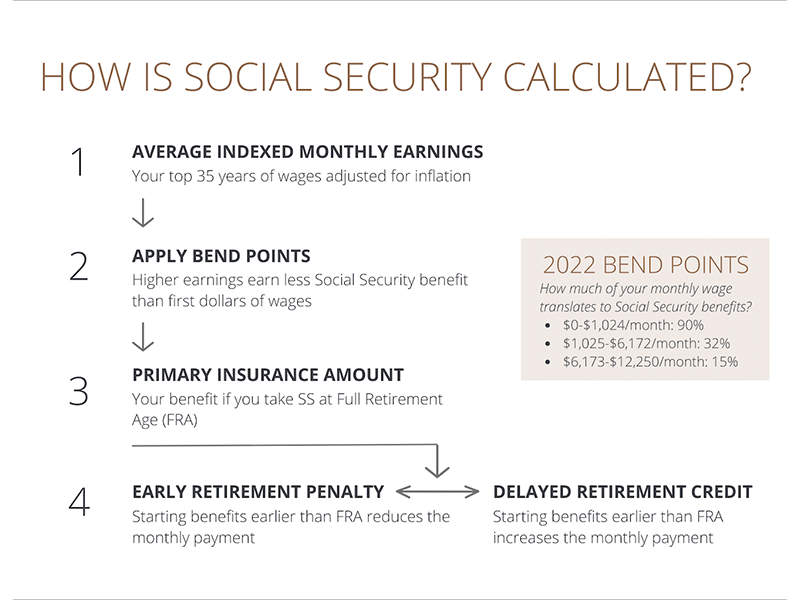

Average Indexed Monthly Earnings (AIME) and Primary Insurance Amount (PIA)

Your Social Security benefit amount is primarily determined by your Average Indexed Monthly Earnings (AIME). The SSA uses your highest 35 years of indexed earnings to calculate your AIME. “Indexed” means that your past earnings are adjusted to account for changes in the national average wage level over time, bringing their value up to closer to current levels. This indexing ensures that earlier earnings reflect their relative value at the time they were earned.

Once your AIME is calculated, it is then used in a formula to determine your Primary Insurance Amount (PIA). Your PIA is the amount of your monthly Social Security benefit if you claim benefits at your Full Retirement Age (FRA). Claiming benefits before or after your FRA will result in a lower or higher monthly benefit, respectively, but the PIA is the starting point. Thus, the higher your Social Security wages over your career, the higher your AIME and, consequently, your PIA and monthly benefit.

Common Misconceptions and Important Considerations

Navigating Social Security wage calculations can be complex, and several common misconceptions often arise. Being aware of these can help you better manage your financial future.

What Isn’t Counted as Social Security Wages?

Beyond the specific exclusions mentioned earlier (like certain fringe benefits or retirement contributions), it’s important to remember that investment income (e.g., dividends, interest, capital gains) and passive income generally are not considered Social Security wages. Only earned income from employment or self-employment contributes to your Social Security earnings record. This distinction highlights why diverse income streams are crucial for comprehensive financial planning, as not all income contributes to every safety net.

The Annual Wage Base Adjustment

The Social Security wage base is not static; it is adjusted annually based on the increase in the national average wage index. This adjustment reflects economic growth and inflation, ensuring the system remains relevant to current earning levels. Staying informed about the current year’s wage base is essential for both employers and high-earning individuals to accurately calculate their contributions. These adjustments are typically announced in October or November for the upcoming year.

Reviewing Your Social Security Statement

The single most important action you can take to ensure your Social Security wages are accurately recorded is to regularly review your Social Security Statement. This statement, accessible online via your my Social Security account at SSA.gov, provides a detailed summary of your earnings history, estimated future benefits, and how many credits you’ve accumulated. It’s recommended to review this statement annually, especially if you change jobs, have multiple employers, or are self-employed. Any errors should be reported to the SSA promptly, as correcting them becomes more difficult the further back in time the error occurred.

In conclusion, calculating Social Security wages involves understanding the definitions of taxable income, applying annual limits, and differentiating between employee and self-employment contributions. These calculations are more than just numbers on a pay stub; they are the bedrock of your future financial security, directly impacting your eligibility and the amount of benefits you and your loved ones may receive from one of the nation’s most critical social programs. A proactive approach to understanding and verifying these wages is a testament to sound personal financial management.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.