Interest is the fundamental “price” of money. Whether you are building a retirement nest egg or managing a mortgage, interest is the invisible force that either accelerates your wealth or complicates your debt. Understanding how to calculate interest is not merely an academic exercise in mathematics; it is a critical life skill that empowers you to make informed decisions about your financial future.

In the world of personal finance, interest functions in two primary ways: as a reward for lending your money (savings and investments) and as a cost for borrowing money (loans and credit cards). By mastering the formulas and logic behind these calculations, you can move from being a passive participant in the economy to a strategic architect of your own net worth.

Understanding the Fundamentals: Simple Interest vs. Compound Interest

Before diving into complex spreadsheets, one must distinguish between the two primary ways interest is calculated. The distinction between simple and compound interest is often the difference between a modest return and exponential growth.

The Simple Interest Formula

Simple interest is the most straightforward method of calculation. It is determined by multiplying the daily interest rate by the principal by the number of days that elapse between payments. Simple interest is most commonly used in short-term personal loans and certain types of consumer car loans.

The formula for simple interest is:

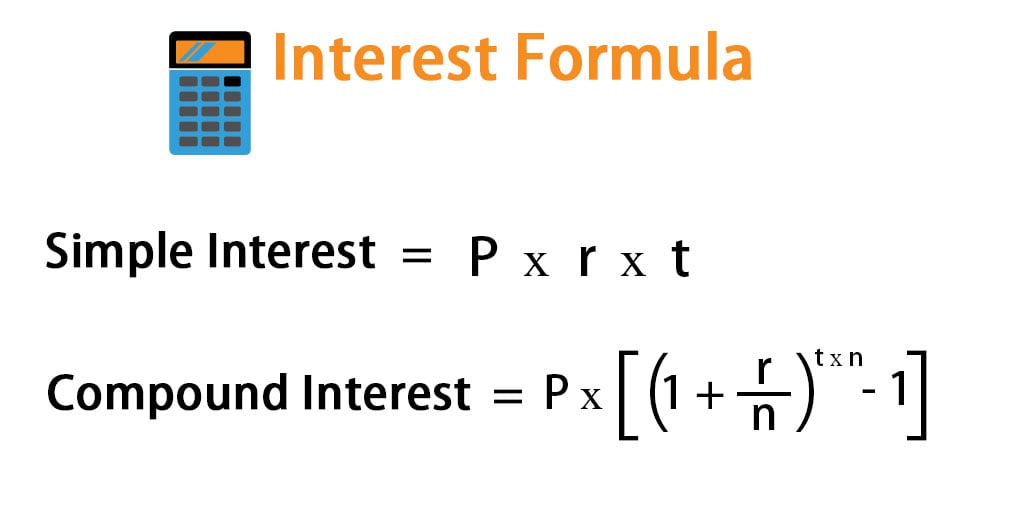

Interest = P × r × t

(Where P = Principal amount, r = Annual interest rate, and t = Time in years)

For example, if you borrow $10,000 at a 5% simple interest rate for three years, the interest would be $1,500 ($10,000 × 0.05 × 3). At the end of the term, you would pay back a total of $11,500. While easy to calculate, simple interest does not account for the “interest on interest” phenomenon that defines modern wealth building.

The Power of Compounding

Compound interest is often referred to as the “eighth wonder of the world.” Unlike simple interest, compound interest is calculated on the initial principal and also on the accumulated interest of previous periods. This creates a snowball effect where your money grows at an accelerating rate.

In the context of personal finance, compounding is your greatest ally when saving for long-term goals like retirement. When you earn interest on a savings account, that interest is added to your balance. In the next period, you earn interest on that new, larger balance. Over decades, this process can turn modest monthly contributions into a substantial fortune.

The Mechanics of Calculation: Tools and Mathematical Models

While the concept of interest is intuitive, the actual calculation requires precision. Depending on the financial instrument—be it a high-yield savings account or a corporate bond—the frequency of compounding can significantly alter the final result.

Manual Calculation and the Compound Interest Formula

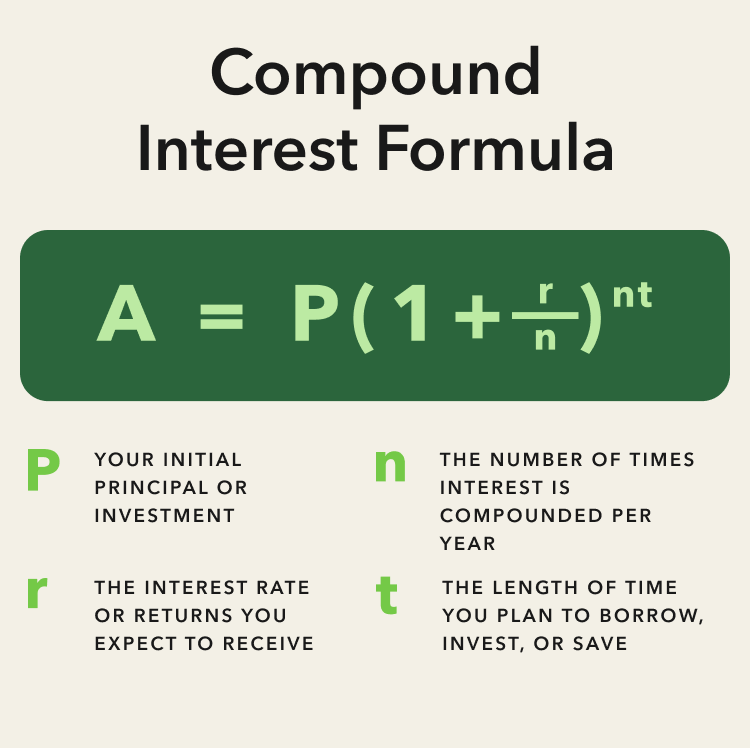

To calculate the future value of an investment with compounding interest, we use a more sophisticated formula:

A = P (1 + r/n)^(nt)

- A = the total amount of money accumulated after n years, including interest.

- P = the principal investment amount (the initial deposit).

- r = the annual interest rate (decimal).

- n = the number of times that interest is compounded per year.

- t = the number of years the money is invested or borrowed for.

If you have $5,000 in a savings account with a 4% interest rate compounded monthly (n=12), after 10 years, your balance would not be a mere $7,000 (simple interest). Instead, it would be approximately $7,454.16. That extra $454.16 is the “magic” of compounding.

Utilizing Financial Tools and Excel

In the modern era, you don’t need to carry a scientific calculator to manage your money. Software like Microsoft Excel and Google Sheets provides built-in functions to handle these calculations. The most common function is =FV(rate, nper, pmt, [pv], [type]), which calculates the Future Value of an investment.

Professional financial planners also use “Amortization Schedules” to help clients understand how interest is applied to long-term debt. These tools break down every single payment of a loan, showing exactly how much goes toward the principal and how much is consumed by interest. Early in a loan term, the majority of your payment goes toward interest; as the principal decreases, more of your payment begins to chip away at the actual debt.

Interest in Action: Mortgages, Savings, and Credit Cards

Interest behaves differently depending on the financial product. To truly understand how to calculate interest, one must look at how these formulas are applied in real-world scenarios.

Real Estate and Amortization

When you take out a 30-year fixed-rate mortgage, the interest calculation is based on the remaining principal balance each month. This is why “extra payments” toward the principal are so effective. By reducing the principal faster than the bank’s schedule, you lower the base upon which the interest is calculated for every subsequent month. Over 30 years, paying just one extra monthly payment per year can shave years off your mortgage and save you tens of thousands of dollars in interest costs.

The High Cost of Revolving Credit

Credit cards use a specific type of interest calculation known as the “Average Daily Balance” method. Because credit card interest (APR) is typically very high (often between 18% and 29%), the interest is often calculated daily.

To find your daily periodic rate, you divide your APR by 365. If you carry a balance of $5,000 at 24% APR, you are being charged roughly $3.28 in interest every single day. This is why credit card debt is so corrosive to personal wealth—the compounding works against you at a much faster rate than it works for you in a savings account.

Advanced Concepts: APR vs. APY

A common point of confusion for many consumers is the difference between APR (Annual Percentage Rate) and APY (Annual Percentage Yield). While they sound similar, they serve different purposes and provide different perspectives on the cost or gain of money.

What is APR?

The Annual Percentage Rate represents the annual cost of borrowing money, including fees. However, APR does not account for the compounding of interest within the year. It is a “nominal” rate. When you see an APR on a car loan or a credit card, it tells you the simple interest rate applied over a year. Because it ignores compounding, it often makes the cost of debt look slightly lower than it actually is if the balance is carried forward.

Understanding APY and the Effective Annual Rate

The Annual Percentage Yield (APY) is the “effective” rate. It takes into account the effects of intra-year compounding. This is the figure you should look at when comparing savings accounts or Certificates of Deposit (CDs).

If a bank offers a 5% interest rate compounded daily, the APY will actually be 5.13%. While a 0.13% difference might seem negligible, on a $100,000 balance, that is an extra $130 per year for doing nothing. When you are the one earning the money, you want the APY to be as high as possible. When you are borrowing, you want to look past the APR to see the “Effective Interest Rate” to understand your true costs.

Strategies for Optimizing Your Financial Health

Understanding how interest is calculated is the first step toward financial mastery. The second step is applying that knowledge to optimize your personal balance sheet.

Maximizing Returns on Savings

To make interest work for you, you must focus on two variables: the rate (APY) and the frequency of compounding. In a low-interest environment, many people leave their money in traditional “big bank” savings accounts earning 0.01%. By calculating the opportunity cost, you can see that moving $20,000 to a High-Yield Savings Account (HYSA) earning 4.5% APY would result in $900 of passive income per year, versus only $2 in a traditional account.

Furthermore, “laddering” investments like CDs allows you to capture higher interest rates over longer terms while maintaining some liquidity. By understanding the math, you can ensure your emergency fund is not just sitting idle but is actually growing.

Minimizing Interest Expense on Debt

On the flip side of the coin, managing interest expense is about “Debt Avalanche” and “Refinancing.” The Debt Avalanche method suggests paying off the debt with the highest interest rate first, regardless of the balance. Mathematically, this is the most efficient way to reduce the total interest paid over time.

Additionally, knowing how to calculate interest allows you to evaluate refinancing opportunities. If you have a private student loan at 8% and can refinance to 5%, you aren’t just saving 3%—you are significantly reducing the amount of interest that compounds over the life of the loan.

In conclusion, interest is the heartbeat of the financial system. It can be a relentless headwind that keeps you in a cycle of debt, or a powerful tailwind that carries you toward financial independence. By learning to calculate it, analyze it, and respect its power, you gain the ultimate tool for navigating the complexities of the modern economy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.