Compound interest has often been called the “eighth wonder of the world.” While that might sound like hyperbole, for anyone who has seen a modest investment transform into a significant fortune over several decades, the description feels entirely accurate. At its core, compound interest is the process where the interest you earn on your money is reinvested, resulting in you earning interest on your interest.

In the world of personal finance and investing, understanding how to calculate and leverage compound interest is perhaps the single most important skill a person can possess. Whether you are planning for retirement, saving for a home, or looking to understand the true cost of debt, the mechanics of compounding will dictate your financial trajectory.

The Mathematical Foundation: Understanding the Formula

To calculate compound interest accurately, you must move beyond the basic addition used in simple interest. Simple interest is calculated only on the principal amount—the initial sum of money deposited. Compound interest, however, is calculated on the principal amount plus all the accumulated interest from previous periods.

The Standard Compound Interest Formula

The most common way to calculate the future value of an investment with compounding interest is by using the following formula:

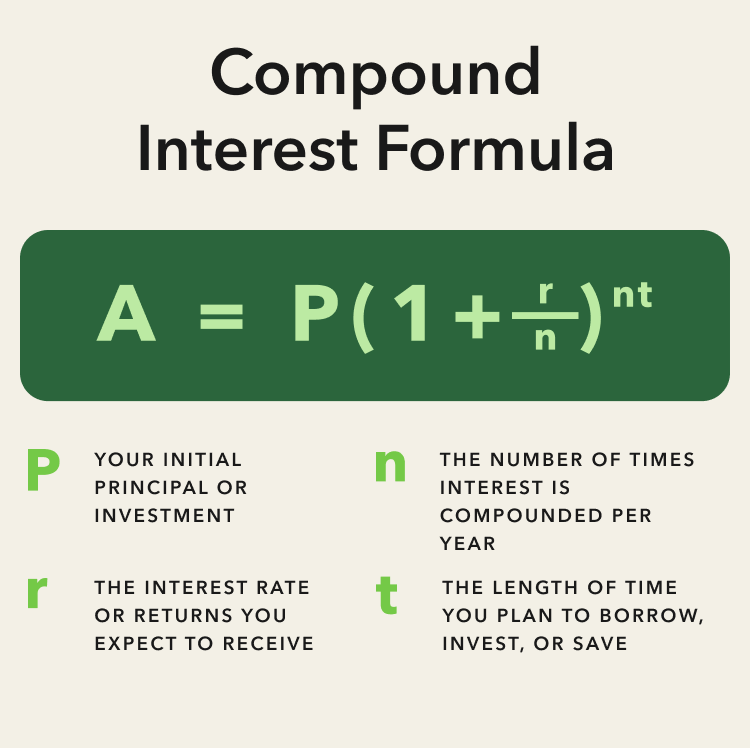

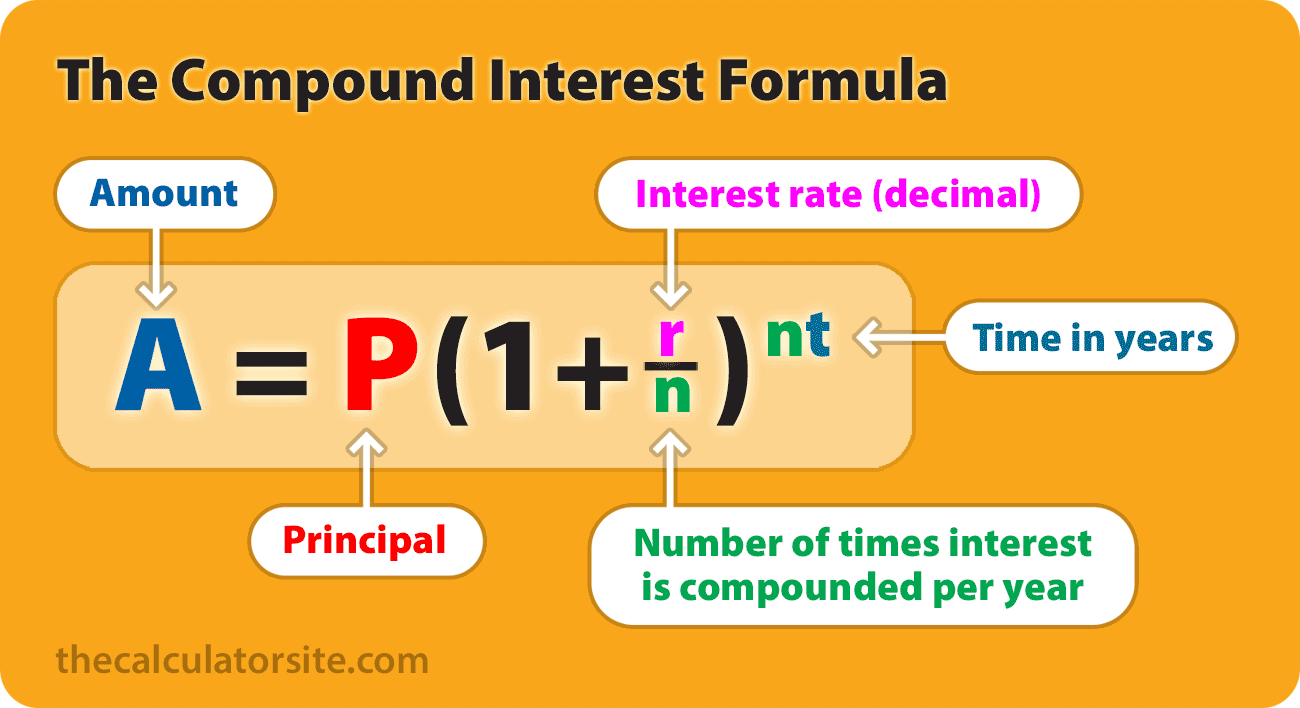

A = P (1 + r/n)^(nt)

In this equation:

- A represents the final amount of money that will be accumulated after the specified time, including interest.

- P is the principal amount (the initial sum of money you start with).

- r is the annual interest rate (decimal).

- n is the number of times that interest is compounded per year.

- t is the number of years the money is invested or borrowed for.

Breaking Down the Variables

Understanding each component of this formula is crucial for making informed financial decisions. The Principal (P) is your starting point; the higher it is, the more significant the absolute growth will be. The Annual Interest Rate (r) is often the variable people focus on most, but it is heavily influenced by the Compounding Frequency (n).

The Time (t) variable is arguably the most powerful. Because it sits as an exponent in the formula, its impact is exponential rather than linear. This is why financial advisors emphasize starting early; adding five years to your investment horizon can have a more profound impact on the final total than doubling your initial principal.

Manual Calculation vs. Financial Tools

While understanding the formula allows you to perform manual calculations using a scientific calculator, most modern investors utilize financial tools. Excel and Google Sheets offer the FV (Future Value) function, which automates this process. For a quick “mental math” check, many professionals use the Rule of 72. By dividing 72 by your annual interest rate, you can approximate how many years it will take for your initial investment to double.

The Variable of Frequency: How Compounding Intervals Change Results

One of the most overlooked aspects of calculating compound interest is the frequency at which the interest is applied. The “n” in our formula represents this frequency, and it can drastically alter the outcome of an investment over a long period.

Common Compounding Intervals

In the financial world, interest is typically compounded in one of the following ways:

- Annually: Interest is calculated and added once a year.

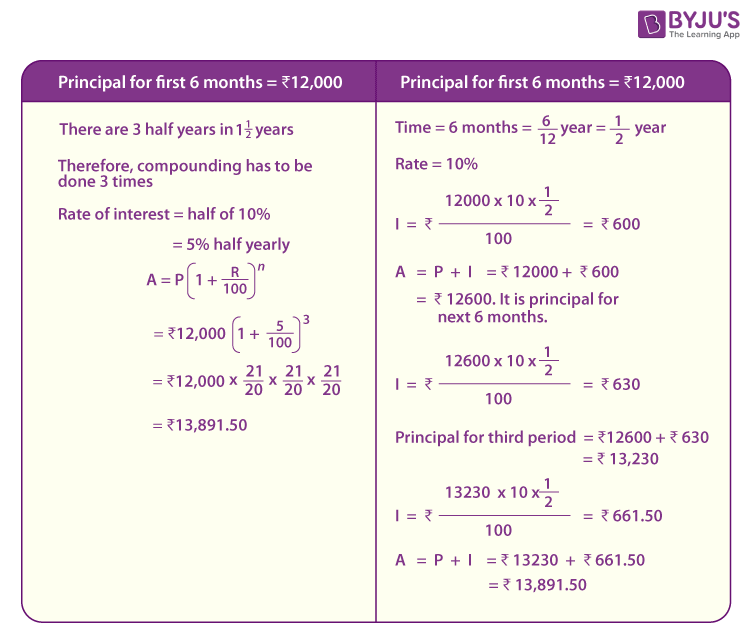

- Semi-annually: Interest is added every six months.

- Quarterly: Common for many savings accounts and corporate bonds.

- Monthly: Standard for most credit cards and mortgages.

- Daily: Used by high-yield savings accounts and some fintech platforms.

The Impact of Increased Frequency

The more frequently interest is compounded, the faster the principal grows. This is because the interest earned in the first period begins earning its own interest in the second period. For example, if you have $10,000 at a 5% interest rate, annual compounding would leave you with $10,500 after one year. However, if that same 5% were compounded daily, you would end the year with slightly more because the tiny increments of interest added each day would themselves earn interest the following day.

While the difference between monthly and daily compounding might seem negligible on a small balance over one year, it becomes substantial when dealing with hundreds of thousands of dollars over thirty years.

APY vs. APR: Knowing the Difference

When comparing financial products, you will often see two terms: Annual Percentage Rate (APR) and Annual Percentage Yield (APY). APR represents the simple interest rate over a year without taking compounding into account. APY, however, reflects the actual amount of interest you will earn (or pay) because it includes the effect of compounding. When calculating your potential returns, always look for the APY to get the most accurate picture of your growth.

Strategic Applications: Compounding in Investing and Wealth Building

Calculating compound interest isn’t just a mathematical exercise; it is a strategic tool used to build long-term wealth. By understanding the formula, you can better structure your portfolio to take advantage of different financial vehicles.

Retirement Accounts and Tax Deferral

Vehicles such as the 401(k) and the Individual Retirement Account (IRA) are designed specifically to maximize compound interest. By allowing your investments to grow tax-deferred (or tax-free in the case of a Roth IRA), you prevent “leakage.” In a standard brokerage account, you might have to pay capital gains taxes annually on dividends or realized gains, which reduces the amount of principal available to compound. In a retirement account, every penny of interest remains in the account to fuel further growth.

Dividend Reinvestment Plans (DRIPs)

For stock market investors, compound interest is often realized through Dividend Reinvestment Plans. When a company pays a dividend, instead of taking that money as cash, the investor uses it to purchase more shares of the stock. This increases the number of shares owned, which in turn increases the next dividend payment. This creates a “snowball effect” that is the equity market’s version of compounding interest.

The High-Yield Savings Advantage

In a low-interest-rate environment, the power of compounding is muted. However, in a high-interest-rate environment, high-yield savings accounts (HYSAs) become powerful tools. By calculating the yield over a five-year period, an investor can see that a 4.5% APY compounded monthly offers a risk-free return that can serve as a potent foundation for an emergency fund or a short-term savings goal.

The Inverse Reality: When Compound Interest Works Against You

While compound interest is a friend to the saver, it is the enemy of the debtor. Understanding how to calculate the cost of interest is vital for maintaining financial health, particularly when dealing with high-interest consumer debt.

Credit Card Compounding

Credit cards are perhaps the most dangerous application of compound interest for the average consumer. Most credit card issuers compound interest daily. This means that if you carry a balance, the interest charged today will be added to your balance tomorrow, and you will be charged interest on that interest the day after.

If you have a $5,000 balance at a 24% APR, the daily periodic rate is roughly 0.065%. While that seems small, the daily compounding ensures that the debt grows at an aggressive pace. Calculating the “cost of carry” helps many consumers realize that paying off high-interest debt is equivalent to a guaranteed 24% return on investment.

Mortgages and Amortization

Mortgages also utilize a form of compounding, though it is structured through an amortization schedule. In the early years of a 30-year mortgage, the vast majority of your monthly payment goes toward interest rather than principal. By making one extra payment per year—essentially reducing the principal upon which future interest is calculated—you can shave years off the loan and save tens of thousands of dollars in interest. This is “reverse compounding” in action.

Student Loans and Capitalization

For students, understanding “interest capitalization” is essential. This occurs when unpaid interest is added to the principal balance of the loan, usually after a period of deferment or forbearance. Once the interest capitalizes, the new, larger principal balance begins to accrue interest. Calculating this ahead of time can encourage students to pay off the interest as it accrues, preventing the loan from “ballooning” out of control.

Optimizing Your Financial Future Through Calculation

The ability to calculate compound interest provides a level of financial clarity that few other skills can match. It allows you to move away from guesswork and toward data-driven decision-making.

The Importance of the “Time” Factor

If there is one takeaway from the compound interest formula, it is that time is the most valuable asset. An investor who starts at age 25 and stops at 35, leaving the money to compound for another 30 years, will often end up with more money than someone who starts at age 35 and contributes every year until age 65. When you run the numbers, you see that the “cost of waiting” is incredibly high.

Using Calculations to Set Realistic Goals

By using the compound interest formula, you can reverse-engineer your financial goals. If you know you want $1,000,000 in 30 years and you expect a 7% annual return, you can calculate exactly how much you need to contribute monthly. This transforms a vague dream of “being rich” into a concrete, actionable monthly budget item.

Final Thoughts on Financial Literacy

Calculating compound interest is more than just plugging numbers into an equation; it is about understanding the momentum of money. In a world of instant gratification, compounding rewards the patient and the disciplined. By mastering these calculations, you gain the “financial goggles” necessary to see through the marketing of high-interest loans and recognize the long-term potential of consistent, early investing. Whether you are using a spreadsheet or the Rule of 72, keep the math of compounding at the center of your financial strategy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.