In the contemporary financial landscape, the methodology of exchanging value has undergone a radical transformation. Gone are the days when settling a dinner bill or splitting the rent required a physical trip to an ATM or the cumbersome writing of a paper check. Today, the “Peer-to-Peer” (P2P) payment ecosystem is dominated by agile platforms that prioritize speed, convenience, and social connectivity. Among these, Venmo has emerged as a titan, particularly within the North American market. Understanding how to receive money on Venmo is no longer just a technical skill; it is a fundamental component of modern personal finance management.

Understanding the Venmo Ecosystem for Personal Finance

To effectively use Venmo as a financial tool, one must first understand its position within your broader economic portfolio. Venmo functions as a digital wallet—a middle ground between your traditional bank account and the point of transaction.

The Shift from Cash to Peer-to-Peer (P2P) Payments

The transition toward a cashless society has been accelerated by the demand for “frictionless” transactions. For the individual, this means liquidity is no longer tied to the physical presence of currency. Receiving money on Venmo represents a digital ledger entry that carries real-world purchasing power. This shift has significant implications for how we track our spending and income. When you receive money digitally, you create an automatic audit trail, which is a cornerstone of disciplined financial planning.

Why Venmo is a Core Tool for Financial Organization

Unlike traditional banking apps that can feel cold and purely transactional, Venmo integrates a social layer that simplifies the awkwardness of debt collection among peers. For the budget-conscious individual, Venmo serves as a secondary reservoir of funds. By maintaining a Venmo balance, users can segregate “lifestyle” money (reimbursements for coffee, movies, or dining) from their primary checking accounts used for fixed costs like mortgages or insurance. This categorization is a subtle but powerful way to manage discretionary spending.

How to Receive Money on Venmo: Step-by-Step Logistics

Receiving funds on Venmo is designed to be intuitive, but there are several nuances to the process that can ensure your money arrives safely and is managed efficiently.

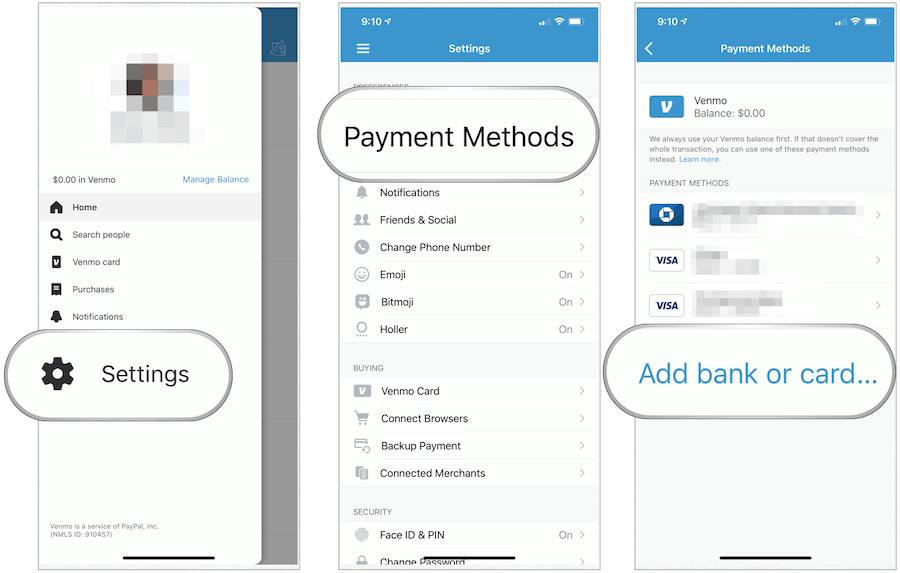

Setting Up Your Account for Seamless Transactions

Before you can receive a single cent, your account must be properly configured. This involves more than just downloading the app. To ensure that the money you receive is actually usable, you must verify your identity under “Know Your Customer” (KYC) regulations. This is a federal requirement for financial institutions to prevent money laundering.

- Link a Funding Source: While you are receiving money, having a verified bank account linked is essential for eventually “cashing out.”

- Profile Optimization: Ensure your profile picture is clear and your username is unique. This prevents “mistransactions,” where a sender might accidentally send funds to a stranger with a similar name—a mistake that is often difficult to reverse in the digital space.

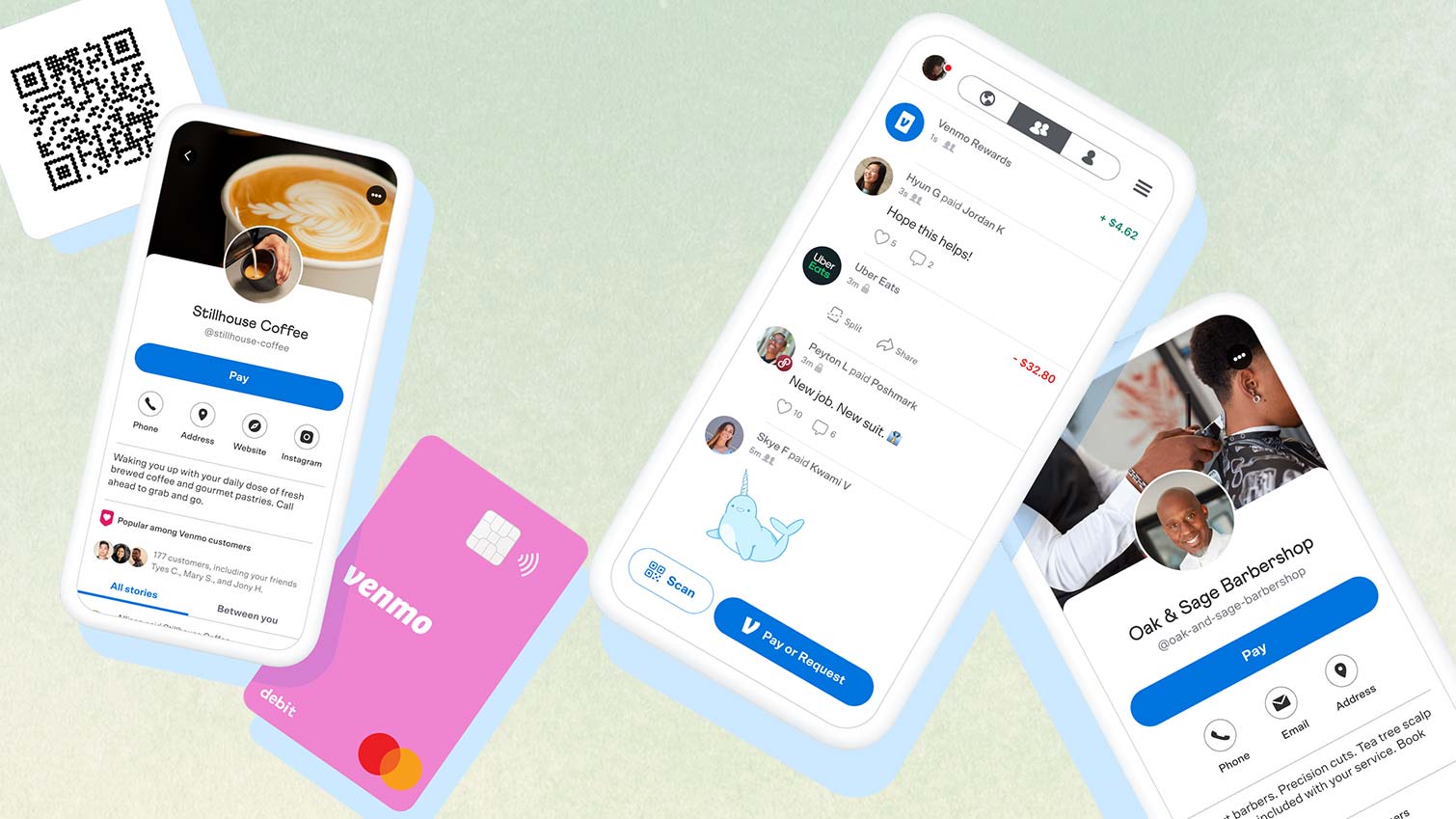

Sharing Your Identity: QR Codes, Usernames, and Links

Venmo provides three primary ways to facilitate an incoming payment:

- The Venmo Username: You can provide your @username to a sender. This is the most common method but carries the highest risk of typos.

- The QR Code: Within the app, you can display a personal QR code. This is the “gold standard” for security and accuracy. When a sender scans your code, your profile is pulled up instantly, eliminating the risk of manual entry errors.

- Scan and Pay Links: For those operating side hustles or small ventures, you can send a direct Venmo link via text or email. This removes hurdles for the sender, making it more likely you will be paid promptly.

Confirming Incoming Payments and Notifications

Once a sender initiates a payment, the funds typically appear in your Venmo balance instantaneously. However, a common pitfall in digital finance is the “notification trap.” Never assume you have received money based solely on an email or text notification, as these can be spoofed by scammers. Always open the official Venmo app and check your “Transactions” feed to confirm that the balance has increased. Once the money is in your Venmo account, it is held in a “Venmo Balance” until you decide your next move.

Managing Your Venmo Balance: Transfer Options and Fees

Receiving the money is only the first half of the equation. The second half is deciding how that money interacts with your broader financial life. This is where strategic financial decision-making comes into play.

Standard Transfers vs. Instant Transfers: A Cost-Benefit Analysis

Once you have a balance in Venmo, you have two primary ways to move that money into your traditional bank account:

- Standard Bank Transfer: This is free of charge but typically takes 1 to 3 business days to process. From a personal finance perspective, this is the preferred method for non-urgent funds. It requires patience but preserves 100% of your capital.

- Instant Transfer: If you need the funds immediately to cover a bill or an overdrawn account, Venmo offers an instant transfer to eligible debit cards or bank accounts. This carries a fee (currently 1.75%, with a minimum fee of $0.25 and a maximum of $25). While convenient, frequent use of instant transfers can nibble away at your net worth. For a $1,000 rent reimbursement, a $17.50 fee is a high price to pay for 48 hours of speed.

Using Your Balance for Direct Purchases

An alternative to transferring money to a bank is to keep it within the Venmo ecosystem. Many retailers now accept Venmo as a form of payment at checkout. Additionally, the Venmo Debit Card allows you to spend your balance anywhere Mastercard is accepted. This can be an effective way to use “found money” (like birthday gifts or dinner reimbursements) for everyday expenses without touching your main savings.

Advanced Financial Strategies with Venmo

As you become more comfortable receiving money on the platform, you should consider the higher-level financial implications, ranging from tax obligations to group budgeting.

Splitting Expenses and Managing Group Budgets

Venmo’s “Request” feature is a powerful tool for accounts receivable. If you are the person who puts a $500 group Airbnb on your credit card, you are essentially acting as a short-term lender. Using the “Split” feature allows you to automate the calculation and request funds from multiple people simultaneously. This ensures that your personal cash flow isn’t hampered by the slow repayment of others. In the world of finance, “Time Value of Money” is key; the faster you get your money back, the sooner it can be put to work in a high-yield savings account or investment.

Security and Fraud Prevention in Digital Finance

Receiving money from strangers carries inherent risks. A common “Money” niche scam involves a stranger “accidentally” sending you a large sum of money and then asking you to send it back. Often, the original payment was made with a stolen credit card and will eventually be reversed by the bank, leaving you out of pocket for the money you “returned.”

- Professional Tip: Only receive money from people you know and trust. If a stranger sends you money, contact Venmo support directly rather than engaging with the sender.

Tax Implications for High-Volume Receivers (1099-K)

For those using Venmo for side hustles or selling items online, it is crucial to understand the IRS requirements. The tax code regarding P2P payments has evolved. If you receive over a certain threshold (historically $600 in a calendar year) for “Goods and Services,” Venmo is required to issue a Form 1099-K.

It is vital to distinguish between “Personal” payments (splitting a pizza) and “Business” payments. Business payments are taxable income. Keeping these separate in your Venmo records will save significant headaches during tax season and ensure you are compliant with federal financial regulations.

Conclusion: Integrating Venmo into Your Wealth Strategy

Learning how to receive money on Venmo is the gateway to a more fluid and organized financial life. By mastering the mechanics of the app, understanding the fee structures of various transfer methods, and staying vigilant regarding security and tax obligations, you transform a simple app into a sophisticated financial tool.

In the modern era, wealth management is as much about the efficiency of your transactions as it is about the size of your investments. By treating your Venmo account with the same professional scrutiny as your primary brokerage or bank account, you ensure that every dollar received is a dollar that contributes to your overall financial health. Whether you are collecting a debt from a friend or managing the proceeds of a side business, the ability to navigate digital payment platforms is an essential pillar of 21st-century financial literacy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.