In an increasingly digital world, the smartphone has evolved from a mere communication device into a powerful personal assistant, a financial manager, and a gateway to myriad services. Among its most transformative capabilities is the ability to manage and pay bills on the go. Gone are the days of paper checks, stamps, and trips to the post office or bank. Today, paying your bills can be as simple as a few taps on your mobile device. This shift represents not just a convenience, but a fundamental change in how we interact with our financial obligations, driven by innovation in mobile technology, secure software, and user-centric app design.

The core question, “how do I pay my bill on my phone,” is a gateway to understanding the technological ecosystem that enables seamless, secure, and efficient financial transactions from the palm of your hand. It’s about leveraging banking apps, dedicated payment platforms, and robust digital security measures to ensure your money reaches its destination accurately and on time. This guide will delve into the various technological facets that make mobile bill payments possible, providing a comprehensive overview for anyone looking to optimize their financial management through their smartphone.

The Digital Wallet Revolution: Why Pay on Your Phone?

The proliferation of smartphones, coupled with advancements in mobile internet and app development, has ushered in an era where digital wallets and mobile payment solutions are not just novelties but essential tools. Paying bills on your phone is more than just a trend; it’s a practical evolution driven by technological convenience and efficiency. This section explores the underlying reasons and technological enablers behind this widespread adoption.

The Convenience Factor

The primary allure of mobile bill payment lies in its unparalleled convenience. Your phone is almost always with you, making it possible to pay bills anytime, anywhere—whether you’re commuting, waiting in line, or relaxing at home. This ubiquitous access eliminates geographical and temporal barriers that traditionally accompanied bill payment. From a technological standpoint, this convenience is powered by responsive app interfaces, cloud-based data synchronization, and reliable mobile network connectivity (4G, 5G, Wi-Fi). Developers invest heavily in creating intuitive user experiences (UX) and user interfaces (UI) that simplify complex financial transactions into a few straightforward steps, reducing cognitive load and saving precious time. Automated payment reminders, often integrated within these apps, leverage notification technologies to ensure you never miss a due date, further enhancing the user experience.

Accessibility and Control

Beyond convenience, mobile payment technology grants users unprecedented accessibility and control over their finances. For individuals with limited mobility or those in remote areas, a smartphone becomes a powerful financial tool, bridging gaps that traditional banking infrastructure might leave open. Accessibility features integrated into modern operating systems (like VoiceOver for iOS or TalkBack for Android) further empower a broader range of users to manage their bills independently.

Technologically, this control manifests through real-time access to account balances, transaction histories, and immediate payment confirmations. Secure APIs (Application Programming Interfaces) allow banking apps to pull and display up-to-the-minute financial data, giving users a clear picture of their financial standing. The ability to schedule payments, view upcoming bills, and instantly verify payment status provides a level of granular control that traditional methods simply cannot match. This digital command center in your pocket empowers users to take proactive charge of their financial health, supported by a sophisticated network of software and data architecture.

Essential Apps and Platforms for Mobile Bill Payments

The ecosystem for mobile bill payments is rich and diverse, offering multiple avenues through which users can settle their accounts. Each platform leverages distinct technological approaches to facilitate transactions, offering varying degrees of integration and functionality. Understanding these tools is key to selecting the most suitable method for your specific needs.

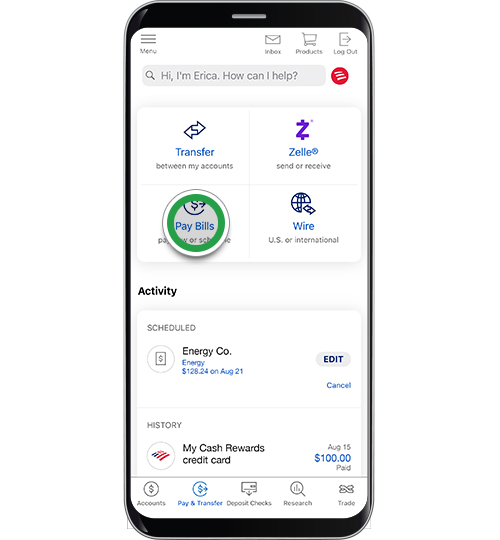

Banking Apps: Your Financial Hub

Most modern banks and credit unions offer robust mobile banking applications for both iOS and Android platforms. These apps are designed to be a comprehensive financial hub, providing secure access to all your accounts, not just for viewing balances but also for executing transactions. Technologically, these apps are built with sophisticated encryption protocols, multi-factor authentication (MFA), and secure API integrations with the bank’s core systems.

Through your bank’s app, you can typically:

- Pay bills directly to registered payees: Banks maintain databases of various utility companies, credit card providers, and other service providers, often allowing direct electronic payments.

- Set up recurring payments: This feature automates regular bill payments, leveraging scheduling algorithms to ensure timely transactions.

- Transfer funds: Move money between your accounts or to external accounts.

- View transaction history: Access detailed records of past payments and deposits.

- Deposit checks: Using your phone’s camera, mobile check deposit features leverage optical character recognition (OCR) and image processing technology to digitize checks.

The security infrastructure behind these apps is paramount, employing advanced data encryption, biometric login options (fingerprint, facial recognition), and session management to protect user data and financial assets.

Dedicated Bill Payment Apps

Beyond individual banking apps, several third-party applications specialize in consolidating and managing all your bills in one place. Examples include Mint, Prism, or Check (now formerly owned by Intuit). These apps aim to simplify financial management by fetching bill details from various providers and presenting them on a single dashboard.

Their technological prowess lies in their ability to securely integrate with numerous service providers (utility companies, telecommunication firms, credit card issuers) through APIs. They often use advanced data aggregation techniques and machine learning algorithms to categorize expenses and predict upcoming bills. While offering immense convenience, it’s crucial to vet the security practices of such apps, as they hold access to multiple sensitive accounts. Reputable apps employ industry-standard encryption, strong authentication, and data privacy policies to safeguard user information.

Utility and Service Provider Apps

Many service providers—from electricity companies to internet providers and mobile carriers—have developed their own dedicated apps. These apps often provide a more tailored experience for managing that specific service account.

Technologically, these apps are focused on providing a direct channel for customer interaction and payment. They often feature:

- Specific bill details: Access to detailed consumption reports, usage statistics, and itemized billing.

- Direct payment options: Integration with various payment gateways to accept credit/debit cards, bank transfers, or even digital wallets like Apple Pay or Google Pay.

- Service management: Features for reporting outages, managing service plans, or contacting customer support, often enhanced with AI-powered chatbots.

Paying directly through these apps can sometimes offer benefits like loyalty programs or specific payment plans unique to the provider.

Third-Party Payment Processors

Platforms like PayPal, Venmo, Zelle, and even Google Pay or Apple Pay offer functionalities that extend to bill payment. While primarily known for peer-to-peer (P2P) transfers or online shopping, many businesses and service providers accept payments through these established digital wallets.

These platforms act as intermediaries, leveraging their robust payment processing infrastructure to facilitate transactions. They employ sophisticated tokenization and encryption methods to protect card details and bank information, allowing users to pay without directly exposing their financial credentials to every merchant. Their convenience lies in their widespread acceptance and the ability to link multiple funding sources to a single digital wallet.

A Step-by-Step Guide to Paying Bills via Your Mobile Device

The actual process of paying a bill on your phone is designed to be intuitive, but understanding the underlying technical flow can enhance confidence and efficiency. This section breaks down the typical steps involved, highlighting the technological elements at play.

Setting Up Your Payment Method

Before you can pay a bill, you need to link a funding source to your chosen app or platform. This usually involves securely inputting your bank account details or credit/debit card information.

- Bank Accounts (ACH): When you link a bank account (checking or savings), the app typically initiates a secure Automated Clearing House (ACH) transfer. This process involves verifying your bank account ownership, often through micro-deposits or by securely logging into your online banking portal via the app’s embedded browser. This ensures that the app can initiate electronic funds transfers from your account.

- Credit/Debit Cards: Adding a card involves securely entering the card number, expiration date, and CVV. Modern apps use secure tokenization services provided by payment gateways (like Stripe, Braintree, or Square) to encrypt and store your card details, replacing them with a unique, non-sensitive token. This token is then used for transactions, meaning your actual card number is never directly transmitted or stored by the merchant or app itself, significantly enhancing security.

- Digital Wallets: If using a digital wallet like Apple Pay or Google Pay, your payment method is already securely stored within the device’s secure element (a dedicated chip designed to protect sensitive data). When you choose this option, the app interfaces with the device’s secure element to authorize the payment using a device-specific account number, rather than your actual card number.

Navigating the Payment Interface

Once your payment method is set up, the process of finding and paying a bill is usually straightforward:

- Login and Authentication: Access your chosen app (bank, dedicated bill pay, or service provider) using your secure credentials, often enhanced with biometric authentication (fingerprint, facial recognition) or a strong PIN. These biometric technologies rely on advanced sensors and algorithms to verify identity, providing a highly secure and convenient login method.

- Locate “Pay Bills” or “Payments”: Most apps feature a clearly labeled section for bill payments. This is typically part of the main navigation or dashboard. The UI/UX design prioritizes ease of discovery.

- Select/Add Payee: If the bill is from a new provider, you’ll usually need to add them as a payee, which involves inputting their name, account number, and sometimes their mailing address. The app’s database and search functionality assist in quickly finding and linking to known billers.

- Enter Payment Details: Input the amount you wish to pay, the payment date (current or scheduled), and select your desired funding source. The app’s backend systems instantly validate the inputs and calculate any applicable fees or minimum/maximum payment limits.

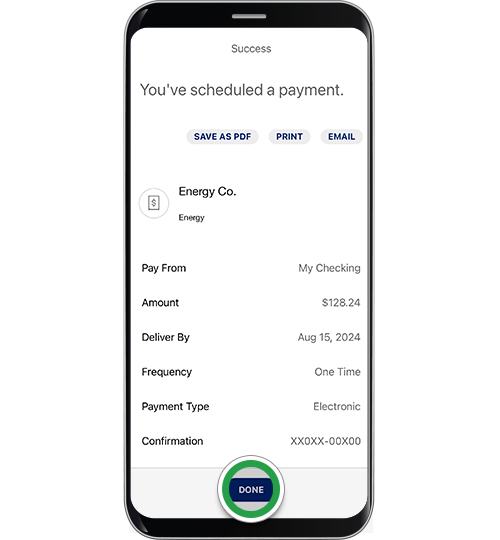

- Review and Confirm: A crucial step where you verify all the details before authorizing the transaction. This screen serves as a final check to prevent errors.

Confirming and Tracking Payments

After confirming, the app initiates the transaction.

- Confirmation: You’ll typically receive an immediate on-screen confirmation and often an email or in-app notification. This confirmation indicates that the payment request has been successfully submitted to the payment gateway or bank’s processing system.

- Tracking: Most apps provide a “pending” or “history” section where you can track the status of your payment. The backend systems update the status as the transaction progresses through various stages (processing, sent, completed). This real-time tracking is enabled by constant communication between the app and the financial institutions’ servers.

Ensuring Digital Security and Privacy While Paying Bills

While the convenience of mobile bill payment is undeniable, the security and privacy of your financial data are paramount. The “Tech” niche dictates a deep dive into the mechanisms that protect users in the digital realm.

Safeguarding Your Device and Accounts

The first line of defense is your device itself. Modern smartphones come equipped with robust security features:

- Strong Passcodes/Biometrics: Always use a strong passcode (PIN, pattern) or biometric authentication (fingerprint scanner, facial recognition) to lock your phone. These technologies leverage hardware-level security modules to securely store and process biometric data, preventing unauthorized access.

- Operating System Updates: Keep your phone’s operating system (iOS, Android) updated. Updates often include critical security patches that address newly discovered vulnerabilities, protecting your device from malware and exploits.

- App Updates: Similarly, ensure your banking and payment apps are always updated. Developers constantly release updates that fix bugs, enhance features, and, crucially, patch security loopholes.

- Secure Wi-Fi: Avoid making financial transactions over unsecured public Wi-Fi networks. These networks can be vulnerable to eavesdropping. Use your mobile data connection (which is inherently more secure due to cellular encryption) or a trusted, private Wi-Fi network. VPNs (Virtual Private Networks) can add an extra layer of encryption when using public Wi-Fi.

Recognizing and Avoiding Scams

Cybercriminals constantly devise new ways to trick users. Awareness and adherence to security best practices are essential:

- Phishing/Smishing: Be wary of suspicious emails or text messages (smishing) requesting personal or financial information, or prompting you to click on unusual links. These are often attempts to trick you into revealing login credentials. Always verify the sender and URL. Technologies like DMARC (Domain-based Message Authentication, Reporting, and Conformance) help email providers identify and block forged emails.

- Fake Apps: Only download banking and payment apps from official app stores (Apple App Store, Google Play Store). Malicious actors sometimes create fake apps designed to steal your data. App store vetting processes, though not foolproof, add a layer of security.

- Two-Factor Authentication (2FA/MFA): Enable 2FA whenever possible. This adds an extra layer of security, typically requiring a code sent to your phone or generated by an authenticator app, in addition to your password. This technology makes it significantly harder for unauthorized users to access your accounts even if they have your password.

Understanding Data Encryption and Protocols

At the heart of secure mobile transactions lies encryption.

- End-to-End Encryption: When you input sensitive data (passwords, card numbers) into an app, that data should be encrypted before it leaves your device and remain encrypted until it reaches the intended server. This is typically achieved using TLS (Transport Layer Security) or SSL (Secure Sockets Layer) protocols, which establish a secure, encrypted connection between your device and the server.

- Data at Rest Encryption: Reputable apps and financial institutions also encrypt data when it’s stored on their servers (data at rest). This protects your information even if their servers are physically compromised.

- Tokenization: As mentioned, credit card numbers are often tokenized, meaning they are replaced with a unique, randomly generated string of characters that cannot be reverse-engineered to reveal the original card number. This token is used for transactions, significantly reducing the risk of card data theft.

- Fraud Detection Systems: Banks and payment processors employ sophisticated AI and machine learning algorithms to monitor transactions in real-time, detecting unusual patterns that might indicate fraudulent activity. These systems can flag suspicious transactions and even temporarily block them, protecting your funds.

The Horizon of Mobile Payments: What’s Next?

The technological advancements in mobile payments are far from over. The future promises even greater integration, security, and convenience, pushing the boundaries of what’s possible with our smartphones.

Biometric Authentication Enhancements

While fingerprint and facial recognition are common today, future iterations will likely include more sophisticated and multi-modal biometric authentication. This could involve combining multiple biometrics (e.g., voice and gait analysis), behavioral biometrics (analyzing how you type or swipe), or even advanced vein pattern recognition. These technologies aim to create even more secure, frictionless authentication experiences, making it nearly impossible for unauthorized users to access financial apps. The underlying technology relies on highly accurate sensors, powerful processing capabilities within the device’s secure enclave, and advanced machine learning algorithms for pattern recognition.

AI-Powered Payment Assistants

Artificial intelligence and machine learning are poised to revolutionize how we manage bills. Imagine an AI assistant on your phone that not only reminds you to pay bills but also analyzes your spending patterns, identifies potential savings, negotiates better deals with service providers, and even automatically optimizes payment schedules based on your cash flow. These intelligent assistants would leverage natural language processing (NLP) to understand your commands and preferences, integrate with your financial apps via secure APIs, and use predictive analytics to offer proactive financial advice. This moves beyond simple reminders to truly intelligent financial management.

Integration with Smart Devices and IoT

The Internet of Things (IoT) will increasingly blur the lines between devices. Your smart home devices, wearables, or even your connected car could become extensions of your mobile payment system. For instance, your smart fridge could automatically reorder groceries and process payment directly, or your smart meter could automatically pay your electricity bill based on real-time consumption and a pre-set budget, all authorized and managed through your smartphone as the central control hub. This requires robust, secure device-to-device communication protocols and standardized APIs for seamless integration across diverse hardware and software platforms.

The journey of paying a bill on your phone is a testament to the incredible progress in mobile technology, software engineering, and digital security. As these innovations continue to evolve, our smartphones will only become more indispensable tools for managing our financial lives with unparalleled efficiency, security, and intelligence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.