For many, the journey toward homeownership is the most significant financial milestone of their lives. It represents stability, the building of equity, and a cornerstone of personal wealth. However, the process of securing a home loan—or mortgage—can often feel like navigating a complex labyrinth of financial terminology, regulatory requirements, and rigorous documentation. Understanding how to get a home loan requires more than just a decent income; it demands a strategic approach to personal finance and a deep dive into the mechanisms of the lending industry.

In this guide, we will break down the essential steps of securing a mortgage, from the preliminary financial preparations to the final signatures at the closing table, ensuring you are equipped with the insights needed to make an informed and fiscally sound decision.

Strengthening Your Financial Foundation

Before you even step foot into an open house, you must audit your financial standing. Lenders do not just look at your current bank balance; they evaluate your long-term reliability as a borrower. Your financial health determines not only whether you qualify for a loan but also the interest rate you will pay, which can save or cost you tens of thousands of dollars over the life of the loan.

Understanding Your Credit Score and History

Your credit score is perhaps the single most influential factor in the home loan process. Most conventional lenders look for a FICO score of at least 620, though scores above 740 generally unlock the most competitive interest rates. A high credit score indicates to the lender that you have a history of managing debt responsibly.

To prepare, you should pull your credit reports from the major bureaus (Equifax, Experian, and TransUnion) at least six months before applying. Look for errors or outdated information that could be dragging your score down. During this period, avoid opening new lines of credit or making large purchases on credit cards, as these actions can create “pings” on your report or increase your utilization ratio, both of which can lower your score.

Managing Debt-to-Income (DTI) Ratios

While your credit score measures your reliability, your Debt-to-Income (DTI) ratio measures your capacity to take on more debt. Lenders calculate this by adding up all your monthly debt obligations—such as car loans, student loans, and credit card minimums—and dividing that total by your gross monthly income.

Most lenders prefer a DTI ratio of 43% or lower, although some programs allow for higher ratios if other financial factors are strong. To improve your chances of approval, consider paying down high-interest revolving debt. This not only lowers your DTI but also frees up more of your monthly cash flow to go toward your future mortgage payment.

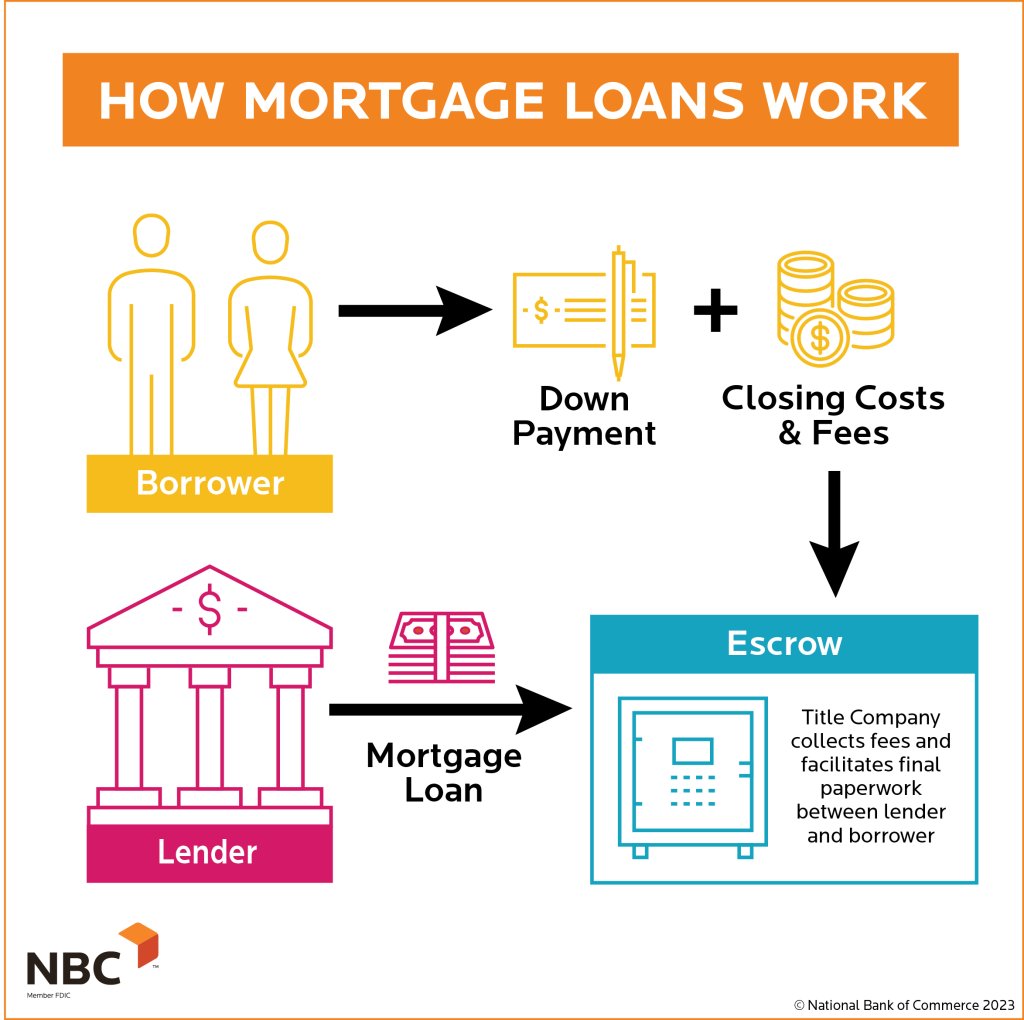

Saving for a Down Payment and Closing Costs

There is a common myth that you need a 20% down payment to buy a home. While 20% is ideal because it allows you to avoid Private Mortgage Insurance (PMI) and lowers your monthly payments, many programs allow for down payments as low as 3% or even 0% for certain borrowers.

However, you must also account for closing costs, which typically range from 2% to 5% of the home’s purchase price. These costs cover appraisal fees, title insurance, taxes, and loan origination fees. Financial discipline in the months leading up to your application—such as automating savings and reducing discretionary spending—is vital to ensuring you have a liquid “safety net” beyond just the down payment.

Navigating the Mortgage Landscape

Once your finances are in order, the next step is to choose the right financial product. Not all home loans are created equal, and the type of loan you choose should align with your long-term financial goals and your current risk tolerance.

Fixed-Rate vs. Adjustable-Rate Mortgages

The most common choice is the 30-year fixed-rate mortgage. The primary benefit here is predictability; your interest rate and monthly principal-and-interest payment remain the same for the entire life of the loan. This protects you against rising interest rates in the future.

Alternatively, an Adjustable-Rate Mortgage (ARM) usually offers a lower “teaser” rate for an initial period (such as 5, 7, or 10 years). After that period, the rate adjusts based on market indexes. ARMs can be beneficial for those who plan to sell or refinance before the initial period ends, but they carry the risk of significantly higher payments if market rates climb.

Conventional Loans vs. Government-Backed Options

Conventional loans are those not insured by the federal government and typically follow the requirements set by Fannie Mae or Freddie Mac. They often require higher credit scores and down payments but offer more flexibility once you reach 20% equity.

If you are a first-time homebuyer or have a lower credit score, government-backed loans may be more accessible:

- FHA Loans: Insured by the Federal Housing Administration, these allow for down payments as low as 3.5% and are more lenient with credit scores.

- VA Loans: Available to veterans and active-duty service members, these often require $0 down and have very competitive rates.

- USDA Loans: Designed for rural and suburban homebuyers with low-to-moderate incomes, these also offer $0 down payment options.

Choosing the Right Lender for Your Needs

Lending is a competitive business, and it pays to shop around. You can obtain a mortgage from a traditional commercial bank, a credit union, or a non-bank mortgage lender. Mortgage brokers can also be helpful, as they act as intermediaries who compare multiple lenders to find you the best deal.

When comparing lenders, look beyond the interest rate. Review the “Loan Estimate” form carefully to compare origination fees, discount points (prepaid interest), and the speed of their closing process. A lender with a slightly higher rate but significantly lower fees might be the more economical choice in the long run.

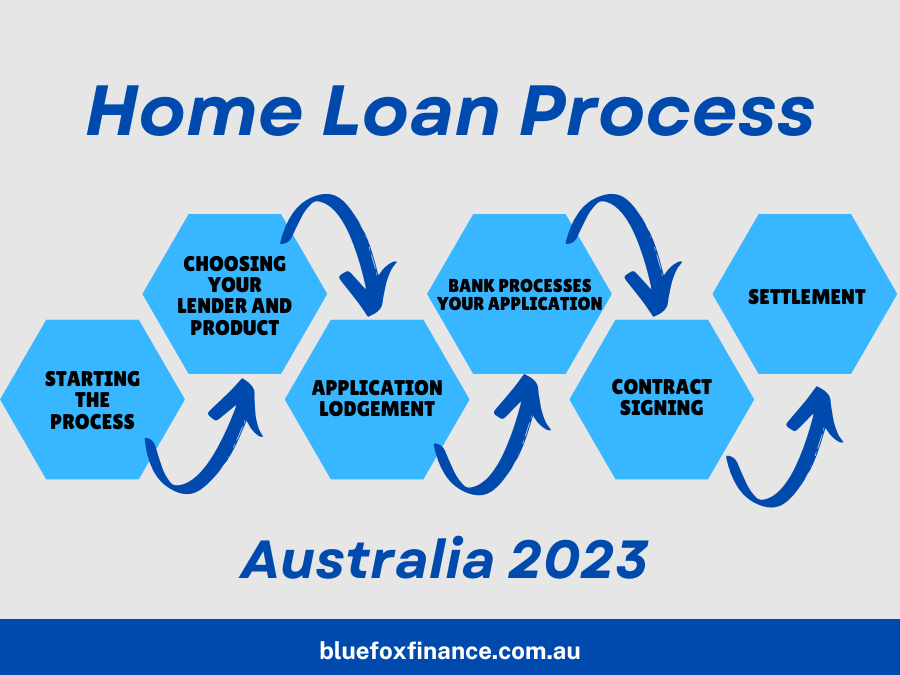

The Step-by-Step Application Process

With a lender in mind and a clear understanding of your budget, it is time to move into the formal application phase. This stage is often the most labor-intensive, requiring a high degree of organization and transparency.

Securing a Pre-approval Letter

A pre-approval is different from a pre-qualification. A pre-qualification is a surface-level estimate, whereas a pre-approval involves a lender verifying your financial data to determine exactly how much they are willing to lend you. In a competitive real estate market, a pre-approval letter is essential; it signals to sellers that you are a serious, vetted buyer with the financial backing to close the deal.

Gathering Essential Documentation

Lenders will require a “paper trail” for your finances. To expedite the process, you should have the following documents ready:

- Proof of Income: W-2 statements from the last two years and your most recent pay stubs.

- Tax Returns: Federal tax returns for the last two years, especially if you are self-employed.

- Asset Statements: Two to three months of bank statements for all checking, savings, and investment accounts.

- Identification: A valid government-issued ID and Social Security number.

- Gift Letters: If a family member is helping with your down payment, you will need a signed letter stating that the funds are a gift and not a loan that needs to be repaid.

Understanding the Underwriting Phase

Once you have found a home and your offer is accepted, the loan moves into “underwriting.” This is the process where the lender’s underwriter double-checks every detail of your application to ensure it meets all guidelines. They will verify your employment, check your credit one last time, and scrutinize your bank deposits.

During this phase, it is crucial to maintain financial “stasis.” Do not quit your job, do not move large sums of money between accounts without documentation, and, most importantly, do not take on new debt. Even a small change in your financial profile can cause the underwriter to deny the loan at the eleventh hour.

From Approval to Closing: Finalizing Your Investment

The final stretch of getting a home loan involves the transition from “approved” to “funded.” This stage focuses on the asset itself—the house—to ensure the lender’s investment is protected.

The Importance of the Home Appraisal

The lender will hire a third-party appraiser to determine the fair market value of the property. This is a safety measure for the lender; they will not lend you more than the home is worth. If the appraisal comes in lower than the purchase price, you may have to bridge the “appraisal gap” with extra cash, renegotiate the price with the seller, or walk away from the deal.

Reviewing the Closing Disclosure

At least three business days before you sign the final papers, your lender is legally required to provide you with a Closing Disclosure (CD). This document outlines the final terms of your loan, your exact monthly payment, and the “cash to close” amount. Compare this document carefully to the initial Loan Estimate you received. If there are significant changes in fees or terms, ask your lender for a detailed explanation immediately.

Signing the Final Paperwork

On closing day, you will meet (often at a title company or attorney’s office) to sign the mortgage note, the deed of trust, and various other legal documents. Once the funds are wired to the seller and the deed is recorded with the county, the process is complete. You are no longer just a borrower; you are a homeowner.

Conclusion

Getting a home loan is a marathon, not a sprint. It requires a high level of financial literacy and a proactive approach to managing your credit, debt, and savings. By understanding the nuances of different loan products and remaining organized through the application and underwriting phases, you can navigate this complex financial landscape with confidence. While the paperwork may be daunting, the result—a home of your own and a stable foundation for your financial future—is a rewarding return on the investment of your time and effort.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.