Closing a bank account might seem like a straightforward task, but it often involves a series of critical steps to ensure a smooth transition and avoid unforeseen complications. Whether you’re consolidating finances, switching to a new bank, moving to a different location, or simply looking to escape recurring fees, understanding the proper procedure is paramount. This comprehensive guide will walk you through everything you need to know, from the initial decision-making to the final confirmation of closure, ensuring your financial integrity remains intact.

Understanding When and Why to Close Your Account

The decision to close a bank account is rarely impulsive; it’s usually driven by specific financial goals or changing life circumstances. Before you initiate the process, it’s beneficial to reflect on your reasons and understand the implications.

Common Reasons for Account Closure

People choose to close bank accounts for a variety of valid reasons, each warranting careful consideration:

- Dissatisfaction with Services or Fees: High monthly maintenance fees, poor customer service, outdated online banking platforms, or unfavorable interest rates are common motivators for seeking a new financial institution. If your current bank no longer meets your needs, it’s a perfectly valid reason to move on.

- Relocation: Moving to a new city, state, or country often necessitates a change in banking relationships, especially if your current bank lacks branches or ATMs in your new area, or if you need a local presence for specific transactions.

- Consolidation of Finances: Many individuals find themselves with multiple accounts opened over time, leading to scattered funds and increased complexity. Consolidating accounts can simplify financial management, making it easier to track spending, savings, and investments.

- Avoiding Dormancy Fees: If an account remains inactive for an extended period, banks may start charging dormancy fees, slowly eroding your balance. Closing an unused account prevents these charges and frees up funds.

- Fraud or Security Concerns: In unfortunate instances of account compromise or perceived security vulnerabilities, closing an account might be a necessary step to protect your finances from further risk.

- Estate Management (Deceased Account Holder): For executors or next of kin, closing accounts belonging to a deceased individual is a crucial part of settling an estate. This process has specific legal requirements and documentation.

When NOT to Close an Account Hasty

While there are many good reasons to close an account, there are also situations where immediate closure might be detrimental. It’s crucial to ensure that the account isn’t actively linked to essential financial obligations. For instance, if you have an active loan (e.g., mortgage, car loan, personal loan) with the same bank, closing your primary checking account there might complicate payment processing or even trigger default clauses if payments are linked to that specific account. Similarly, if critical direct debits for utilities, rent, or loan repayments are still tied to the account, closing it prematurely will lead to missed payments, late fees, and potential damage to your credit score. Always ensure all active financial ties are severed or re-routed before proceeding.

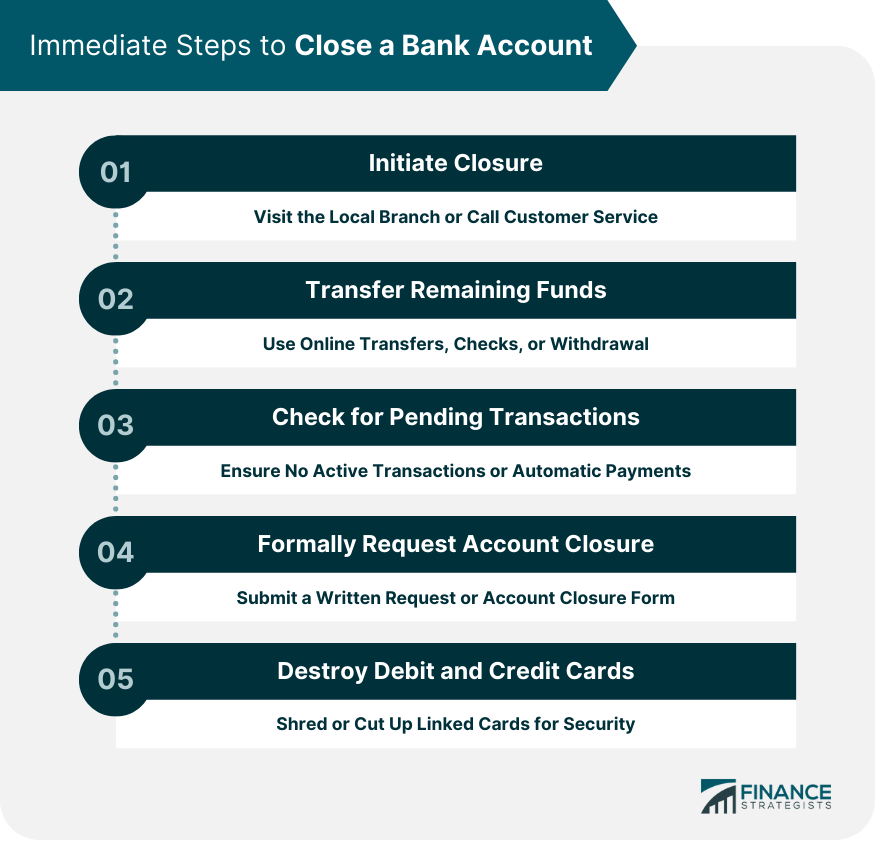

Crucial Steps Before You Initiate the Closure

The preparatory phase is perhaps the most critical part of closing a bank account. Rushing this stage can lead to bounced payments, unexpected fees, and significant financial headaches. Diligence here will save you considerable stress later.

Transferring Funds and Settling Debts

Before anything else, ensure all funds are withdrawn or transferred out of the account you intend to close. This typically involves moving money to another active bank account or withdrawing it as cash. If you choose to transfer, allow ample time for the transaction to clear. Equally important is settling any outstanding debts or fees associated with the account. Overdrafts, monthly service fees, or charges for specific services must be paid off in full before the bank will approve the closure. A negative balance can complicate or indefinitely delay the process.

Updating Direct Deposits and Automatic Payments

This is a step that often gets overlooked, leading to major inconveniences. Create a comprehensive list of all direct deposits (e.g., salary, government benefits, investment dividends) and automatic payments (e.g., utility bills, loan repayments, subscriptions, insurance premiums) linked to the account. Contact each payer and payee individually to update your banking information with your new or existing active account. Begin this process several weeks in advance, as some organizations may take time to process changes. It’s advisable to keep the old account open with a minimal balance for a transitional period (e.g., one to two billing cycles) to catch any payments or deposits that haven’t been successfully rerouted.

Reviewing Linked Services and Subscriptions

Beyond standard direct debits, consider other services linked to your bank account. This could include mobile payment apps (e.g., PayPal, Venmo, Zelle), investment platforms, online shopping accounts, or even digital wallets. Ensure these services are updated with your new bank details or disconnected entirely from the account you plan to close. Failing to do so could result in failed transactions or even continued charges against a closed account, potentially leading to fees or legal issues.

Downloading and Retaining Account Statements

Before closing an account, it’s vital to download and save digital copies of your past statements, typically for at least the past five to seven years, or as long as required for tax purposes or personal record-keeping. These statements serve as crucial documentation for tax filings, loan applications, financial disputes, or simply for monitoring your financial history. Once an account is closed, accessing past statements can become difficult, often incurring fees or requiring special requests. Create a secure digital archive or print physical copies for your records.

Navigating the Account Closure Process

Once you’ve completed all necessary preparations, you’re ready to formally initiate the account closure. Banks typically offer several methods for this, and understanding the requirements for each will streamline the process.

Choosing Your Closure Method

Most banks provide multiple avenues for closing an account:

- In-Person at a Branch: This is often the most straightforward and recommended method, especially if you anticipate any complexities. Visiting a branch allows you to speak directly with a bank representative, ask questions, complete any necessary paperwork on the spot, and receive immediate confirmation. Bring all required documentation.

- Online Banking (if available): Some modern banks and fintech companies allow account closures directly through their online banking portal or mobile app. This method is convenient but less personal. Ensure you follow all digital prompts carefully and look for a digital confirmation.

- Via Mail: If you cannot visit a branch or use online banking, you might be able to close an account by sending a written request via mail. This letter should include your account number, full name, address, contact information, and a clear statement requesting closure. For security and proof of delivery, send it via certified mail with a return receipt requested.

- By Phone: A few banks may facilitate account closures over the phone, but this is less common due to security verification requirements. If available, be prepared to answer extensive security questions to verify your identity.

Required Documentation and Information

Regardless of the method chosen, you will typically need to provide certain information and documentation:

- Account Number(s): The exact account number(s) you wish to close.

- Identification: A valid government-issued photo ID (e.g., driver’s license, passport).

- Signature: Your signature matching the one on file with the bank.

- Written Request: A formal letter or bank form explicitly requesting account closure.

- Debit Card and Checkbook: You may be asked to return or destroy your debit card and any unused checks associated with the account.

For joint accounts, both account holders typically need to authorize the closure, either by appearing together in person or by providing signed consent.

What to Expect During the Process

After submitting your request, the bank will process it. They will verify your identity, confirm that all funds have been transferred out (or issue a final check for any remaining balance, though this is less common now), and ensure there are no outstanding fees or pending transactions. The timeline for closure can vary, but it usually takes a few business days to a week. Some banks might require a hold period to ensure all transactions have cleared. You should receive a confirmation notice, either immediately (in-person) or via mail/email, confirming the account has been successfully closed.

Post-Closure Checklist and Best Practices

The process isn’t truly over until you’ve confirmed the closure and taken a few final precautionary steps. This ensures no loose ends remain that could cause issues down the line.

Confirming Account Closure

The most crucial post-closure step is to verify that the account has indeed been closed. Do not assume closure until you receive official confirmation from the bank. This confirmation can come in the form of a letter, an email, or a final statement showing a zero balance and indicating closure. If you don’t receive confirmation within the expected timeframe, follow up with the bank. You might also try logging into your online banking portal to see if the account is still visible; if it’s gone, that’s a good sign. Keeping the confirmation document in your records is advisable.

Monitoring Your Credit Report

While closing a checking or savings account typically doesn’t directly impact your credit score, especially if it’s not linked to an overdraft facility or a loan, it’s always good practice to monitor your credit report. This helps you ensure that no unexpected credit inquiries or adverse marks appear due to unforeseen issues related to the closure, such as an accidental overdraft fee being reported. Most services allow you to check your credit report annually for free.

Safely Disposing of Old Cards and Checks

Once the account is confirmed closed, safely dispose of any associated debit cards and unused checks. Debit cards should be cut into multiple pieces, particularly through the magnetic strip and chip, to prevent unauthorized use. Unused checks should be shredded to protect your banking information. Simply throwing them away could make you vulnerable to identity theft or fraud.

Common Pitfalls and Important Considerations

Even with careful planning, certain situations can complicate account closures. Being aware of these potential pitfalls can help you navigate them more effectively.

Avoiding Unforeseen Fees and Penalties

Banks can charge various fees if an account is closed improperly. These might include early closure fees (if the account is closed shortly after opening), fees for insufficient funds during the closure process, or dormancy fees if the account sits inactive for too long before you decide to close it. Always inquire about any potential fees associated with closing your specific account type before proceeding. Ensure your balance is sufficiently positive to cover any final deductions.

Dealing with Joint Accounts

Closing a joint account requires the consent of all account holders. Typically, all parties must sign the closure request or appear in person. If one account holder is unavailable or uncooperative, the process can become more complex. In such cases, contact the bank to understand their specific policies and requirements for closing a joint account when not all parties are present or agreeable. It might be possible to remove one person from the account instead of closing it entirely, depending on the bank’s rules and the agreement between the account holders.

Special Cases: Deceased Accounts and Bankruptcy

- Deceased Accounts: When an account holder passes away, closing their bank account is a legal process handled by the executor or administrator of the estate. This requires presenting a death certificate, letters of testamentary (or similar legal document proving authority), and often a copy of the will. The funds typically become part of the deceased’s estate, subject to probate or distribution according to the will or state law. Banks have strict procedures to protect the estate and beneficiaries.

- Bankruptcy: If you are undergoing bankruptcy, the closure of bank accounts is usually handled as part of the bankruptcy proceedings by the court-appointed trustee. It’s crucial not to close accounts independently without consulting your bankruptcy attorney, as this could have significant legal implications.

The Impact on Your Credit Score

For most checking and savings accounts, closure has no direct impact on your credit score, as these are not considered credit accounts. However, if the account has an overdraft protection line of credit attached, closing it might subtly affect your credit utilization or credit history. More significantly, if an account is closed with a negative balance that goes into collections, this will negatively impact your credit score. This underscores the importance of clearing all outstanding debts before initiating closure.

Closing a bank account is a common financial task that, when approached systematically, can be executed without stress. By understanding your reasons, meticulously preparing, following the bank’s procedures, and conducting a thorough post-closure check, you can ensure a seamless transition and maintain sound financial health.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.