Gift cards have become a ubiquitous part of modern commerce, serving as convenient gifts, promotional incentives, and even tools for personal budgeting. However, like any financial instrument, their utility is maximized when you know precisely how much value they hold. An unspent, forgotten balance is effectively money left on the table. In an era where digital transactions and diverse payment methods prevail, understanding how to accurately and efficiently check your gift card balance is not just a matter of convenience; it’s a crucial aspect of responsible personal finance. This guide delves into the various methods for verifying your gift card balance, explores the financial implications, and provides insights to ensure you never leave money behind on these versatile cards.

The Financial Utility of Gift Cards in Personal Finance

Beyond their superficial role as a present, gift cards hold a significant place in the landscape of personal finance. They represent a stored value, a pre-paid amount designated for specific purchases, making them a unique financial tool that straddles the line between cash and credit. For many, they simplify budgeting, streamline gifting, and introduce consumers to new brands or services, all while carrying specific financial implications that savvy individuals should understand.

Gift Cards as a Gifting and Budgeting Tool

From a gifting perspective, gift cards offer the perfect balance between thoughtful intent and practical choice. They eliminate the guesswork of finding the “perfect” item, empowering the recipient to select what they truly want or need, thereby reducing the likelihood of unwanted gifts contributing to waste or requiring returns. For the giver, they provide a convenient and universally accepted form of present, often available for purchase instantly.

However, their role extends beyond simple gifting. For individuals keen on meticulous budgeting, gift cards can act as a powerful spending control mechanism. Imagine dedicating a specific gift card balance towards discretionary spending categories, such as entertainment, dining out, or a particular hobby. Once the balance is depleted, the spending stops, preventing overspending from one’s primary bank account or credit cards. This pre-funded nature imposes a natural boundary, fostering disciplined spending habits and making it easier to track expenditures within defined limits. For instance, a gift card to a coffee shop ensures that daily caffeine fixes don’t inadvertently spiral out of control and impact broader household budgets.

Understanding Stored Value and Consumer Rights

Fundamentally, a gift card represents “stored value.” You (or someone else) have pre-paid for a certain amount of goods or services from a specific merchant or network. This pre-payment creates a liability for the issuer and an asset for the holder. It’s crucial to recognize that this isn’t merely a piece of plastic; it’s a financial instrument backed by the issuer’s promise to honor its value.

Consumer rights surrounding gift cards have significantly evolved, particularly in regions like the United States with the CARD Act of 2009. This legislation introduced key protections, such as:

- Expiration Dates: Generally, gift cards cannot expire in less than five years from the date of issuance or the last date funds were added to the card.

- Dormancy Fees: If a gift card is inactive for a period, issuers can charge dormancy, inactivity, or service fees, but usually only after one year of inactivity, and they must disclose these fees clearly.

- Disclosure: Issuers are required to clearly disclose any terms and conditions, including fees and expiration dates.

Understanding these rights is paramount. It ensures that consumers are not unfairly deprived of their hard-earned or gifted value. Knowing the legal framework empowers cardholders to challenge unfair practices and guarantees that the stored value remains accessible for a reasonable period, solidifying the gift card’s role as a reliable financial tool.

Common Methods for Verifying Your Gift Card Balance

The process of checking a gift card balance has become increasingly streamlined, offering multiple avenues to suit various preferences and situations. While the specific steps can vary slightly depending on the issuer (e.g., a major retailer vs. a credit card network gift card), the underlying methods remain largely consistent. Familiarity with these options ensures quick and accurate verification, preventing the embarrassment of insufficient funds at checkout or the oversight of forgotten value.

Online Portal Checks: The Digital Approach

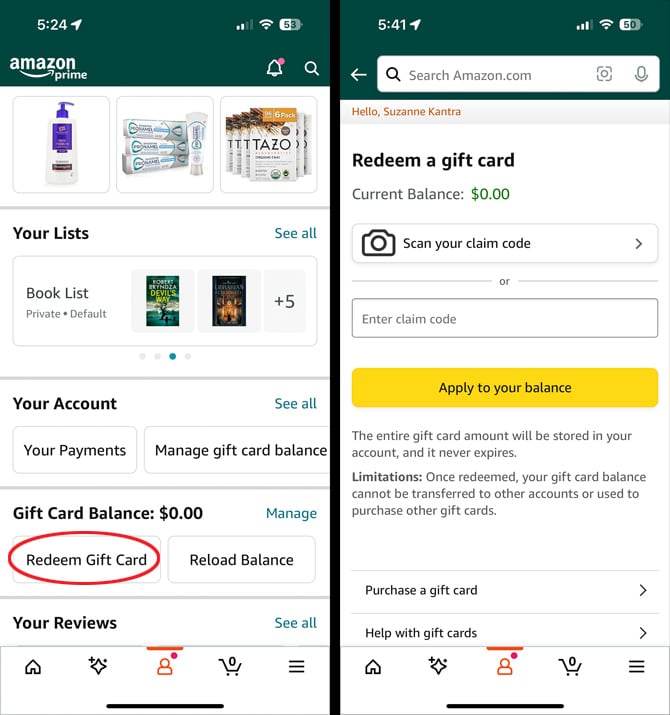

In today’s digital age, checking a gift card balance online is often the quickest and most convenient method. Most major retailers, restaurants, and financial institutions that issue gift cards provide a dedicated section on their official websites for balance inquiries.

How it works:

- Locate the Website: Turn over your gift card. You’ll typically find the issuer’s website address printed on the back, often near the card number or PIN.

- Navigate to the Balance Check Page: On the website, look for a link or search bar function related to “Check Balance,” “Gift Card Balance,” “Card Services,” or “My Account.”

- Enter Card Details: You will be prompted to enter the gift card number (usually 16 digits) and often a PIN (Personal Identification Number). The PIN is typically found under a scratch-off strip on the back of the card.

- View Balance: After submitting the details, your current balance will be displayed.

This method is ideal for those who prefer digital interaction, offering instant results from the comfort of their home. It also allows you to keep a digital record of balances for multiple cards if you wish.

In-Store Inquiry: The Traditional Method

For those who prefer a more traditional, direct approach, or perhaps find themselves already at the merchant’s location, an in-store inquiry is a reliable option.

How it works:

- Visit the Store: Take your gift card to any physical location of the merchant that issued it.

- Approach Customer Service: Head to the customer service desk, a checkout counter, or sometimes even a dedicated gift card kiosk.

- Present Your Card: Hand your gift card to an employee and politely ask them to check the balance.

- Receive Confirmation: The employee will typically swipe the card or manually enter its number into their point-of-sale system and inform you of the remaining balance.

This method provides immediate, in-person confirmation and can be particularly useful if you’re planning an immediate purchase and want to confirm the exact funds available before selecting items.

Phone Support: Direct Communication with Issuers

When online access is unavailable, or if you encounter issues with a card (e.g., a damaged card number, a suspicious transaction), calling the issuer directly is a robust alternative.

How it works:

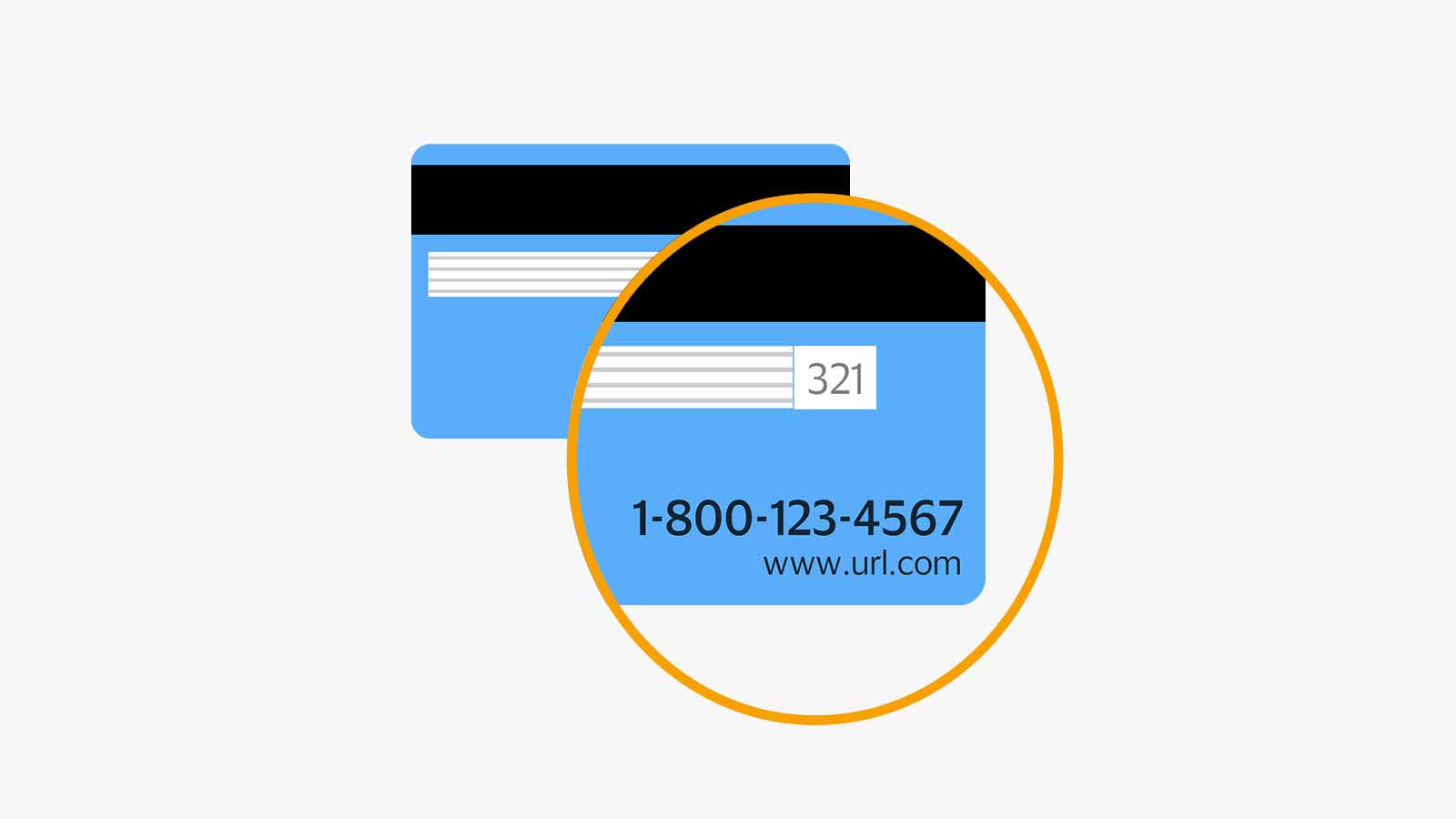

- Find the Customer Service Number: The toll-free customer service number is almost always printed on the back of the gift card.

- Dial and Navigate: Call the number and follow the automated prompts to reach the gift card or customer service department. You might be asked to input your card number and PIN via the phone keypad.

- Speak with a Representative: If the automated system doesn’t provide the information or if you have specific questions, you’ll have the option to speak with a customer service representative who can manually check the balance and offer further assistance.

This method is excellent for troubleshooting or when you require more detailed information than what an online portal might provide. It also offers a human touch, which can be reassuring when dealing with financial matters.

Mobile Apps and Digital Wallets: Modern Convenience

As smartphones become indispensable, many retailers and payment platforms have integrated gift card management into their mobile ecosystems.

How it works:

- Download the Merchant’s App: Many large retailers have dedicated mobile apps where you can link your gift cards to your account.

- Add Gift Card: Within the app, look for a “Wallet,” “Payments,” or “Gift Cards” section. You can typically add your gift card by scanning it or manually entering its details.

- View Balance: Once linked, the app will often display the current balance and allow you to use it for in-app or in-store purchases.

- Digital Wallets: Platforms like Apple Wallet, Google Pay, and others are increasingly allowing users to store digital versions of gift cards. While not all gift cards are supported, for those that are, the balance is often updated automatically or can be checked with a tap.

These modern methods offer unparalleled convenience, allowing you to access and manage your gift card balances on the go, often integrating them seamlessly into your daily payment routines.

Navigating Challenges and Maximizing Gift Card Value

While gift cards offer convenience and financial flexibility, their true value can be eroded by common pitfalls such as expiration, loss, or inactivity fees. Proactive management and awareness of specific challenges are crucial to ensuring you extract every penny of their worth. Maximizing gift card value extends beyond merely checking a balance; it involves strategic redemption and safeguarding against common issues.

Dealing with Expired or Lost Gift Cards

The dread of finding an expired gift card or realizing one has been misplaced is familiar to many. However, not all hope is lost.

- Expired Cards: Thanks to consumer protection laws (like the CARD Act in the U.S.), gift cards generally cannot expire for five years from their issuance date or the last time money was added. If your card has an expiration date, check if it falls within this protective window. Even if it seems expired, it’s always worth contacting the issuer. Some companies, as a gesture of goodwill, may re-issue an expired card or apply the balance to a new one, especially if the expiration is recent. Persistence and politeness can often yield positive results.

- Lost or Stolen Cards: This is where the importance of keeping records comes in. If you have the original receipt, the card number, or any activation information, immediately contact the issuer. Many issuers can cancel the lost card and issue a replacement with the remaining balance, particularly if it was a registered card. However, general “open-loop” cards (like Visa or Mastercard gift cards) are often treated like cash – once lost, they’re gone. Some retailers offer balance protection if you’ve registered the card online, so always check this option.

The key takeaway is to act quickly and keep detailed records (card number, PIN, original purchase receipt) for all your gift cards.

Consolidating and Re-gifting Unused Balances

Often, a gift card might have a small, leftover balance that isn’t enough for a substantial purchase but too much to simply discard. This “orphan” money can be effectively managed:

- Consolidation: If you have multiple gift cards from the same retailer with small balances, ask if the store can consolidate them onto a single new card. This simplifies management and ensures the full value is more easily redeemable.

- “Gift Card Chipping”: Use the small balance towards a larger purchase, paying the difference with another form of payment. This strategy ensures you use every last cent.

- Sell or Trade: Several online platforms (e.g., CardCash, Raise) allow you to sell unwanted gift cards for cash, typically at a slight discount to their face value. This is a practical way to convert a card you won’t use into spendable money.

- Re-gifting (with caution): If a gift card is for a store you genuinely won’t visit, and it has a reasonable balance, re-gifting can be an option. However, ensure the card’s terms are clear, and the recipient will genuinely appreciate and use it. Always ensure you know the exact balance and any potential expiration dates before passing it on.

Strategic consolidation or alternative uses prevent these small, forgotten sums from accumulating into significant lost value over time.

Avoiding Scams and Protecting Your Gift Card Value

Gift cards are unfortunately a common target for scammers due to their “cash-like” nature and often limited traceability. Protecting your investment requires vigilance:

- Inspect Before Purchase: When buying a gift card, always check the packaging for any signs of tampering, scratched-off PINs, or altered barcodes. Scammers might tamper with cards in stores, record the numbers, and drain them after activation.

- Purchase from Reputable Sources: Buy gift cards directly from the merchant or well-known retailers. Avoid purchasing from unknown third-party websites or individuals, especially at a deep discount, as these could be counterfeit or already drained.

- Register Your Card: If the option is available, register your gift card online with the issuer. This can offer some protection against loss or theft and make it easier to recover balances.

- Be Wary of Requests for Gift Card Payments: Legitimate businesses and government agencies (like the IRS) will never demand payment via gift cards for debts, taxes, or services. Any such request is a scam. If you receive such a request, report it immediately to the authorities.

- Use Promptly: The best way to protect your gift card value is to use it promptly. The longer a card sits unused, the higher the risk of loss, theft, or forgetting about it entirely.

By being mindful of these risks and adopting protective measures, consumers can ensure that their gift card balances remain secure and fully accessible for their intended purpose, truly maximizing their financial utility.

The Broader Financial Implications of Gift Card Usage

While checking a balance might seem like a simple transactional task, the broader use and management of gift cards hold significant implications for personal finance, consumer behavior, and even the economy. Understanding these wider facets elevates gift card usage from mere spending to a more informed financial decision.

Impulse Spending vs. Mindful Redemption

Gift cards often act as an immediate trigger for spending. The presence of pre-allocated funds can sometimes lead to impulse purchases that wouldn’t have occurred otherwise. The psychological effect of “free money” (even though it was paid for) can override typical budgeting restraints. People might feel compelled to spend the entire balance, even if it means buying something they don’t critically need, simply to “use it up.”

Conversely, gift cards can be a powerful tool for mindful redemption. By intentionally planning how and when to use a gift card, it can facilitate purchases that align with long-term financial goals or provide a budgeted treat without impacting regular cash flow. For instance, holding onto a bookstore gift card until a specific educational book is released, or saving a restaurant gift card for a special occasion, demonstrates a mindful approach. This intentionality prevents the card from dictating spending and instead makes it a component of a well-considered financial plan. The act of checking the balance regularly can reinforce this mindful approach, reminding the holder of the exact value available and encouraging thoughtful allocation.

Understanding Escheatment Laws and Unclaimed Property

A less-talked-about, but financially significant, aspect of gift cards is their relationship with escheatment laws. Escheatment refers to the process by which unclaimed or abandoned property (including gift card balances) is transferred to the state treasury after a certain period of inactivity. The rationale behind these laws is that the funds should ultimately benefit the public good rather than remaining indefinitely with corporations or simply being lost.

The period before escheatment varies by state, but it often ranges from two to five years of inactivity on a gift card. Once escheated, reclaiming these funds can be a bureaucratic process, often requiring claims through state unclaimed property websites. For consumers, this highlights the critical importance of using gift cards promptly and keeping track of balances. While consumer protection laws have extended expiration dates, escheatment remains a risk for truly abandoned cards. Understanding this allows individuals to prioritize the use of older, less-active gift cards to prevent their value from being transferred to the state. It underscores the financial imperative to check balances and redeem value rather than allowing cards to gather dust.

Gift Cards in a Cashless Economy

The growing prevalence of gift cards also reflects a broader shift towards a cashless economy. As physical cash transactions diminish, digital and stored-value instruments, including gift cards, become more integrated into daily financial life. They serve as a bridge between traditional money and newer digital payment methods.

This trend offers benefits like enhanced security (less physical cash to lose), convenience, and often, improved tracking of spending when cards are linked to digital accounts. However, it also introduces challenges, such as digital literacy requirements for balance checks and a higher potential for scams targeting digital assets. For individuals, adapting to this evolving landscape means becoming comfortable with digital management of financial tools, including gift cards. The ability to seamlessly check balances online or via an app isn’t just a nicety; it’s a foundational skill for navigating a world increasingly reliant on digital transactions. As the financial world continues its digital transformation, understanding and managing tools like gift cards become an integral part of maintaining financial health and staying economically empowered.

Ultimately, knowing “how do I check my gift card balance” is far more than a simple inquiry. It’s an entry point into responsible personal finance, consumer awareness, and adaptation to the modern financial ecosystem. By embracing the diverse methods available and understanding the broader implications, consumers can ensure they maximize the utility and safeguard the value of every gift card they receive.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.