Understanding how interest is calculated is one of the most fundamental skills in personal finance. Whether you’re saving for retirement, taking out a loan for a new home, managing credit card debt, or investing in the stock market, interest plays a pivotal role in determining how your money grows or how much you owe. Far from being a complex mathematical enigma, the core principles of interest calculation are straightforward and, once mastered, provide an invaluable lens through which to view your financial decisions.

Interest, in its simplest form, is the cost of borrowing money or the reward for lending it. For borrowers, it’s the extra amount they pay back in addition to the principal loan amount. For savers and investors, it’s the return they earn on their deposited or invested capital. The ability to calculate interest not only helps you understand the true cost of a loan or the potential growth of an investment but also empowers you to make smarter financial choices, from selecting the right savings account to strategizing your debt repayment. This guide will demystify interest calculation, covering everything from basic simple interest to the powerful forces of compound interest and beyond.

The Fundamentals: Simple Interest Explained

Before diving into the more complex aspects of financial mathematics, it’s crucial to grasp the concept of simple interest. This is the most basic form of interest calculation and serves as a foundational building block for understanding all other interest types.

What is Simple Interest?

Simple interest is calculated solely on the original principal amount of a loan or deposit. This means that the interest earned or charged does not accumulate and get added back into the principal for subsequent interest calculations. It’s a flat rate applied to the initial sum for a specified period.

Simple interest is typically used for short-term loans, basic savings accounts, or when the interest is paid out periodically rather than being reinvested. For instance, a small personal loan, a short-term certificate of deposit (CD), or even a basic savings account might use simple interest. Its simplicity makes it easy to understand and calculate, but it doesn’t offer the accelerated growth potential seen with compound interest.

The Simple Interest Formula

Calculating simple interest is straightforward and relies on a very accessible formula:

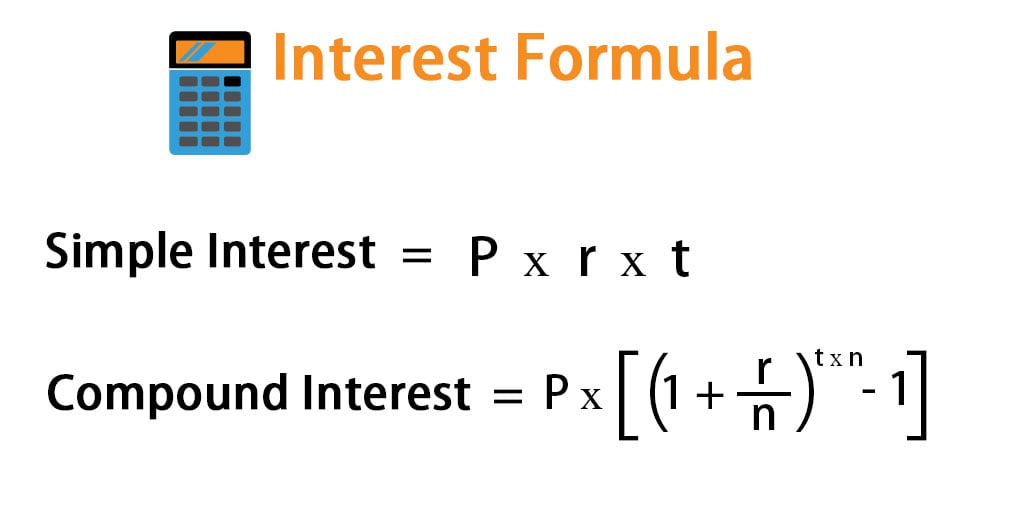

I = P × R × T

Where:

- I = Interest amount (the money earned or paid)

- P = Principal amount (the initial amount of money borrowed or invested)

- R = Annual interest rate (expressed as a decimal, e.g., 5% is 0.05)

- T = Time period (the duration for which the money is borrowed or invested, in years)

It’s crucial that the interest rate (R) is an annual rate and the time (T) is expressed in years. If you have a rate that’s monthly, you’ll need to convert it to an annual rate (multiply by 12). If your time period is in months, divide by 12 to convert it to years.

Practical Examples of Simple Interest Calculation

Let’s illustrate with a few scenarios:

Example 1: A Personal Loan

Suppose you take out a personal loan of $10,000 with a simple annual interest rate of 6% for 3 years.

- P = $10,000

- R = 0.06 (6%)

- T = 3 years

I = $10,000 × 0.06 × 3 = $1,800

The total interest you will pay over 3 years is $1,800. The total amount to repay would be the principal plus interest: $10,000 + $1,800 = $11,800.

Example 2: A Simple Savings Account

You deposit $5,000 into a savings account that pays 1.5% simple annual interest for 6 months.

- P = $5,000

- R = 0.015 (1.5%)

- T = 6 months = 0.5 years (6/12)

I = $5,000 × 0.015 × 0.5 = $37.50

After 6 months, you would have earned $37.50 in interest. Your total balance would be $5,000 + $37.50 = $5,037.50.

These examples highlight how simple interest provides a clear, predictable cost or earning over a set period.

Harnessing the Power: Understanding Compound Interest

While simple interest is easy to grasp, the true engine of wealth creation (and, conversely, debt accumulation) lies in compound interest. Often called the “eighth wonder of the world” by Albert Einstein, its effect can be profoundly impactful over time.

What is Compound Interest?

Compound interest is the interest on an initial principal plus the accumulated interest from previous periods. In essence, it’s “interest on interest.” Instead of only calculating interest on the original amount, compound interest calculates interest on the continually growing total amount. This snowball effect means your money can grow at an accelerating rate.

Compound interest is the standard for most long-term financial products, including investments, mortgages, credit card debt, and the majority of savings accounts. Understanding its mechanism is paramount for anyone planning for retirement, saving for a major purchase, or managing significant debt.

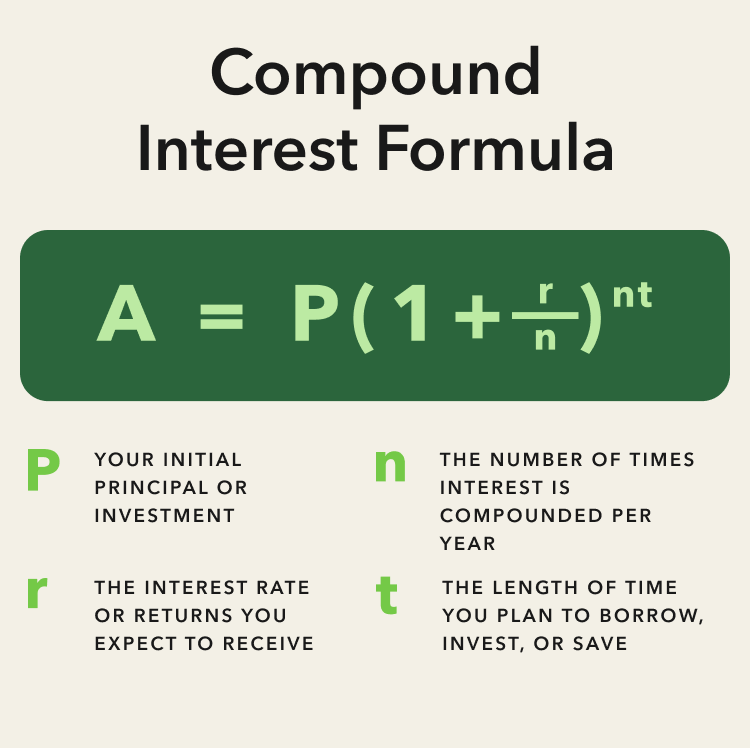

The Compound Interest Formula

The formula for compound interest is slightly more complex than simple interest, reflecting its dynamic nature:

A = P (1 + R/n)^(nt)

Where:

- A = The future value of the investment/loan, including interest (Total Amount)

- P = The principal investment amount (the initial deposit or loan amount)

- R = The annual interest rate (as a decimal)

- n = The number of times that interest is compounded per year

- t = The number of years the money is invested or borrowed for

The variable ‘n’ is crucial here, as it dictates the compounding frequency. Interest can be compounded:

- Annually: n = 1

- Semi-annually: n = 2

- Quarterly: n = 4

- Monthly: n = 12

- Daily: n = 365

The more frequently interest is compounded, the faster your money grows (or your debt increases), assuming the same annual interest rate.

Step-by-Step Compound Interest Calculation Examples

Let’s see compound interest in action:

Example 1: Investment Compounded Annually

You invest $10,000 in a savings bond that offers a 5% annual interest rate, compounded annually, for 5 years.

- P = $10,000

- R = 0.05

- n = 1 (annually)

- t = 5 years

A = $10,000 (1 + 0.05/1)^(1*5)

A = $10,000 (1.05)^5

A = $10,000 * 1.27628

A = $12,762.82

The total amount after 5 years is $12,762.82. The interest earned is $2,762.82.

Compare this to simple interest for the same period: $10,000 * 0.05 * 5 = $2,500. Compound interest yielded $262.82 more.

Example 2: Savings Compounded Monthly

You deposit $5,000 into a savings account that pays 1.5% annual interest, compounded monthly, for 1 year.

- P = $5,000

- R = 0.015

- n = 12 (monthly)

- t = 1 year

A = $5,000 (1 + 0.015/12)^(12*1)

A = $5,000 (1 + 0.00125)^12

A = $5,000 * (1.00125)^12

A = $5,000 * 1.01511

A = $5,075.55

The total amount after 1 year is $5,075.55. The interest earned is $75.55. Even with a modest rate, monthly compounding slightly outperforms annual compounding.

Example 3: Credit Card Debt with Monthly Compounding

You have a credit card balance of $2,000 with an annual interest rate of 18%, compounded monthly. If you make no payments for one year, what would your balance be?

- P = $2,000

- R = 0.18

- n = 12 (monthly)

- t = 1 year

A = $2,000 (1 + 0.18/12)^(12*1)

A = $2,000 (1 + 0.015)^12

A = $2,000 * (1.015)^12

A = $2,000 * 1.1956

A = $2,391.24

Your balance would grow to $2,391.24, meaning you’d owe $391.24 in interest. This example starkly illustrates the power of compounding working against you in the context of debt.

Beyond the Basics: Advanced Interest Concepts and Applications

While simple and compound interest form the core, the financial world introduces further nuances that are critical for truly informed decision-making.

Annual Percentage Rate (APR) vs. Annual Percentage Yield (APY)

These two terms are frequently confused but represent distinct aspects of interest:

- APR (Annual Percentage Rate): This represents the annual cost of a loan, including any additional fees or costs, but before compounding. It’s often used for mortgages, car loans, and credit cards. For loans that compound interest more frequently than annually, the APR will be lower than the true effective rate. It’s a nominal rate.

- APY (Annual Percentage Yield): This represents the effective annual rate of return an investment or savings account actually earns, taking into account the effect of compounding. Because it includes compounding, the APY will always be equal to or higher than the stated annual interest rate when compounding occurs more than once a year.

Why the distinction matters: When borrowing, look for the lowest APR. When saving or investing, look for the highest APY. APY gives you a truer picture of your earnings, while APR gives you a standard basis for comparing loan costs.

Interest in Lending: Amortization and Loan Schedules

For larger loans like mortgages or auto loans, interest calculation becomes part of an amortization schedule. This schedule breaks down each payment into its principal and interest components over the life of the loan. Early in the loan term, a larger portion of your payment goes towards interest, and a smaller portion towards the principal. As the principal balance decreases with each payment, the interest portion of subsequent payments also decreases, and more of your payment goes towards reducing the principal.

Understanding this allows borrowers to make strategic decisions, such as:

- Making extra principal payments: Even small extra payments can significantly reduce the total interest paid and shorten the loan term, particularly early in the loan’s life.

- Refinancing: Knowing how much interest you’ll pay over the remaining life of your loan helps evaluate whether refinancing to a lower interest rate is beneficial.

Interest in Investing: Present Value and Future Value

Interest calculations are fundamental to the concept of the time value of money, which states that a dollar today is worth more than a dollar in the future due to its potential earning capacity.

- Future Value (FV): Calculates what a current amount of money or a series of payments will be worth at a specific point in the future, assuming a certain interest rate (compounding). The compound interest formula calculates future value.

- Present Value (PV): Calculates the current value of a future sum of money or stream of cash flows given a specified rate of return. It essentially discounts future money back to today’s terms.

Investors use these calculations to evaluate investment opportunities, determine fair prices for assets, and plan for future financial goals.

Practical Tools and Tips for Interest Calculation

While understanding the formulas is vital, modern technology offers accessible ways to perform these calculations quickly and accurately.

Using Online Calculators and Spreadsheets

You don’t need to manually crunch numbers for every scenario:

- Online Calculators: Numerous free online calculators are available for mortgages, personal loans, savings growth, credit card interest, and more. A quick search for “compound interest calculator” or “loan amortization calculator” will yield many options. These tools often allow you to adjust variables like principal, rate, time, and compounding frequency to see immediate results.

- Spreadsheets (Excel/Google Sheets): Spreadsheets offer powerful built-in financial functions:

FV()(Future Value): Calculates the future value of an investment based on periodic, constant payments and a constant interest rate.PV()(Present Value): Calculates the present value of an investment.RATE(): Returns the interest rate per period of an annuity.NPER(): Returns the number of periods for an investment.PMT(): Calculates the payment for a loan based on constant payments and a constant interest rate.IPMT()andPPMT(): Calculate the interest payment and principal payment for a given period of an investment/loan.

Mastering these spreadsheet functions can provide a highly flexible and customizable way to analyze various financial scenarios.

Key Factors Influencing Interest

Several factors influence the interest rates you encounter:

- Economic Conditions: Central bank interest rates (e.g., the Federal Funds Rate in the U.S.) significantly impact lending rates across the economy.

- Creditworthiness: For borrowers, a higher credit score generally leads to lower interest rates on loans and credit cards, as lenders perceive less risk.

- Compounding Frequency: As discussed, more frequent compounding leads to greater interest accumulation over time for a given annual rate.

- Loan/Investment Term: Longer terms often come with slightly higher interest rates (for loans) or greater overall interest earnings (for investments) due to the increased time exposure.

- Risk: Higher-risk investments or loans typically demand higher interest rates to compensate for the potential for loss.

Strategic Implications for Personal Finance

Armed with a solid understanding of interest calculation, you can make smarter financial moves:

- Maximize Savings and Investments: Understand how to leverage compound interest to your advantage. Start saving early, contribute regularly, and seek out accounts with higher APYs and more frequent compounding.

- Minimize Debt Costs: Be acutely aware of the APR on credit cards and loans. Prioritize paying off high-interest debt first to reduce the compounding effect working against you. Make extra principal payments whenever possible.

- Make Informed Decisions: Whether it’s comparing mortgage offers, evaluating different investment vehicles, or choosing a savings account, knowing how to calculate interest allows you to compare options on an apples-to-apples basis and select the most financially beneficial path.

Conclusion

The question “how do I calculate interest?” opens the door to a fundamental aspect of financial literacy. From the simplicity of simple interest to the exponential power of compounding, mastering these calculations transforms abstract financial concepts into actionable insights. Understanding interest isn’t just about crunching numbers; it’s about gaining control over your financial destiny.

By grasping how interest works, you empower yourself to accelerate your wealth accumulation, minimize your debt burden, and make confident, informed financial decisions. It is the cornerstone upon which sound personal finance is built, providing the clarity needed to navigate the complexities of saving, borrowing, and investing. Embrace these calculations, and you’ll unlock a powerful tool for financial success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.