In the intricate world of personal finance and investing, few concepts hold as much power and promise as compound interest. Often dubbed the “eighth wonder of the world” by Albert Einstein, it’s the engine that drives long-term wealth accumulation, allowing your money to earn money on itself. While many are familiar with the general idea of compounding, understanding its daily application – and how to calculate it – can unlock a significantly deeper appreciation for its potential. This article will demystify daily compound interest, breaking down its calculation, exploring its advantages, and providing practical tools and strategies to harness its formidable power for your financial future.

Understanding the Power of Compounding

Before diving into the mechanics of calculation, it’s crucial to grasp what compound interest truly is and why its frequency, especially daily, matters so much.

What is Compound Interest?

At its core, compound interest is interest calculated on the initial principal, which also includes all the accumulated interest from previous periods. Unlike simple interest, where interest is only earned on the original principal amount, compound interest allows your earnings to generate further earnings. It’s a snowball effect: the longer your money is invested and the more frequently it compounds, the larger your principal becomes, leading to an exponential growth trajectory.

Imagine you deposit $1,000 into an account that pays 5% interest annually.

- Simple Interest: After one year, you earn $50 ($1,000 * 0.05). If you keep it for 10 years, you’d earn $500 total ($50 * 10). The principal for interest calculation always remains $1,000.

- Compound Interest: After one year, you also earn $50, making your balance $1,050. In the second year, however, you earn 5% interest on $1,050, not just $1,000. This means you earn $52.50 in the second year, bringing your total to $1,102.50. This small difference grows substantially over time.

Simple vs. Compound Interest: A Fundamental Difference

The distinction between simple and compound interest is fundamental to financial literacy. Simple interest is usually seen in short-term loans or very basic savings accounts, where the interest is calculated only on the initial principal amount. It provides a linear growth path for your money.

Compound interest, conversely, provides an exponential growth path. It’s the standard for most savings accounts, investments like stocks and bonds (through reinvested dividends or coupon payments), and retirement funds. The key takeaway is that with compound interest, your capital not only grows from the initial investment but also from the interest previously earned, creating a virtuous cycle of wealth accumulation.

The Daily Advantage: Why Frequency Matters

The frequency of compounding refers to how often the earned interest is added back to the principal. While interest can compound annually, semi-annually, quarterly, or monthly, daily compounding is one of the most frequent intervals available. The more frequently interest is compounded, the faster your money grows, because you start earning interest on your interest sooner.

For instance, an account that compounds daily will add a tiny amount of interest to your principal every single day. This means that the next day, you’re earning interest on a slightly larger sum. While the individual daily increment might seem negligible, its cumulative effect over months and years can be quite significant, especially with larger principal amounts and longer time horizons. This is the core reason why optimizing for daily compounding, where available, can be a smart move for investors and savers alike.

The Formula and Its Components

To calculate daily compound interest, we turn to the universal compound interest formula, adapting it slightly for the daily frequency. Understanding each variable is key to accurate calculation.

Deconstructing the Compound Interest Formula

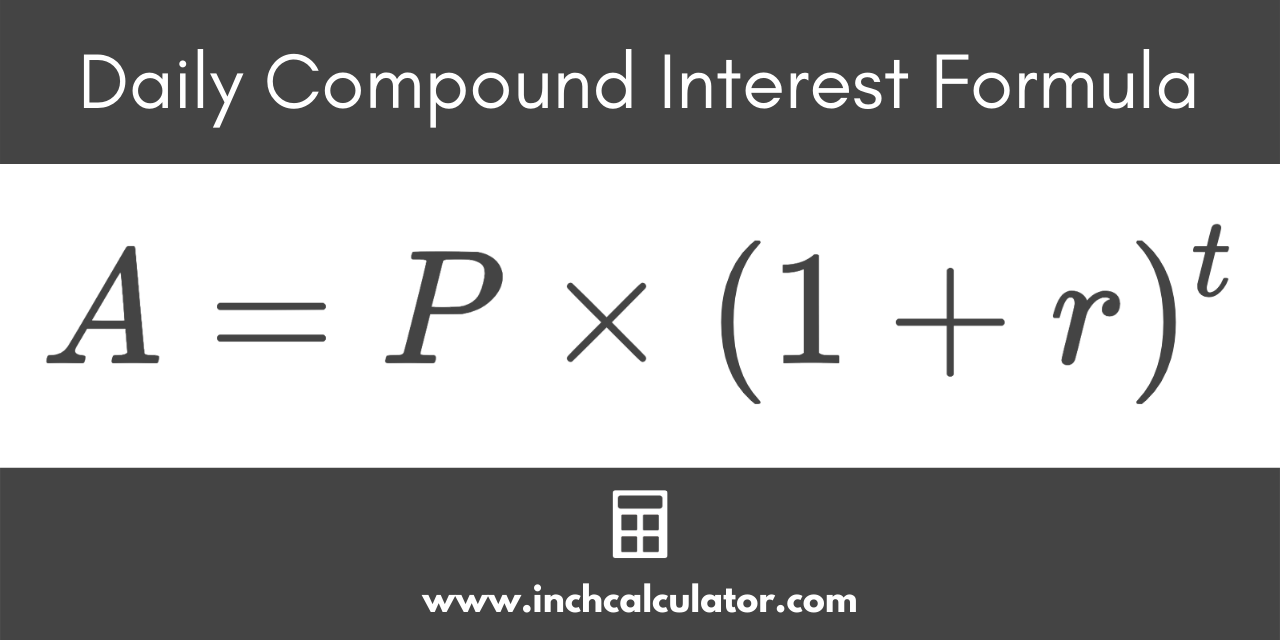

The standard formula for compound interest is:

$$A = P (1 + r/n)^{nt}$$

Let’s break down what each variable represents:

- A = Future Value of the Investment/Loan, including interest: This is the total amount you will have at the end of the investment period.

- P = Principal Investment Amount (the initial deposit or loan amount): This is the starting sum of money you’re investing or borrowing.

- r = Annual Interest Rate (as a decimal): This is the stated interest rate, but it must be converted from a percentage to a decimal for calculation (e.g., 5% becomes 0.05).

- n = Number of times that interest is compounded per year: This is the critical variable for determining frequency. For daily compounding, ‘n’ will be 365 (or 360 in some specific financial contexts, but 365 is standard for daily).

- t = Number of years the money is invested or borrowed for: This represents the total duration of the investment.

Adapting the Formula for Daily Compounding

To calculate daily compound interest, we simply set ‘n’ to 365 (assuming a standard year without leap days).

So, the formula becomes:

$$A = P (1 + r/365)^{365t}$$

This adjustment ensures that the annual interest rate is divided into 365 daily segments, and the compounding occurs 365 times each year for the duration of ‘t’ years.

Practical Example: A Step-by-Step Calculation

Let’s put the formula into action with a practical example.

Scenario: You invest $10,000 into a savings account that offers an annual interest rate of 4% and compounds interest daily. You want to know how much money you will have after 5 years.

Given:

- P (Principal) = $10,000

- r (Annual Interest Rate) = 4% = 0.04 (as a decimal)

- n (Compounding Frequency) = 365 (daily)

- t (Time in Years) = 5

Calculation Steps:

- Calculate r/n:

$0.04 / 365 approx 0.000109589$ - Calculate 1 + r/n:

$1 + 0.000109589 = 1.000109589$ - Calculate nt:

$365 * 5 = 1825$ - Calculate (1 + r/n)^nt:

$(1.000109589)^{1825} approx 1.221396$ - Calculate A = P * (result from step 4):

$A = 10,000 * 1.221396 approx 12,213.96$

Result: After 5 years, your investment will have grown to approximately $12,213.96.

To find the actual interest earned, subtract the principal: $12,213.96 – $10,000 = $2,213.96.

This step-by-step approach demonstrates the precise way to calculate daily compound interest, revealing the eventual growth of your initial investment.

Tools and Resources for Calculation

While manually calculating daily compound interest is possible, especially with the provided formula and an advanced calculator, several tools can simplify the process and minimize the risk of human error.

Online Compound Interest Calculators

The internet is replete with free online compound interest calculators. These tools are incredibly user-friendly: you simply input your principal, annual interest rate, compounding frequency (select daily), and the investment term, and they instantly provide the future value. Many also offer charts and breakdown tables to visualize the growth over time. They are ideal for quick estimations and comparing different scenarios.

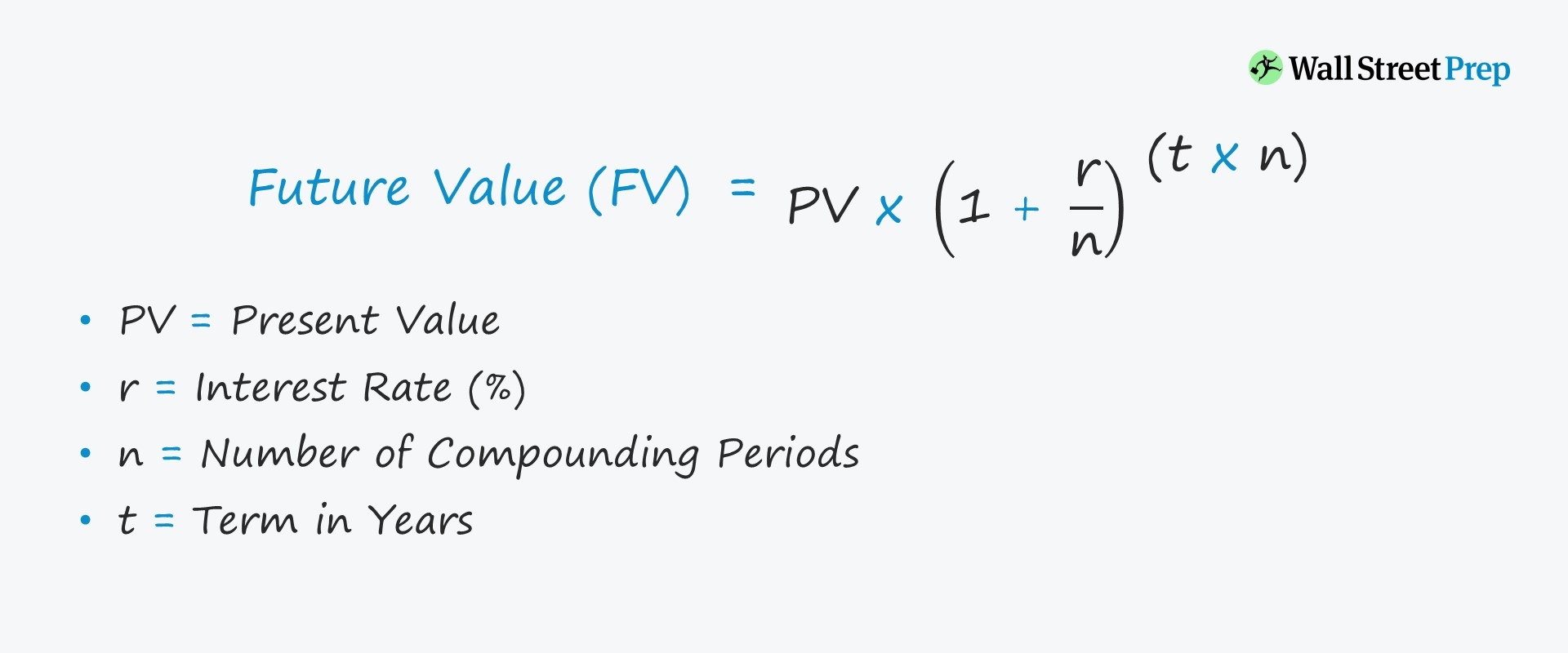

Spreadsheet Software (Excel/Google Sheets)

For those who prefer a more hands-on approach or need to integrate compound interest calculations into larger financial models, spreadsheet software like Microsoft Excel or Google Sheets is invaluable. They offer built-in functions that can perform these calculations with ease.

The primary function for future value (FV) in spreadsheets is often:

=FV(rate, nper, pmt, [pv], [type])

For daily compound interest, it would look something like this:

=FV(r/365, t*365, 0, -P)

Where:

r/365is your daily rate.t*365is your total number of daily periods.0forpmt(no additional payments).-Pis your initial principal, entered as a negative value because it’s an outflow of cash.

Spreadsheets allow for great flexibility, letting you easily adjust variables and see the impact in real-time.

Financial Calculators and Apps

Dedicated financial calculators (both physical devices and smartphone apps) are also excellent tools. Many come pre-programmed with functions to calculate time value of money (TVM) scenarios, including future value with various compounding frequencies. While they might have a slight learning curve, they are powerful for complex financial planning and professional use. Investing apps often have built-in calculators or projections that consider compounding.

Strategies to Maximize Daily Compounding

Understanding the calculation is only half the battle; the other half is implementing strategies to truly maximize the benefits of daily compounding.

Start Early, Be Consistent

The most significant factor influencing compound interest growth is time. The longer your money has to compound, the more substantial the “interest on interest” effect becomes. Starting early, even with modest amounts, allows you to leverage decades of compounding. Consistency, through regular contributions, further amplifies this effect, turning small, regular deposits into significant sums over the long run.

Understand and Optimize Your Interest Rate

While daily compounding offers a slight edge, a higher interest rate will always have a more pronounced impact on your returns. Seek out investment vehicles that offer competitive annual percentage yields (APYs) that compound daily. Be mindful that many high-yield savings accounts advertise daily compounding, making them an excellent choice for short-term savings. For long-term growth, explore investment accounts that offer reinvestment of dividends or capital gains on a frequent basis.

Consider Reinvesting Dividends and Interest

Many investment platforms offer the option to automatically reinvest any dividends or interest payments you receive back into the original investment. This is a powerful strategy that effectively turns those payouts into additional principal, allowing them to start compounding immediately. If your investment pays dividends quarterly, and those dividends are immediately reinvested, it effectively boosts the “n” factor in your personal compounding equation.

The Impact of Taxes and Fees

While not directly part of the calculation, taxes and fees can significantly erode your compounding gains. Be aware of any maintenance fees on accounts or management fees on investments. Furthermore, interest earned on savings accounts is typically taxed as ordinary income. Consider tax-advantaged accounts like IRAs or 401(k)s, where investments can grow tax-deferred or even tax-free, allowing the full power of compounding to work undisturbed for longer periods.

Beyond Daily: Other Compounding Frequencies and Their Implications

While this article focuses on daily compounding, it’s beneficial to understand how it compares to other frequencies and what the theoretical limit is.

Monthly, Quarterly, Annually: A Comparison

- Annually (n=1): The least frequent. Interest is added once a year. This offers the slowest growth.

- Semi-Annually (n=2): Interest added twice a year.

- Quarterly (n=4): Interest added four times a year.

- Monthly (n=12): Interest added twelve times a year. A common frequency for many savings accounts and mortgages.

- Daily (n=365): The most common frequent compounding available for consumers, offering the fastest growth among discrete intervals.

The difference in total returns between daily and monthly compounding might seem small over a single year, but over decades, even a fractional advantage in compounding frequency can lead to thousands of dollars in difference in overall wealth.

Continuous Compounding: The Theoretical Limit

In financial theory, there’s a concept called “continuous compounding,” where interest is compounded an infinite number of times per year. While it’s a theoretical concept and not practically offered by financial products, it represents the absolute maximum growth potential from compounding. The formula for continuous compounding is $A = Pe^{rt}$, where ‘e’ is Euler’s number (approximately 2.71828). Comparing daily to continuous compounding reveals that daily compounding already gets incredibly close to the theoretical maximum, illustrating its efficiency.

The Long-Term Perspective: Why Daily is Often Superior

For most individuals seeking to grow their wealth through savings and investments, daily compounding offers a significant advantage over less frequent intervals. It maximizes the opportunity for earned interest to start earning its own interest immediately. While the difference from monthly compounding might be marginal in the short term, over an investment horizon of 10, 20, or even 30+ years, the power of daily compounding can contribute substantially to achieving financial goals such as retirement, homeownership, or higher education funding.

In conclusion, calculating daily compound interest is a straightforward process once you understand the underlying formula and its components. By leveraging this knowledge, utilizing available tools, and adopting smart financial strategies, you can harness the remarkable power of daily compounding to accelerate your journey towards financial independence and wealth accumulation. It’s not just a mathematical concept; it’s a fundamental principle of financial growth that, when understood and applied, can profoundly impact your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.